Image © Pound Sterling Live

Economists respond to another above-consensus inflation surprise, saying the Bank of England has little choice but to delay any further interest rate cuts.

UK inflation, the headlines:

- CPI annual inflation rose to 3.8% in July 2025, up from 3.6% in June.

- Services inflation rose from 4.7% in June to 5.0% in July, driven by airfares, package holidays, and insurance.

- Food inflation rose to 4.9%.

- Market-implied odds of a Bank of England rate cut in November close to 0%.

"Another hawkish blow to the MPC means no more cuts this year. The doves on the MPC have taken a battering over the past week. July’s figures show sticky underlying services inflation and are another blow to those on the MPC that argued hard at the August meeting about the disinflationary process being underway." - Elliott Jordan-Doak, Senior U.K. Economist at Pantheon Macroeconomics

"The Bank of England has been clear that government policies, which have driven up the costs of employment, are fuelling price rises at the till, while poor harvests and global instability have also added further cost pressures." - Kris Hamer, Director of Insight at the British Retail Consortium.

"The risk is this price persistence triggers renewed second round effects. That could yet derail the MPCs assumptions for a further, more intense, cooling of wage pressures into year-end." - Sam Hill, Head of Market Insights at Lloyds Bank.

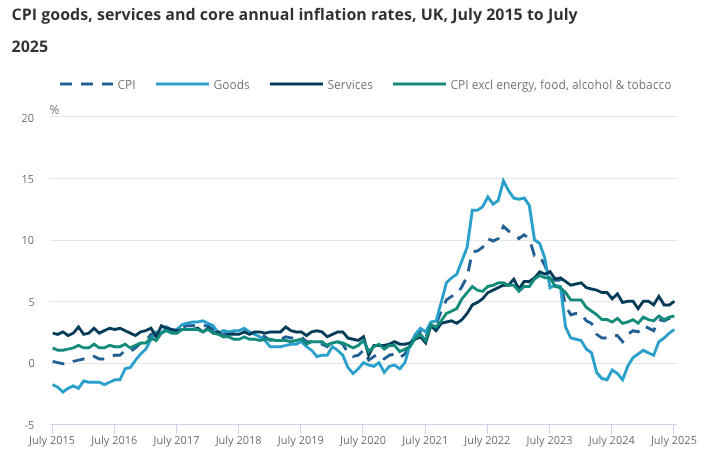

Chart: Until services inflation falls, headline CPI won't hit the target 2.0% on a sustainable basis.

"The perverse rate cut earlier this month looks even more ridiculous and irresponsible in the light of this news. 4pc plus inflation is coming in the autumn!" - Andrew Sentance, an economist who formerly served on the Bank's Monetary Policy Committee.

"The uptick in inflation comes after the Bank of England cut rates earlier this month. That’s an unfortunate look, although economists can argue that the rise in air fares may be a one-off. There was a swift market reaction to the data as traders started to price out the probability of further cuts in the near term. This saw sterling rally and FTSE 100 stock index futures fall." - David Morrison, Senior Market Analyst at Trade Nation.

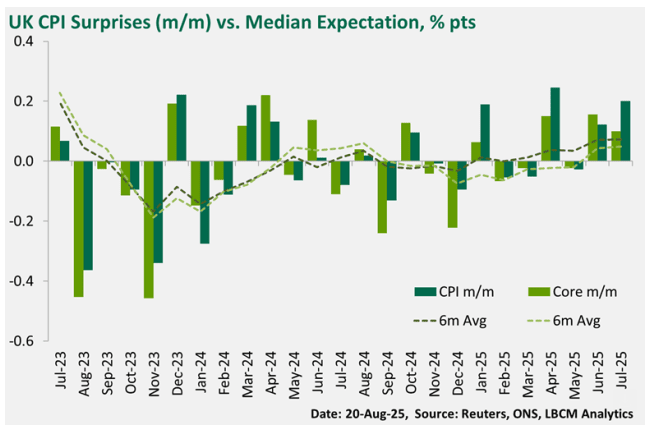

Chart: We're increasingly prone to underestimate inflation. Image courtesy of Lloyds Bank.

"Another interest rate cut is not likely in the next few months, it’s touch and go for December, with a reduction not fully priced in by financial markets until the spring. This is likely to keep gilt yields higher, and cause continued headaches for the government, given it pushes up borrowing costs, and keeps the public finances in a fragile state," - Susannah Streeter, head of money and finance, Hargreaves Lansdown.

Sanjay Raja, Chief UK Economist at Deutsche Bank:

Why the surprise? In short, the ONS’ price collection day was later than usual, just about coinciding with the summer school holidays.

Why does this matter? Prices for airfares and sea-fares tend to be more volatile later in July as demand picks up. In fact, according to the ONS airfares were up a staggering 30% m/m – the highest monthly increase going back to 2001.

The good news? Most of this will unwind in the next month or so.

The bad news? Cost of living pressures remain with food prices on the up and pump prices still on an ascent. With food inflation topping the Bank of England’s forecasts, concerns around inflation expectations will be hard to shake off for the MPC.

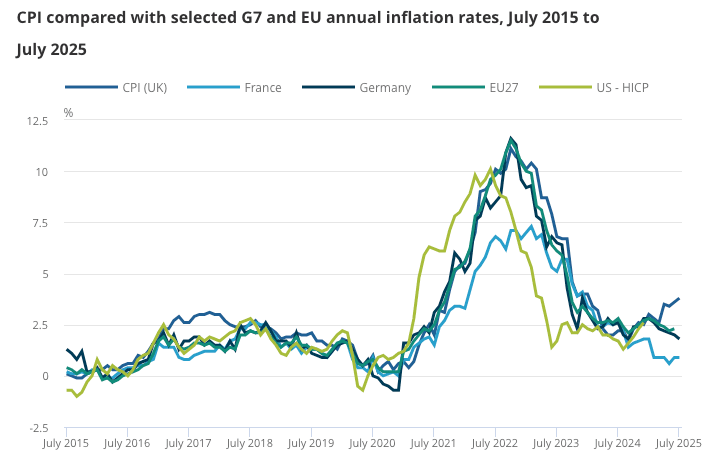

Chart: UK inflation increasingly an outlier.

"After falling to the 2% target in the final two months of the last government, UK CPI inflation has now diverged sharply again from the euro area. This divergence mainly reflects increases in government-set prices, higher taxes, and higher housing costs." - Julian Jessop, independent economist, IEA Economics Fellow.

"The risk of stagflation is very real. If the UK is heading towards the economic "worst of all worlds", it’s not clear what the central bank or the government should do about it." - Nicholas Hyett, Investment Manager at Wealth Club.

"As far as the Bank is concerned, we are still on track. The key question is whether the elevated inflation we see on the way embeds itself in expectations, and impacts price and wage-setting in the medium-term. For now, the combination of faster price rises and resilience in real GDP growth will see Bank sticking to its ‘gradual and careful’ approach, with markets expecting one more cut at most this year." - Adam Deasy, Economist at PwC.