“Just think of ‘a while’ as longer than the months that the markets have priced in,” - Federal Reserve Bank of San Francisco President Mary Daly.

Image © Adobe Images

Federal Reserve Bank of San Francisco President Mary Daly said twice this week that bond markets are mispricing the outlook for U.S. interest rates and implied that a reset of expectations could be in store for the months ahead, which would have possible implications for the Dollar and other currencies.

U.S. bond prices and interest rate derivative markets have implied for some time now that investors view the Federal Reserve (Fed) as likely to raise its interest rate to 3.5% this year before cutting it again early in the new year.

This week and amid the recent market discussion about the perceived risks of a recession in the U.S., overnight indexed swap contracts have suggested the first interest rate cut is likely to come in May 2023.

But Fed policymakers are now warning against that assumption.

“Markets are really ahead of themselves on cutting rates. You know that was not something that if you looked at the June [forecasts], it was the last time you could see the dot plot, you didn't see any of that hump shaped behavior,” San Francisco Fed President Mary Daly said on Wednesday.

“So this is about just resetting. You know, the economy's got some strength. Inflation is too high. We are in a period of trying to get inflation down and create sustainable growth,” Daly told Retuers’s Lindsay Dunsmuir.

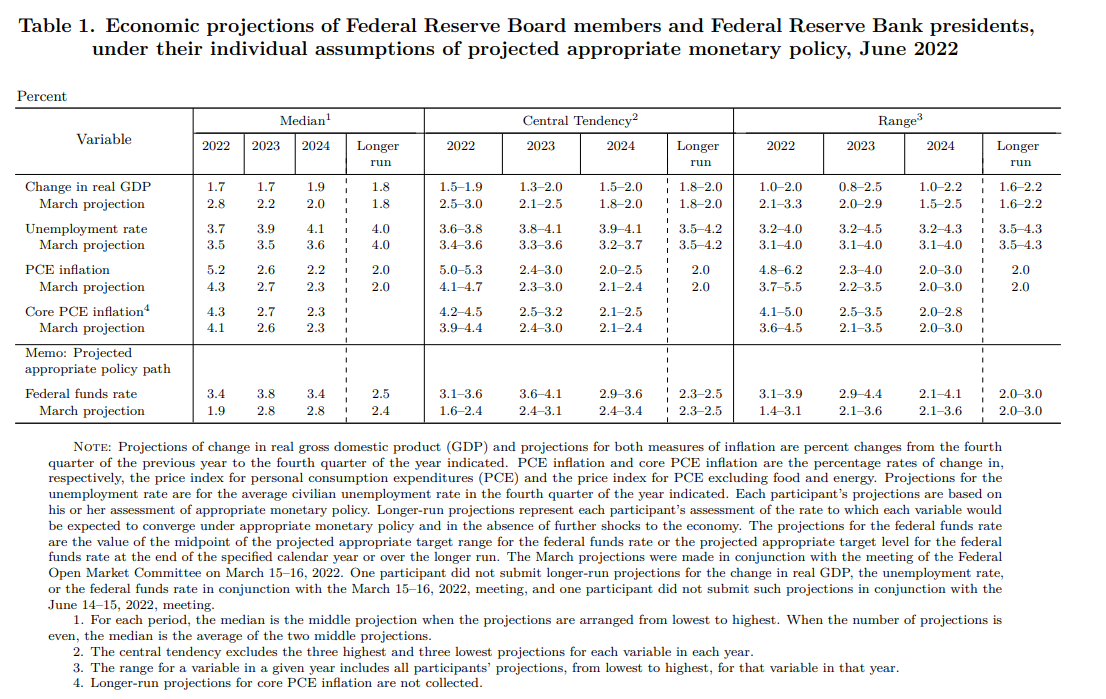

Above: Latest economic forecasts from FOMC members. Source: Federal Reserve. Click image for closer inspection.

Above: Latest economic forecasts from FOMC members. Source: Federal Reserve. Click image for closer inspection.

Daly’s remarks are most pertinent because as a 2023 voted on the Federal Open Market Committee of U.S. interest rate setters, she will help determine the Fed’s interest rate policy at exactly the point when financial markets are expecting the bank to begin cutting borrowing costs.

“My hope is that we have clarified our path and just reiterated the resolute thoughts we have. The fact that we're all united in making sure that we deliver on both sides of our mandate, which would include price stability, inflation of around 2% and full employment,” she said in a Twitter discussion.

Daly’s remarks echoed those made in a Tuesday interview with CNBC News' Jon Fortt where she described being “puzzled” by the pricing-in of interest rate cuts and said that borrowing costs could be “held at their peak for a while.”

On Wednesday she offered insight into what was meant by the term “a while.”

“What I'm conveying when I say for a while is that I want people to recognize that I do not think we should ratchet interest rates up really fast and really high and with the idea that we'll then bring them down quickly by lowering rates. You know just a few months from that, which is that hump shaped curve you saw some people pricing in that is very hard on the economy,” she said.

Above: U.S. 02-year government bond yield shown at daily intervals.

Above: U.S. 02-year government bond yield shown at daily intervals.

“Just think of ‘a while’ as longer than the months that the markets have priced in. Not six months. You know, think of it as you know something like a year, but I don't want you to hold me to that because if you held me to that then you would be saying, well, that's the path no matter what happens. And that's actually not how policy is done,” she added in the Wednesday conversation with Reuters.

Daly’s remarks are even more notable in the context of her reiterated support for the policy plan outlined in June’s dot-plot representation of Federal Open Market Committee members’ forecasts for the economy, inflation and interest rates.

June’s Fed meeting saw members of the rate setting committee coalesce around a plan to lift the Fed Funds rate to a “moderately restrictive” level by year-end, which Fed policymakers think is somewhere between 3% and 3.5%, and to then raise it further to between 3.75% and 4% next year.

“Directionally when I look out there, I am working towards being able to raise the rate to a level where we can keep it there and that will be sufficient to push inflation back down to our price stability goal, all while not derailing the labor market in any significant way,” Daly said on Wednesday.

The June forecasts imply the Fed Funds rate is likely to be lifted as far as 4% next year while Daly said that once it reaches that level, it could remain there for some time, implying that U.S. bond yields like the 02-year may still be too low.

Above: U.S. Dollar Index shown at weekly intervals alongside 02-year U.S. bond yield.

Above: U.S. Dollar Index shown at weekly intervals alongside 02-year U.S. bond yield.

The Dollar has proven sensitive to changes in the shorter maturity U.S. bond yields, which has surged this year after it became clear that the inflation challenge faced by economies and policymakers would be prolonged by the Russian invasion of Ukraine.

This sensitivity and the level of yields could mean the U.S. Dollar’s rally is not yet done and that it still poses risk to other currencies including Sterling.

Daly’s remarks came in the middle of a financial market attempt to gauge how close the U.S. economy is, or isn't, to slipping into recession although she and other Fed policymakers have continued to pour cold water all over that notion.

“Recession fears are a little inconsistent with an economy adding almost 400,000 jobs a month and with unemployment near its historic low at 3.6 percent. But I understand the concerns,” Richmond Fed President Tom Barkin said on Wednesday and just days ahead of the July payrolls report.

“So there is a path to getting inflation under control. But a recession could happen in the process. If one does, we need to keep it in perspective: No one canceled the business cycle,” he told the Shenandoah Valley Partnership at Blue Ridge Community College.