"Recognising that its earlier actions are now gaining traction, the MPC needs to ensure that it does enough to return inflation to target, while guarding against the possibility that it does either too much or – for that matter – too little. Finding that balance is the central challenge for monetary policy at present" - Huw Pill, chief economist, Bank of England.

Image © Adobe Stock

The Bank of England (BoE) would risk going too far if it continues to lift Bank Rate as fast as it has in recent months, its chief economist Huw Pill has said, suggesting that he too could favour a return to more conventional sized increases, if any, as a response to lingering inflation risks up ahead.

Huw Pill has been one of the more 'hawkish' Monetary Policy Committee members of recent times and his Thursday remarks suggested that a March increase in Bank Rate can no longer be taken for granted and that a smaller 0.25% uplift is perhaps the most that should be expected.

"Continuing to raise rates at the pace and magnitude seen over the past year would eventually – and perhaps soon – imply that monetary policy had cumulatively been tightened too much," Chief economist Huw Pill told Warwick Think Tank at Warwick University on Thursday.

"Nevertheless, given where we stand, I still choose to emphasise the MPC’s need to be watchful for signs of greater-than-expected persistence in inflationary pressure. And I would flag the need for the Committee to maintain a readiness to act to address any such persistence should it emerge," he added.

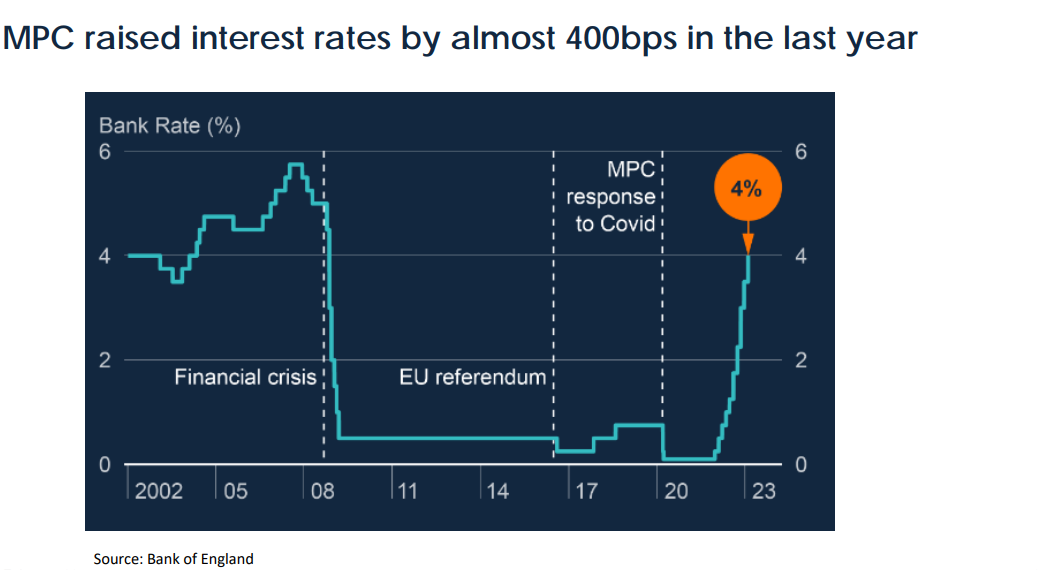

Bank Rate was lifted from 3.5% to 4% earlier this month in a fifth successive larger-than-usual increase, which followed equal sized moves in December, September and August last year that were themselves interspersed with a 0.75% uplift announced in November.

Source: Bank of England.

Source: Bank of England.

February's was the 10th increase in a row and brings the culmulative uplift in Bank Rate since December 2021 to some 390 basis points, while making for the strongest tightening of monetary policy since the late 1980s.

"While headline inflation is set to ease this year as the large increases in energy bills seen during 2022 begin to drop out of the annual calculation, the evolution of corporate pricing setting, wage developments and services prices is consistent with greater-than-desirable strength in the underlying, more persistent component of inflation," Huw Pill said at one point on Thursday,

"Both the March and May MPC meetings represent points at which the Committee can again assess the implications of incoming data for the monetary policy stance, with the latter having the advantage of an updated comprehensive assessment in the form of the MPC forecasts. As ever, I will come to my own conclusions about Bank Rate on those occasions on the basis of my assessment of the data flow," he also later added.

Thursday's address came barely more than a day after Office for National Statistics figures suggested that both UK inflation rates fell sharply in January with the overall pace of price growth falling from 10.5% to 10.1%, in line with BoE forecasts, while the core inflation rate fell from 6.3% to 5.8%.

Source: Bank of England.

Source: Bank of England.

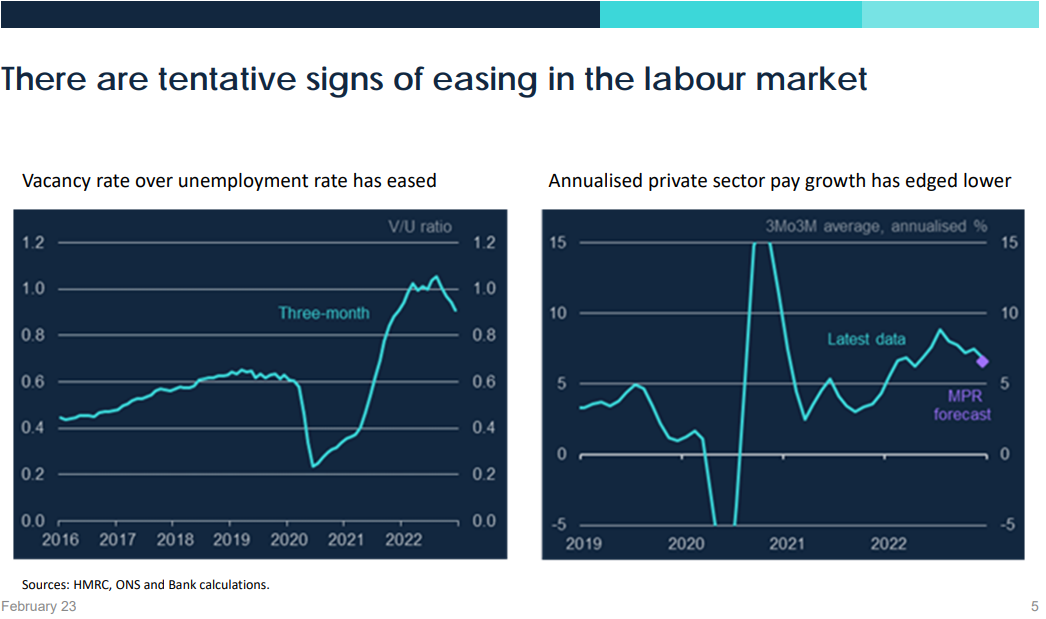

Inflation still remains far above the two percent target, however, and there were mixed signals about the outlook for it in Tuesday's December employment data.

Huw Pill acknowledged on Thursday that while the ratio of job vacancies to unemployed people has recently fallen to 0.9, from a peak of 1.1 back in August, salary and wage growth rates have also recently accelerated to an extent that could lead inflation to become self-sustaining at above-target levels.

Tuesday's data showed total pay including bonuses dipping from 6.5% to 5.9% last quarter but also revealed that growth in regular and permanent pay settlements had reached a new high by climbing from 6.5% to 6.7%.

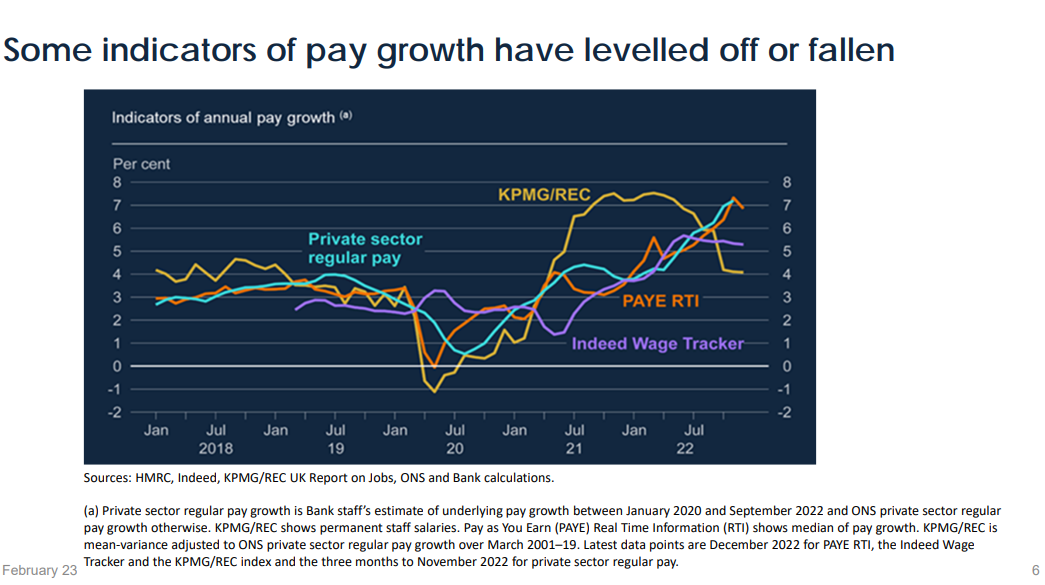

"While pointing to some easing in recent months, these indicators suggest the labour market remains tight in an absolute sense relative to historical experience. In turn, this is consistent with continued strength in UK wage growth," Huw Pill said on Thursday.

Source: Bank of England.

Source: Bank of England.

Permanent pay growth is, arguably, a greater concern for companies than that which comes through discretionary annual bonuses and so is potentially a far more potent determinant of the outlook for the inflation.

Rising pay growth often results from rising prices of goods and services but can also be a cause of rising prices and inflation, given how increases in labour costs for businesses can impact profit margins and price-setting decisions.

That dynamic is a narrow and one dimensional example of how inflation and its mechanical impacts upon national and global economies can lead it to fit the definition of a "wicked problem," which was the core subject of Thursday's speech at Warwick University.

"If striving to achieve price stability is a ‘wicked problem’ in the sense defined here, then it will always be premature to declare victory, since new disturbances to price stability can always occur and propagate," Huw Pill said in one part.

"To paraphrase Thomas Jefferson: the price of achieving meaningful price stability is eternal vigilance. For one of the characteristics of a ‘wicked problem’ is that it does not a have a ‘stopping rule'," he added in partial conclusion.