- Plurality of views keeps BoE’s policy outlook up for debate

- Despite August’s notice of tighter policy settings up ahead

- Key differences on timing, pace of lift-off & outlook for GBP

Image © Adobe Stock

The August monetary policy decision from the Bank of England (BoE) gave companies and households advanced notice that a normalisation of interest rates could be likely over the coming year or so, although as ever there remains a broad plurality of views among analysts and economists on the question of exactly when borrowing costs and savings returns are likely to rise.

This month’s policy decision proved to be a milestone in the UK economy’s journey through the pandemic after the BoE’s announcement revealed that an unknown number of the eight participants in August’s Monetary Policy Committee (MPC) meeting thought the Bank’s minimum economic thresholds for necessitating an interest rate rise had already been met fully during recent months.

“Some members of the Committee judged that, although considerable progress had been made in achieving the conditions of the MPC’s existing policy guidance, the conditions were not yet met fully,” minutes of the MPC’s meeting read.

“The other members of the Committee judged that the conditions of the existing policy guidance had been met fully, as demonstrated by developments in economic data and the latest central projections for spare capacity and CPI inflation in the August Report, but noted that the guidance had made clear that these had only ever been necessary not sufficient conditions for any future tightening in monetary policy,” the minutes later state.

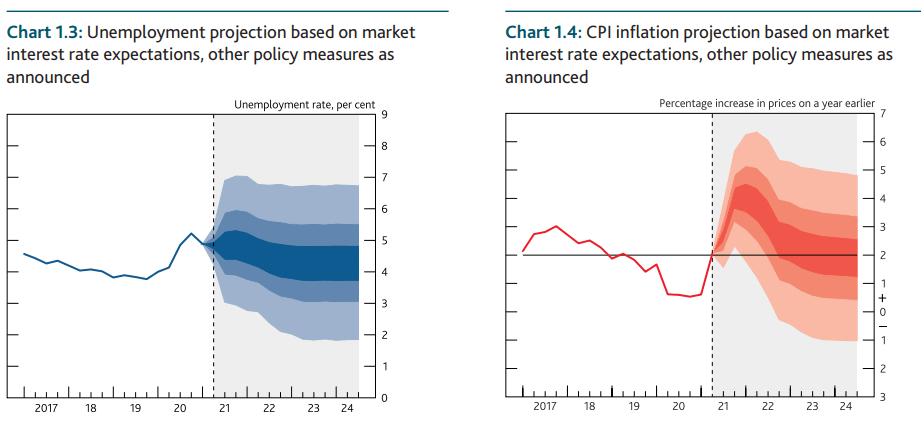

Above: Fan charts showing BoE assumptions for unemployment rate and inflation. Source: August Monetary Policy Report.

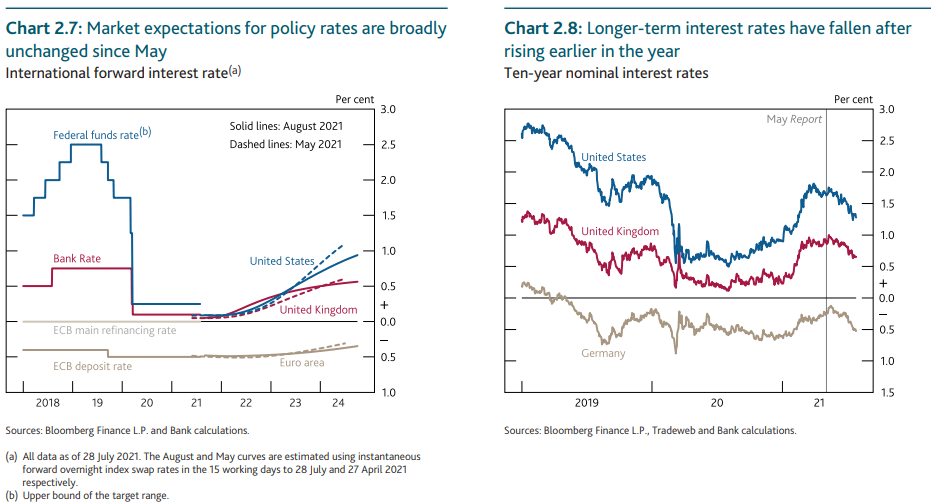

The MPC in the end agreed to leave Bank Rate at 0.10% and to continue as planned with the additional £150BN of government bond purchases announced as a supplement to the £895BN asset purchase target of its quantitative easing programme back in November, but the accompanying guidance made clear that the BoE’s interest rates would likely rise as soon as next year and that they could reach 0.50% before the end of 2023.

Furthermore, and following a months-long discussion, the BoE also set out the preconditions necessary for a steady reversal of its QE programme that would eventually see the £895BN portfolio of government and corporate bonds sold back into the market in a policy step that would also eventually have the effect of lifting borrowing costs and savings returns across the economy.

“The rapid recovery in demand has eroded spare capacity such that the economy is projected to have a margin of excess demand for a period. In the medium term, conditioned on the market path for interest rates, inflation is projected to fall back close to the 2% target, and demand and supply are expected to return broadly to balance,” the BoE’s August Monetary Policy Report says.

Above: Fan charts showing BoE assumptions for unemployment rate and inflation. Source: August Monetary Policy Report.

Driving the BoE’s decisions was the expectation of a continued strong bounceback by the economy this year and next that is seen encouraging a stubborn return of inflation, which was expected to reach 4% later this year; twice the level of the BoE’s 2% target.

It’s the inflation target that the BoE is seeking to meet when it makes changes to its policy settings, though inflation is influenced by many factors including overall activity within the economy as well as ‘supply side’ factors like the availability of goods and services.

There’s still plentiful scope for the fortunes of the economy to change over the coming quarters however, as well as ample room for the inflation picture to materialise differently to how it was envisaged in August’s meeting, which is a big part of the reason why analysts and economists still have a plurality of views about the outlook for the BoE’s interest rates and quantitative easing programme.

Some of these views are detailed below.

Shahab Jalinoos, head of FX strategy, Credit Suisse

“Last week’s BoE decision to map out its intentions around the sequencing of rate hikes and QE withdrawal reminded markets that the UK economy likely warrants quicker monetary tightening than most in G10.”

“The idea of persistent rate hikes that emerged again in the US in the past week was not mirrored in the UK...In our view, this conservatism in terms of UK rates pricing is the weak link that could yet be challenged by data in coming months.”

“If employment numbers in the Autumn are robust enough to suggest the end of the job furlough scheme in September will not lead to a jump in unemployment. Or if signs of post-Brexit / pandemic labour shortages deepen further and suggest persistent wage pressure is possible, we can imagine a scenario where by Q4, the market makes a meaningful attempt to re-price higher.”

Valentin Marinov, head of FX strategy, Credit Agricole CIB

“The resilience of the pound contrasts sharply with the underperformance of other European G10 currencies and, in particular, the EUR.”

“One recent reason for the recent decoupling between the GBP and the rest of the European G10 currencies has been the outcome of the BoE August policy meeting.”

“We doubt that the meeting was a hawkish game changer for the GBP, however, with the BoE likely to embark on a very gradual policy rate normalisation rather than a tightening cycle.”

“The BoE still doesn’t see any significant risk of runaway inflation in part because there was a limited scope for overheating of the UK economy beyond 2022. In all, we think that the BoE should remain hesitant to join the camp of the hawkish G10 central banks.”

Philip Shaw, chief UK economist, Investec

“After last week’s news, we have amended our view. We still envisage a Bank rate hike to 0.25% from 0.10% to take place in May 2022. However we now also expect a subsequent increase to 0.50% in Q4 2022. In tandem with the MPC’s guidance, we expect the BoE to cease reinvesting maturing gilts from 2023, facilitating a decline in its stock of assets...We expect outright gilt sales to begin in early-2024 (i.e. once the Bank rate is 1.0%).”

“At the same time, we are pencilling in two further increases in the Bank rate to 1.0% by end-2023.”

“Of course it is impossible to forecast the pace with any degree of confidence at all. However our working assumption is that the BoE will sell £20bn of gilts through the course of 2024 and 2025, in addition to the £130bn (currently) set to mature over those two years, shrinking the balance sheet by a further £150bn, effectively unwinding the additional QE supplied over the course of 2021.”

James Smith, developed markets economist, ING Group

“The Bank of England is no longer forecasting any real increase in UK unemployment later this year, even as wage support comes to an end. We think this may prove optimistic, and instead we think we could see an increase in the jobless rate to around 5.5% - though clearly this is still much lower than predictions made only a few months ago.”

“Taken together with the fact that inflation is likely to be much less exciting after a peak of around 3.5-4% later this year, a rise in unemployment would suggest the Bank of England is unlikely to rush into tightening in 2022. For now we’re pencilling in a rate hike in early 2023.”

Stephen Gallo, European head of FX strategy, BMO Capital Markets

“The current pricing of the sterling OIS curve has the first full 15bps rate hike baked into it by June (Figure 2). Assuming Q3 shapes up to be a strong growth quarter, and there is no harsh reimposition of restrictions during autumn and winter months, we don't see why that 15bps can't be pulled forward, especially since the BoE has scope to argue that the return to a 25bps setting is not a 'tightening move'.”

“Although the BoE believes a significant overshoot of the 2.0% CPI inflation target will be temporary, there is probably at least some acknowledgement within the MPC that the factors which severely held down inflation pressure immediately after the GFC are now working in reverse or gaining in intensity (namely: globalization, capacity constraints, bank lending, fiscal policy, and currency debasement).”

Michael Cahill, G10 FX strategist, Goldman Sachs

“The Bank of England’s updated outlook and exit guidance essentially aligned with the market’s view that the time for liftoff has been pulled forward, but the likely glide path will be relatively shallow.”

“Our economists maintain a much later liftoff (Q3 2023) than current market pricing, because they think there is more slack in the economy, which should translate into softer labor market and inflation data through year-end than expected by the BoE.”

“Given the BoE’s refreshed guidance on exit sequencing, as well as our slightly-revised Bank Rate forecast, we are upgrading our 3m and 6m EUR/GBP forecasts to 0.85 [GBP/EUR: 1.1764]; we expect the currency to be particularly sensitive to incoming data on inflation and the labor market as the furlough scheme expires, with a smaller revision to our 12m forecast to 0.87 [GBP/EUR: 1.1494] (vs aflat 0.88 path previously).”

“In revising their Bank Rate forecast our economists noted that risks are skewed toward earlier hiking, which also implies that risks are for a lower path for EUR/GBP than in our updated projections.”

Paul Dales, chief UK economist, Capital Economics

“We think tightening will start later than the markets expect, perhaps in August 2023. And we will be keeping an eagle eye on the labour market and wage data to see if our assessment is looking good or a bit skew-whiff.”

“The financial markets are fully pricing in a hike in Bank Rate from 0.10% to 0.25% by this time next year. The Bank’s inflation forecasts loosely suggest that might be a bit too soon.”

“In response to the Bank confirming how it will tighten policy, we now think Bank Rate will be raised a bit earlier and QT will start a bit later. Our new forecasts envisage Bank Rate rising from 0.10% to 0.25% in August 2023, to 0.50% in February 2024 and QT beginning in February 2024.”

Andrew Goodwin, chief UK economist, Oxford Economics

“While there was greater clarity on the strategy for future tightening of monetary policy, the potential timing was little clearer. The tone of the minutes was more hawkish, but the shift was subtle, and we think the MPC is still some way from starting active discussions about the need to tighten policy.”

“The £150bn programme of gilt purchases, which was set in train last November, is now very unlikely to be stopped before its planned finish at the end of the year. At the August meeting, only Michael Saunders voted to curtail it sooner. And with only two more opportunities to cut it short, the MPC’s forecasts appeared to set the bar high for a change of heart.”

Kallum Pickering, UK economist, Berenberg

“After ending asset purchases in December, we continue to expect the first-rate hike to come in August 2022 (15bps). Today’s meeting suggests the risk to this call are for a rate hike somewhat sooner than we project. If, as we expect, the BoE hikes the bank rate to 0.5% by end 2022 (following a 25bps hike in December), the newly outlined exit strategy opens the door for the start of a passive balance sheet reduction beginning in 2023.”

“While the voting pattern of the August meeting surprised a little to the dovish side, the overall meeting outcome and guidance is in line with the base case outlined in our preview – that we expect the BoE to begin to normalise its policy by the end of the year.”

Samuel Tombs, chief UK economist, Pantheon Macroeconomics

“We are bringing forward our expectation for the increase in Bank Rate to 0.25% to Q2 2023, from H2 2023 previously. We then expect Bank Rate to rise to 0.50% in Q1 2024 and for the MPC to stop QE reinvestment then too.”

“We think that CPI inflation will return to the 2% target in Q4 2022, four quarters earlier than the BoE expects.”

“In particular, we think that supply chain issues and strong pandemic-related demand for goods will have eased by early next year, causing core goods inflation to undershoot its long-run average.”

“We think that sterling will depreciate against the dollar to $1.35 over the coming months, from $1.38, as it becomes clear the U.S. Fed will raise interest rates sooner and further than the U.K. MPC, and then will remain at this level in 2022, as political risks start to be considered by investors again.”

“We expect a smaller depreciation against the euro to €1.17, given the likelihood that Eurozone interest rates remain stuck at the floor over the next two years.”