Next year, young people will be able to earn more on out-of-work benefits than on a minimum wage job. Picture by Lauren Hurley / No 10 Downing Street.

The world is awash with debt, but the UK will be punished first and hardest.

Bond markets are prodding and testing the UK's debt markets, similar to the tremors that arrive before a major volcanic eruption.

"Bond Vigilantes are losing patience with populist politicians who can't seem to do basic fiscal arithmetic. They are casting around for a scapegoat and it is increasingly clear that the UK may well be first to be hit full on," says Albert Edwards, an economist at Société Générale.

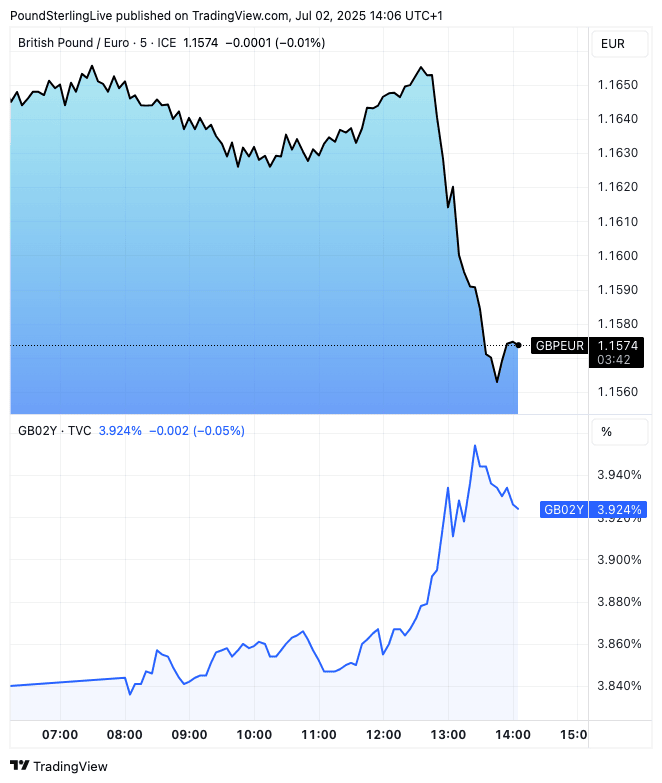

Last Wednesday the UK suffered a bond selloff as investors questioned the sustainability of the UK's debt trajectory. We saw a similar episode in January, when it became clear UK growth was going to disappoint, despit the huge boost to public spending announced by the new Chancellor, Rachel Reeves, in October of 2024.

The episodes were mini versions of the market fallout that followed Liz Truss's famed 2022 'mini budget'.

"In retrospect, the Liz Truss budget debacle back in September 2022 might seem like a tea-party compared to what is coming down the line," he adds.

Above: Price action from Wednesday July 02. Bond yields up (lower panel) and GBP down. Usually GBP would rise when gilts rise. When this breakdown in correlation happens it signals an unease over UK debt sustainability.

An eruption is getting closer, and the warnings are becoming louder and more frequent. The Office for Budget Responsibility this week focused minds when it stated "the risks to the fiscal outlook are mounting."

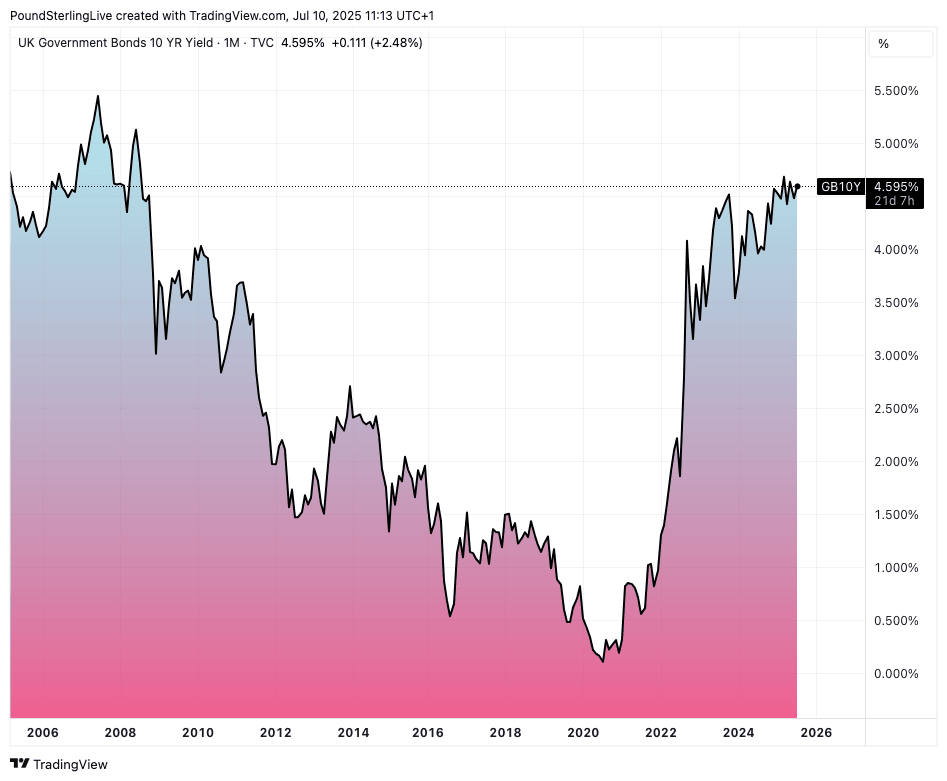

UK debt yields are rising, particularly on long-dated debt issuance, such as the ten-year and 30-year. This is being driven by rising term premium, which in financial speak is simply the premium investors demand to account for rising fears that the government won't be able to honour that debt at some point in future years.

Edwards, who is a chief global strategist at Soc Gen, has been an economist in the City of London for over 40 years, which means he knows that the decade of ultra-low interest rates that followed the 2008 financial crisis was an anomaly.

That decade allowed governments to become spendthrift and pay lip service to debt sustainability. But the return of inflation means interest rates are resetting close to historical levels, putting significant pressure on governments that haven't adjusted to the new reality.

Above: The cost of debt is rising.

The current left-wing Labour Government is particularly unsuited to meet the needs of the new reality.

"Successive humiliating U-turns by the UK government as it struggles to get welfare cuts through parliament despite its massive majority really has placed the UK Gilt market dead centre in the crosshairs," says Edwards.

Prime Minister Keir Starmer last week had to abandon an effort to trim the growth in the UK's runaway benefits bill.

More and more working-age people in the UK are signing up for out-of-work benefits, with the Personal Independence Payment (PIP) being the main gateway. This allows those with a wide ranging set of ailments, including acne, anxiety and ADHD, to 'sign on'.

As a result of the government's generosity, the Centre for Social Justice, a think tank, says jobless Universal Credit claimants who also receive PIP will receive £25,000 next year, while a worker on minimum pay will, after tax and NI, only receive £22,500.

But the biggest component of the welfare bill is the state pension, which continues to grow in real terms thanks to the Triple Lock guarantee that was designed to ensure pensioners are left better off year after year. It is something the OBR is particularly concerned about.

"Having witnessed the debacle of the UK budget arithmetic, the Bond Vigilantes are now voting with their feet. Who can blame them? This week’s report from the Office of Budget Responsibility (the UK’s fiscal overlord) makes for disturbing reading," says Edwards.

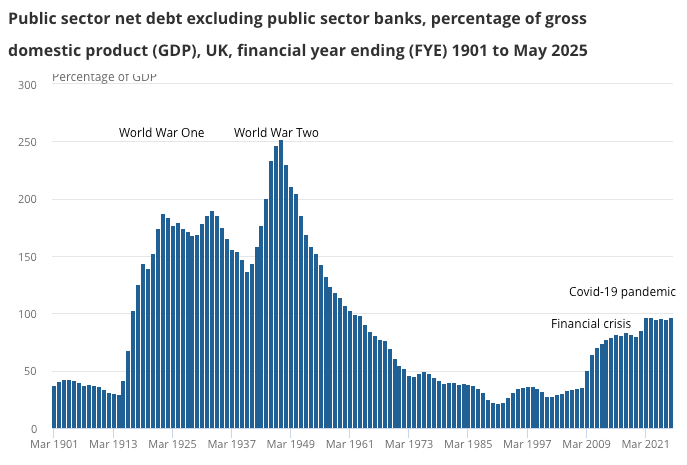

Yet, the UK's debt dynamics are not as bad as those of the U.S., France and Japan. So why the focus on Britain?

Each of those three examples has some sort of special dispensation, which the UK doesn't:

- The U.S. has the exorbitant privilege of issuing the U.S. Dollar, the world's global currency.

- France is wrapped tightly in the Eurozone, which is dominated by Germany, a fiscally more austere country. The ECB also provides a formidable backstop, similar to that the U.S.

- Federal Reserve offers the Dollar.

- Japan has the highest debt-to-GDP ratio of the developed world, yet it runs current account surpluses, meaning it is a net saver.

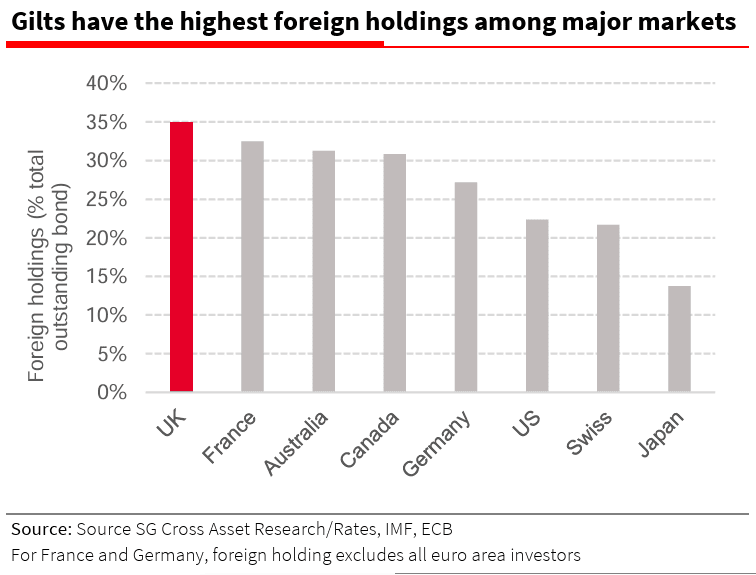

The UK is none of the above. Bond specialists say the UK Gilt market is noticeably more vulnerable to the fickleness of foreign investors than most other government bond markets because foreigners make up a decent chunk of the UK debt customer base.

Image courtesy of Societe Generale.

Are there any routes available to the UK other than massively cutting spending? No, says Edwards:

- "All the UK has left in its armoury is the ability to either:

back away from QT (but it was the BoE announcement of aggressive QT the day before Liz Truss’s Sept 2022 budget that likely triggered the Gilt market rout as much as the expansionary budget itself), or - do more of what the US Treasury and BoJ have been doing - twisting issuance away from the long end (see right chart above). But for me, that would be symptomatic of an overindebted EM country shuffling the fiscal deckchairs on a sinking Titanic. Delay is not a solution."

"I don’t want to be melodramatic here," he adds, "but I think Bill Gross may have been right about the UK Gilt market sitting on a bed of nitroglycerine, some 15 years on from his original pronouncement. The Bond Vigilantes are angry, and having identified the UK Gilt market as 'the weakest link' have started voting with their feet – in other words giving the extremely exposed UK Gilt market a good kicking."