Image © Adobe Images

This week's above-consensus UK inflation report provides the first tentative signals that the disinflation trend in the UK is stalling.

UK Chancellor Jeremy Hunt applauded the news headline that CPI inflation fell to 3.2% year-on-year in March, down from February's 3.4%, but market reactions centred around the fact that this figure was higher than expectations for 3.1%.

Digging into the details revealed numerous other upside surprises, with the more timely month-on-month prints in CPI, core and services inflation showing clear signs of resilience.

"The skew of inflation risks are shifting firmly," says Sanjay Raja, an economist at Deutsche Bank. "Upside risks are building around our projections."

Bank of England governor Andrew Bailey's reaction to the latest inflation figures was sanguine, telling fellow central bankers in Washington that inflation was progressing in line with expectations and that next month should see a sharp fall.

This alludes to the consensus expectation for inflation to fall below the magic 2.0% target next month as April's Ofgem household energy price cut makes a massive dent.

But, disappointment might be in the air. "The upside surprise today means we will likely have to wait until May for that first sub-2% reading, compared to April before," says Rob Wood, Chief UK Economist at Pantheon Macroeconomics.

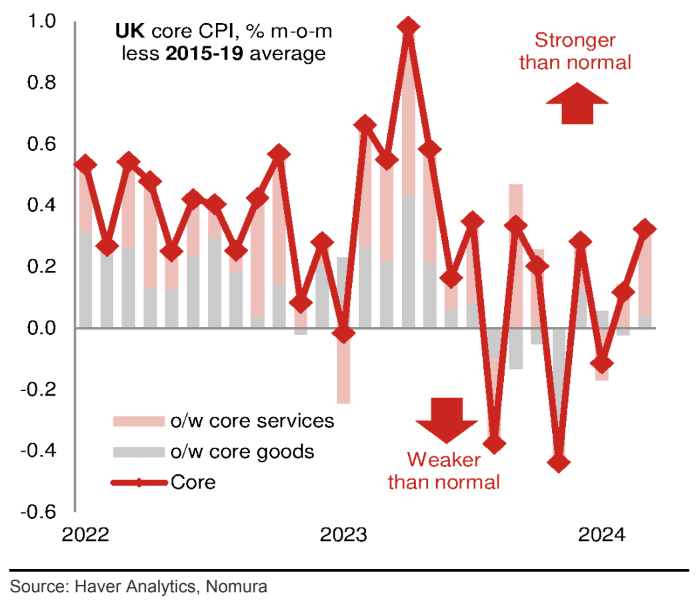

For the Bank of England to achieve its goal of anchoring inflation around 2.0%, core inflation must fall further. And for core to come down, services inflation must fall. The below chart from Nomura is instructive in that it shows momentum in core inflation is picking up again:

Services CPI inflation is where all the potential problems for the Bank of England might arise: this is the measure of inflation in the services sector, easily the largest sector of the UK economy.

"The risk is for a higher April services inflation reading than we previously thought," says Wood.

Services inflation surprised at a stubborn 6.0% in March, hardly budging on the previous month's 6.0%. The Bank of England and consensus expected it to fall to 5.8%.

"It feels somewhat optimistic talking of this stickiness as reflecting 'last mile risks'. Rather, it feels more like there’s a lot more work to do in bringing services inflation down to a level that is more manageable and, crucially, is consistent with the Bank of England’s 2% overall CPI inflation target," says George Buckley, an economist at Nomura.

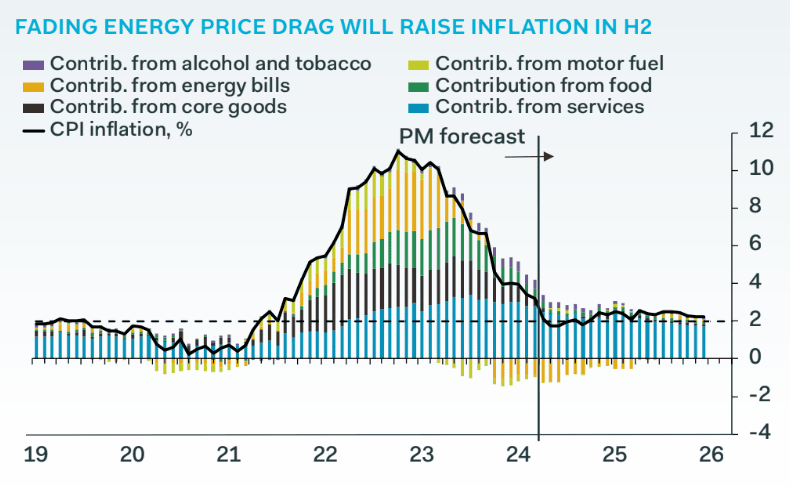

Above: The blue bars show services inflation, unless it falls, or unless goods inflation falls into outright deflation, achieving 2.0% inflation will be a hard ask. Image courtesy of Pantheon Macroeconomics.

Deutsche Bank warns that it's not just services inflation that could prove problematic, as its own bespoke Price Survey Tracker points to upside pressures on core goods.

"Logistical tensions from the Red Sea could result in some upward movement in core goods momentum in the second half of this year – something we've warned about before. Food prices could also turn later this year, lifted by heavy rainfalls dampening domestic production. And given rising geopolitical risks, oil and gas could also become more of an issue than we previously assumed with potential increases to dual fuel bills coming through in H2-24," says Deutsche Bank's Raja.

Deutsche Bank expects headline CPI to land around the Bank of England's 2.0% target in the second quarter but sees inflation bouncing back up in the second half of the year, running around 2-2.5%.

Ruth Gregory, Deputy Chief UK Economist at Capital Economics, says the risk is that UK inflation "will follow the trend in the U.S. and soon stall".

2024 inflation prints out of the U.S. show a clear pickup in inflation, leading markets to drastically slash expectations for the number of rate cuts from the Federal Reserve this year.

Markets have also taken a second look at UK interest rate expectations, now only expecting a first rate cut in September.

"The chances of interest rates being cut for the first time in June are now a bit slimmer," says Gregory.

Nevertheless, Bank of England Governor Bailey's comments in Washington are suggestive that a June rate cut is in play. He has previously said UK interest rates can be cut without risking a spike in inflation.

This suggests there is some tolerance to upside inflation surprises.

"We continue to think that CPI outturns over the coming months will convince the MPC that they can make monetary policy less restrictive, though risks are increasingly shifting to the Committee opting to wait until August to cut Bank Rate, compared to our call for a June reduction," says Pantheon's Wood.

Deutsche Bank expects the Bank will cut rates in May, but Raja concedes the "margin of error" the Bank faces in its fight against inflation "is narrowing."