Above: File image of Huw Pill. Image © Global Utmaning, Lasse Skog. Modified from original, reproduced under CC licensing, non-commercial.

The Bank of England looks all but set on a path to raise Bank Rate to just above 1.0% in 2022, according to its Chief Economist.

In a speech Huw Pill says the severity of inflationary pressures facing the UK and expectations for high wage growth means further rate hikes are required.

Pill said he voted for a rate hike of 25 basis points on February 03, and not 50bp, but acknowledged "that decision was finely balanced for me as an individual voter on the MPC."

Pill said the substantial upward pressure placed on inflation broadly rests with surging global energy prices, which are out of the Bank's remit.

However, another key ingredient to the inflation mix is wages, and this is where the Bank can exert influence by managing inflation expectations.

"Recent data confirm that the UK labour market is tight. It is tighter than we expected at the time of the previous Monetary Policy Report published in November. And we expect it to tighten further in the coming months," says Pill.

The Bank's economists in February revised up their underlying wage growth forecasts for 2022 to rates approaching 5%.

"Given expected productivity developments, this rate is probably stronger than that consistent with the inflation target over the medium term," says Pill.

On the all-important question of future rate hikes, Pill says a move to 1.0% by December is baked into the equation.

"Following the market-implied path to 1.2% by the end of this year would have left inflation somewhat below target. I leave it to you to draw any implications for where the MPC sees the path of Bank Rate headed," says Pill.

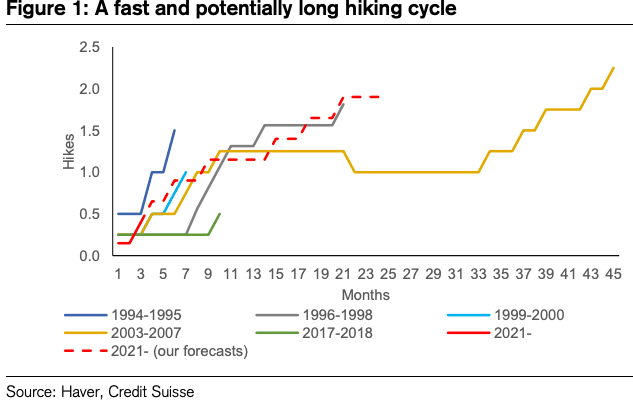

Above: Credit Suisse see a "fast and furious" path higher for Bank Rate. The story is here.

But were we to see evidence of second round effects in wage and cost developments, a tighter policy than otherwise might be required.

On the other side of the equation, Pill said were energy prices to fall steadily in line with futures rather than stabilise as the Bank assumes, then – other things equal – more policy accommodation could be maintained.

Pill said he remains committed to a steady, data-dependent reaction to price inflation.

"Restricting ourselves to a 25bp now – albeit with the prospect of more to come in the coming months – is an investment in containing market expectations of aggressive ‘activism’ that I saw as worth making," he said.

Pill reflected that since joining the Bank as Chief Economist in September he has retired the forward guidance that signalled unchanged policy rates and has brought asset purchases to an end.

He has also overseen the rise in Bank Rate and announced a start to the reduction of asset portfolios accumulated as a result of Quantitative Easing.

"From a starting point of substantial policy accommodation, this is a consistent, measured and resolute set of actions intended to rebalance the stance of monetary policy and address the inflationary pressures that have emerged," he says.