- Stay reactive to debt ceiling outcomes says Julius Baer

- CIBC says this is the perfect time for fiscal restraint

- Rather cut spending now than when times are truly tight

Image © Adobe Images

Investors should remain reactive to any unexpected outcomes of the current U.S. debt ceiling negotiations says a strategist we follow, with another saying the issue offers a welcome opportunity to cut spending at a time of high inflation.

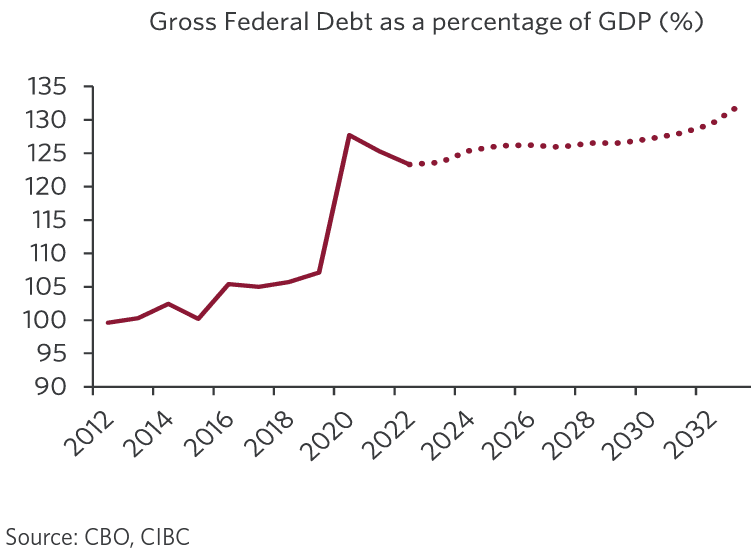

As the U.S. government approaches the deadline to address the statutory debt ceiling, market attention has been intensifying, with estimates indicating that the U.S. Treasury cash balance could be depleted as early as 1 June.

This situation has raised concerns among investors and the media.

Markus Allenspach, Head of Fixed Income Research at Julius Baer, provides a balanced assessment, stating, "we do not share the recent panic that a U.S. government default is unavoidable but recognise its 'low risk – big impact' element."

Allenspach believes that a last-minute deal is a likely scenario, encompassing a compromise that would result in an increase or temporary suspension of the debt ceiling, coupled with some social spending cuts.

He nevertheless acknowledges that as the deadline approaches without a resolution, market tension and volatility are expected to increase.

Image courtesy of CIBC Capital Markets.

Allenspach emphasises that from an investment strategy standpoint, reacting to the event rather than repositioning beforehand is the appropriate approach.

However, he points out that regardless of the debt limit drama, the current environment of tighter financing conditions has prompted a derisking of credit portfolios, supporting their call for quality bonds with longer durations.

Avery Shenfeld, Chief Economist of CIBC Capital Markets, offers a more optimistic perspective, suggesting that an outcome improving the U.S. economy's outlook is possible if some fiscal restraint is exercised now.

Shenfeld explains, "Not by spurring growth, which would be counterproductive while we're still battling inflation. Instead, if raising the debt ceiling includes some near-term fiscal restraint, that could allow for a more balanced overall stance of monetary and fiscal policy that would still bring inflation down."

Shenfeld believes that combining the efforts of both monetary and fiscal policy, with the latter involving some fiscal restraint, could result in a reduction in inflationary pressures without excessive downside risks.

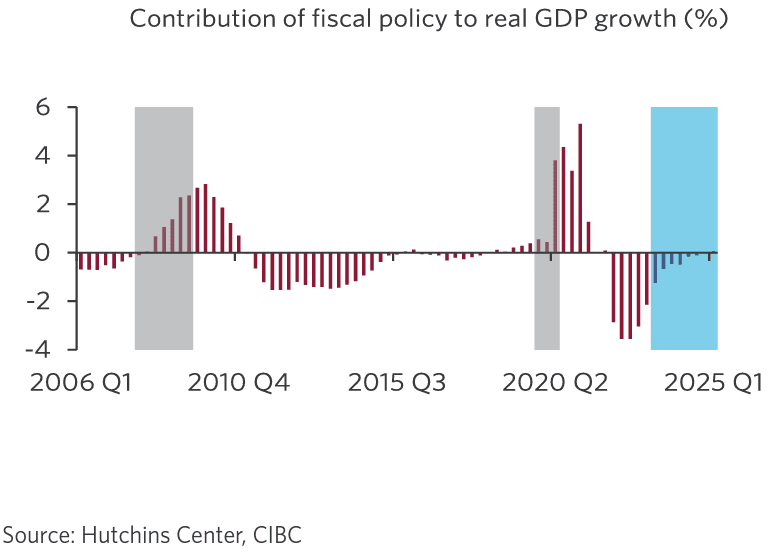

Above: |Fiscal policy no longer a meaningful drag" - CIBC Capital Markets.

He highlights the importance of fiscal policy in tandem with monetary policy, as it can influence the level of restraint and impact on economic growth. "Right now, we’re in a period in which fiscal restraint could actually be painless for the economy as a whole. Not because it doesn’t slow growth; virtually any mix of spending cuts or tax hikes will do just that. Instead, it’s because the Fed is already looking to stall growth for a few quarters to bring inflation back to 2% next year."

By tightening fiscal policy, the government would allow the Federal Reserve to potentially take a less aggressive approach to interest rates, avoiding further hikes or even advancing the timeline for rate cuts.

"If we don’t take opportunities to ease up on that path when they are available, it is surely going to be more difficult to lean against growing government debt when the economy has slack, and spending cuts or tax hikes would run counter to being at full employment," says Shenfield.

"What we fear is that the debt ceiling stalemate will be solved by pledging medium term fiscal restraint, which for all we know could hit the economy when it’s weak and in need of stimulus. The Chinese proverb notes that a journey of a thousand miles starts with a single step, and in the case of a fiscal journey to pare deficits, the right time for that step is now," he adds.