![]()

Image © Pound Sterling Live

The Bank of England (BoE) faces an unprecedented challenge as inflationary pressures resurge while economic growth stagnates, leaving the Monetary Policy Committee (MPC) more divided than ever ahead of a crucial March rate decision.

The latest meeting saw hawkish stalwart Catherine Mann make a dramatic pivot, advocating for a 50-basis point (bp) rate cut, a move that has sent ripples through financial markets.

The decision highlights the sharp contrast in views within the MPC and underscores the deep uncertainty surrounding the UK’s economic outlook.

On one side, dovish members argue that the economy is weakening due to declining demand and deteriorating sentiment, necessitating swift rate cuts to prevent long-term economic scarring.

On the other, hawkish policymakers contend that supply-side constraints remain a key driver of inflation, warranting a more cautious approach to monetary easing.

According to Paul Dales, Chief UK Economist at Capital Economics, the March meeting will be a critical moment for the BoE. "It would only take one member to swing the majority to cutting rates by 25bps," he notes, highlighting the razor-thin margins within the MPC.

"Given that three MPC members voted to speed up the pace of rate cuts in December and Mann’s vote today suggests she’ll join them, March’s policy meeting will be a humdinger. It would only take one member to swing the majority to cutting rates by 25bps," he explains.

Despite some members pushing for immediate easing, Dales believes the majority may remain hesitant:

"Our hunch is that the other five are not for turning, but the two GDP and labour market releases and one CPI release between now and then will be key."

Capital Economics also sees deeper cuts ahead, projecting a Bank Rate of 3.50% by early 2025, with the possibility of further reductions to 3.00% if economic weakness persists.

Andrew Wishart, Senior UK Economist, describes the committee as being split across multiple perspectives and ultimately the Bank will soon have to abandon its cutting cycle:

"The minutes described four differing views of the outlook for the economy rather than the usual two, making the future path of interest rates particularly uncertain."

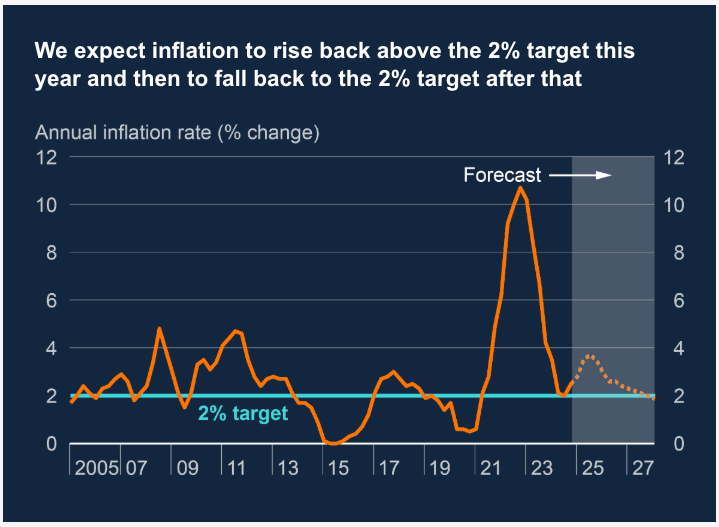

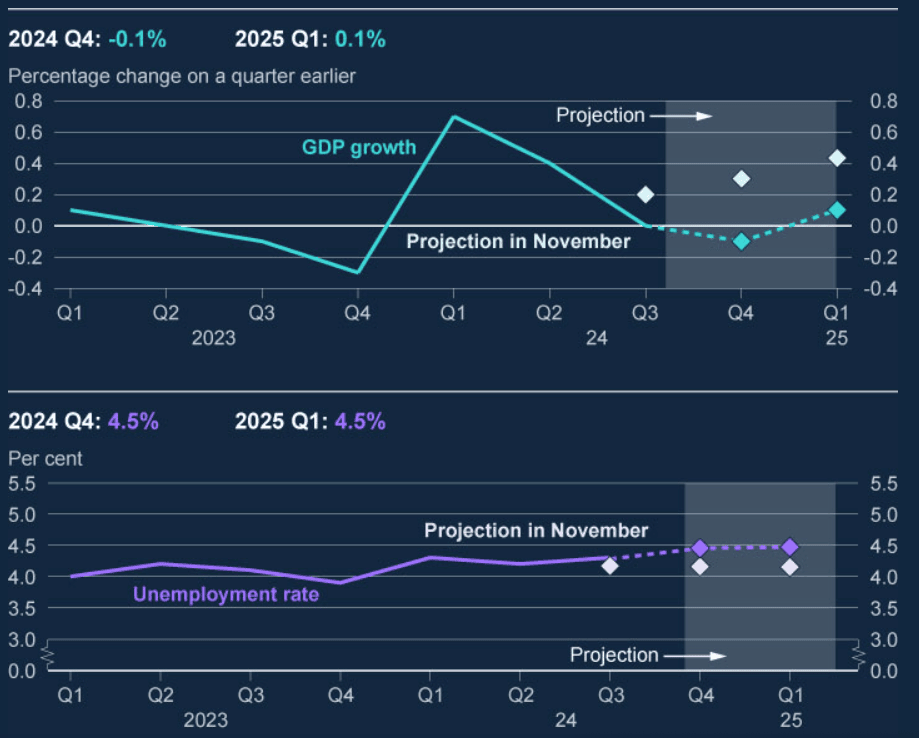

The BoE’s own forecasts add to the complexity, with its growth projections lower than market consensus while its inflation expectations remain significantly higher. Wishart warns that the BoE faces a difficult balancing act, needing to address both persistent inflation and faltering growth.

Wishart explains that the divide boils down to differing assessments of why the UK economy is faltering. Dovish MPC members see weakening demand as the main culprit and argue for aggressive cuts to avoid unnecessary damage to the labour market.

"Meanwhile, hawks maintain that inflation is still underpinned by supply-side constraints, suggesting that rapid rate reductions would be premature," he warns.

Berenberg thinks the Bank will be forced into abandoning its rate cutting cycle as soon as the second half of this year as inflation accelerates.

Mann’s U-Turn: A Market Game-Changer

Perhaps the most surprising development was the hawkish Catherine Mann’s abrupt shift, as highlighted by Kathleen Brooks, research director at XTB:

"Mann is an arch hawk who has previously favoured a ‘shock and awe’ approach to rate cuts. The fact that she thinks the economic picture is so dire that we need a 50bp rate cut is a sign that the BoE could be behind the curve."

This shift has led to market expectations for four rate cuts in 2025, with pricing across the curve falling by 8bps.

According to James Smith, Developed Markets Economist at ING Bank, Mann’s decision is highly significant:

"Not only has Mann ended her fight against rate cuts, but she has doubled down with a vote to slash rates by 50bp."

Mann's stance suggests that the BoE might need to act more decisively to realign policy with economic realities, despite its current cautious messaging.

What Comes Next?

Looking ahead, TD Securities’ James Rossiter forecasts a total of 125bps in rate cuts through 2025, with reductions expected at each meeting until August. However, he acknowledges that persistent inflation risks could lead the BoE to delay easing beyond March.

Meanwhile, Karl Schamotta, Chief Market Strategist at Corpay, notes that the BoE’s hawkish inflation warnings may limit the pound’s downside:

"The Bank warned that inflation could accelerate 'quite sharply' later this year before subsiding, which, combined with other factors, could temper the bearish outlook on GBP."

However, Jayati Bharadwaj, Global FX Strategist at TD Securities, warns that the dovish tilt from the BoE could leave sterling vulnerable:

"While investors have moderated their long GBP positioning, it remains optimistic compared to non-USD peers, making it susceptible to further downside risks."

The Verdict: March Will Be a Defining Moment

With inflation still a major concern but the economy showing clear signs of strain, the BoE’s March decision will be one of the most significant in recent history. As Wishart puts it:

"A boost to demand from rate cuts at the same time as firms are facing a large increase in costs will push inflation well over 3% later this year. The BoE will find it difficult to justify further loosening in that environment."

The BoE is now caught in a high-stakes balancing act—cut too soon, and inflation could reaccelerate; wait too long, and the UK risks sliding deeper into economic stagnation. One thing is certain: March’s Monetary Policy Committee meeting will be a humdinger.