- Germany's inflation jump raises eyebrows

- Hints of strong Eurozone inflation in coming months

- Poses new challenge for ECB

- But ECB tipped to look through near-term price pressures

Image © Adobe Stock

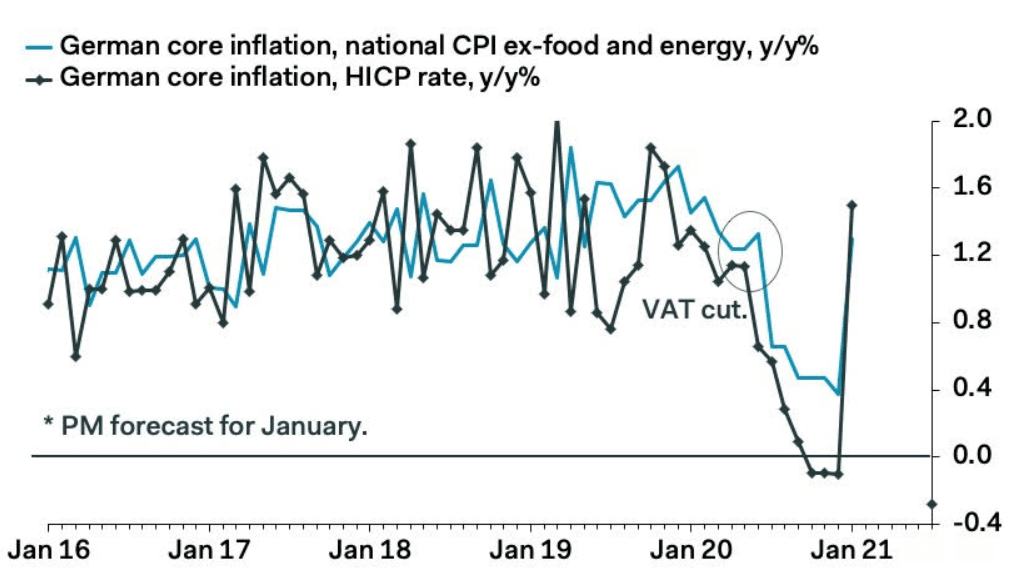

German inflation for January rose 1.0% on a year-on-year comparison, a sizeable rise from the -0.3% reported in December and well ahead of the 0.7% rise markets had been expecting.

"Watch out, the inflation monster is back," says Carsten Brzeski, Global Head of Macro at ING Bank.

According to Destatis, the month-on-month inflation rise stood at 0.80%, ahead of the 0.4% expected and the previous month's 0.50%.

"This was the largest monthly increase in a long time," adds Brzeski.

"The jump is much stronger than we and the consensus expected," says Claus Vistesen, Chief Eurozone Economist at Pantheon Macroeconomics.

Image courtesy of Pantheon Macroeconomics.

Economists at ING note that the strong print in German inflation figures do reflect a one-off effect where the VAT cut of 2020 is reversed, however focusing too heavily on the VAT rise risks masking inflationary pressures in the pipeline.

"Looking ahead, today’s inflation number is just the beginning of a period of significantly higher headline inflation in Germany," says Brzeski. "Interestingly, the prices for clothing increased sharper than justified by higher VAT, probably another result of the lockdown comparing fictive prices of closed retailers with winter sale prices from last year."

ING tell clients the inflation data "is just the beginning of a period of significantly higher headline inflation in Germany. The full impact of higher energy prices compared with last year will show in the coming months."

Economists at the bank say together with price mark ups in some sectors once the economy starts to reopen again, headline inflation in Germany could be pushed above 2% after the summer.

The rising inflation in Germany will unlikely be isolated, and economists are expecting the wide Eurozone to reflect similar price pressures.

Pantheon's Vistesen says what is now clear is that risks are firmly tilted to the upside for next week’s release of core inflation data.

Giovanni Zanni, Chief Euro Area Economist at Natwest Markets says "after a long bout in sub-zero territory, the January euro area inflation print should jump assertively into positive ground, helped by a long list of special factors."

Special drivers including energy base effects will further add to inflation later this year, "but will then wane again in 2022: underlying inflation is only on a slow recovering path in our projections," says Zanni.

{wbamp-hide start}{wbamp-hide end}{wbamp-show start}{wbamp-show end}

The sharp rise in inflation poses awkward questions for the European Central Bank (ECB) who will be questioned on why interest rates should remain so low and quantitative easing so generous just as inflationary pressures build.

It is clear that the inflationary pressures are coming despite an historic slump in Eurozone economic activity, meaning the ECB can't simply abandon its supportive policies even as inflation reaches their mandated 2.0% target.

However, ING's economics team say it is too soon to get nervous about rising inflation, highlighting that the economy will not reach its pre-crisis level before early-2022, unemployment and insolvencies are bound to increase and a further euro appreciation will be rather deflationary putting a lid on any inflationary pressure.

"Nevertheless, these inflation developments could easily present a new communication challenge for the ECB," says Brzeski.

"Recent comments on possible yield curve control, warnings against premature tightening of monetary and fiscal policies as well as more emphasis on symmetry and hence the possibility of inflation overshooting are just a few tools the ECB could use to preserve what seems to be the ECB’s latest treasure: favourable financing conditions," he adds.