Above: Chancellor Sunak will still have some wiggle room to tax cuts in coming years. File image, Image © Gov.uk.

The latest set of government spending and borrowing data from the ONS was not as cheery as some economists had expected, largely because the cost of servicing debt is rising rapidly in line with surging inflation.

In fact, the cost of servicing debt could cost the government close to £60BN in the coming year, according to one economist.

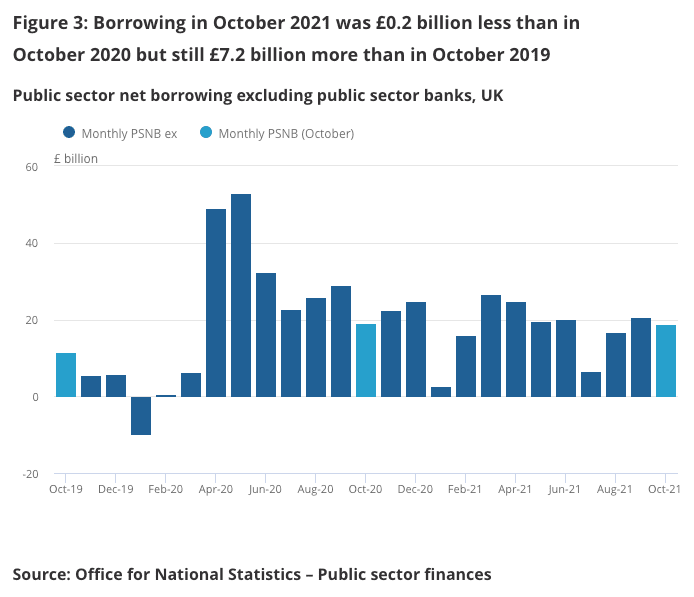

The ONS said public sector net borrowing (excluding public sector banks) read at £18.8BN in October, which was more than expected by the market (£14.0BN).

The official estimate of borrowing in the first six months of this fiscal year was revised up to £108.5BN from £108.1B previously.

"Public borrowing is falling much less quickly than earlier this year, reflecting the slowing of the economic recovery and the pick-up in inflation, which determines interest payments on index-linked gilts," says Samuel Tombs, Chief U.K. Economist at Pantheon Macroeconomics.

The deficit was therefore just £0.2BN lower than in October 2020.

The slim reduction to the deficit is despite estimated furlough expenses being £1.6BN lower than a year earlier as the schemes ended in September.

But the figure would have been worse had central government tax receipts not come in £3.8BN higher than expected.

"That suggests overall economic activity is holding up well," says Paul Dales, Chief UK Economist at Capital Economics, a view confirmed by the better than expected economic data out of the economy reported this week.

Surging inflation means a major concern going forward will be the cost of servicing debt.

The ONS says debt interest payments for October were at £5.6BN, which is £3.8BN higher than the comparable period a year earlier.

Tombs says this is due to the surge in inflation as measured by the RPI.

Index-linked gilts issued by the government are bonds on which interest is expressed in real terms by linking it to the retail prices index (RPI).

UK RPI rose 6.0% in the 12 months to October.

"Interest payments on government debt were £3.8bn up on the year, as the surge in RPI inflation automatically lifted payouts on index-linked gilts," says economist Sandra Horsfield at Investec.

Horsfield says given the lag between inflation and coupons on index-linked gilts, and also given that inflation is likely to move higher still in the coming months, "the harm to the public purse from higher inflation looks set to intensify in the near term".

"Our latest RPI forecast implies that debt interest payments will total £60.5B this year, £3.0B above the OBR's forecast," says Tombs.

Further headwinds to the outlook are provided by expectations for underwhelming growth; Pantheon Macroeconomics forecast GDP to rise 1.0% in the fourth quarter and 0.8% in the first quarter of 2022.

As such Tombs says the Office for Budget Responsibility's (OBR) forecast for GDP to rise by 1.9% in the fourth quarter and 1.2% in the first quarter of 2022 "looks too upbeat... accordingly, tax receipts likely will undershoot the OBR’s expectations over the coming months."

Pantheon Macroeconomics forecast public borrowing will total about £188BN in 2021/22 and £95BN in 2022/23, which is more than the OBR’s £183B and £83B forecasts.

Although the outlook for the UK's public sector finances have deteriorated somewhat, economists all agree that the Chancellor Rishi Sunak will find he still has extra wriggle room over coming months and years.

"Notwithstanding our forecast that GDP growth will be soft over the next six months, our assumption of smaller long-term scarring suggests that the Chancellor will meet his fiscal targets sooner than the OBR expects," says Dales.

Tombs says the Chancellor had a £25BN margin for error in meeting his target for a current budget balance in three years’ time.

"And since the target rolls forwards every year, we still expect Mr. Sunak to cut taxes in 2023, in the run up to the next election," says Tombs.