Image © Adobe Images

UK retail sales were little changed in December after an anticipated rebound failed to materialise and government borrowing surged ahead of the festive holidays in what economists say should be taken by Chancellor Rishi Sunak as a warning against any tax rises in the March budget.

Sales rose by just 0.3% last month when consensus estimates had indicated that around a 1.1% increase was likely, while a revision to the estimated scale of November's contraction added insult to injury.

"Retail sales added almost nothing to GDP in December and January’s lockdown means a drop back will probably contribute to a fall in GDP this month," says Paul Dales, chief UK economist at Capital Economics. "These data highlight how the economy still needs the government’s financial support. The Chancellor should ensure that is the main focus of his Budget on 3rd March and not a desire to reduce the budget deficit by raising taxes."

December's rebound failed to materialise after allegedly non-essential businesses were instructed to close again across increasingly large parts of the country, while the contraction seen during the month-long November 'lockdown' was restated as -4.1% when it had previously been reported as -3.8%.

Source: Pantheon Macroeconomics.

"With non-essential retailers unlikely to get the green light to reopen until March at the earliest, Q1 will put many of them into the red, triggering more insolvencies over the coming months," says Samuel Tombs, chief UK economist at Pantheon Macroeconomics.

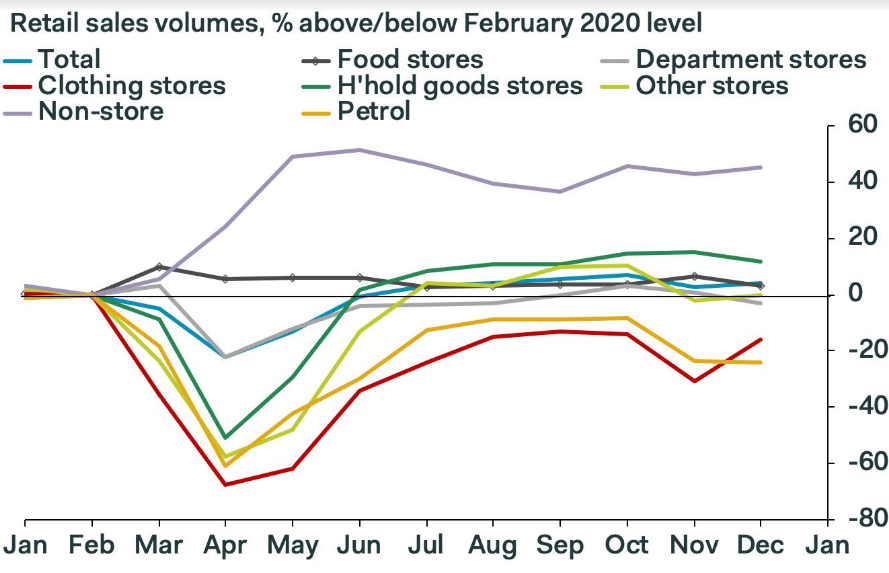

Sales surprised on the downside to end what will have been a year to forget for already-troubled bricks and mortar retailers who all saw sales decline by double-digit percentages in 2020. Food stores were the only exception with growth last year of 4.4%, while online retailers saw sales rise 46.1%.

The data came was just as the Office for National Statistics announced what was the third largest amount of government borrowing ever recorded for a single month with the public sector net-borrowing requirement having risen from a downwardly-revised £25.4bn in November to £34.1bn in December.

"Rishi Sunak may be receiving the message from the backbenchers that the time is right to bring the borrowing under control. However, the current lockdown may last longer still and the Chancellor may need yet another round of targeting easing. He should remember that he has a willing partner in the Bank of England, which continues to have further capacity to keep borrowing costs low," says Paul Craig, portfolio manager at Quilter Investors.

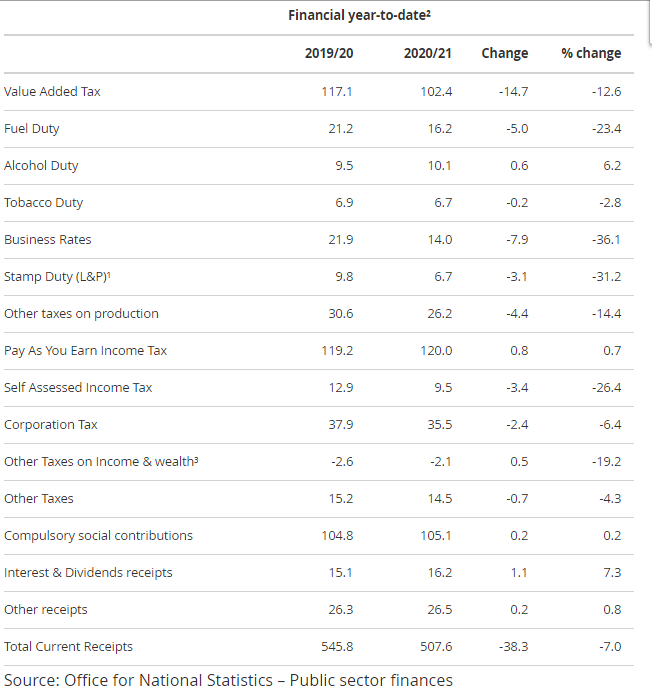

Above: UK Government tax receipts.

That's was £28.2 billion more in borrowings than for the same month in 2019 and came as the goverment lost tax revenues of £1.4 billion in December.

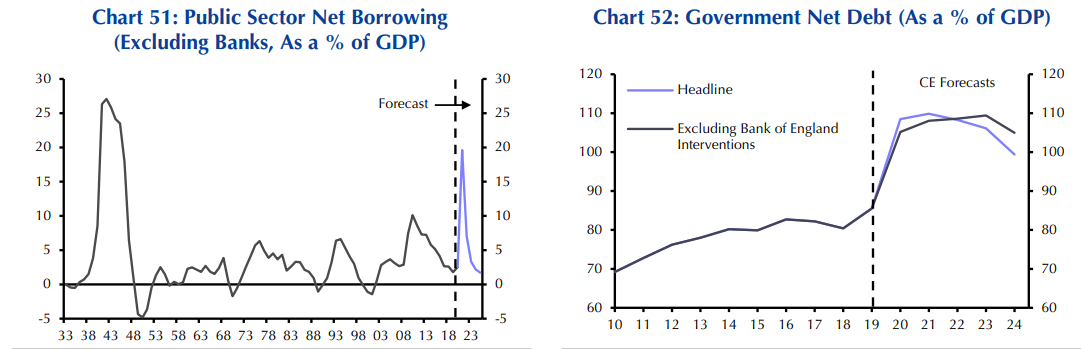

That month's new liabilities took total borrowing for the first nine months of this financial year to an estimated £270.8 billion, which is equivalent to 13.5% of GDP. Meanwhile, public sector net debt rose by £333.5 billion in the same time to reach £2,13 trillion by year-end, taking it to 100.5% og GDP.

The government spent £86.2 bn on day-to-day activities in December including HM Treasury's job furlough scheme with £4.7 bn spent as a part of the Coronavirus Job Retention Scheme (CJRS) and £5.3 bn on the Self Employment Income Support Scheme (SEISS).

"The rebound in GDP and record low interest rates will keep the debt to GDP ratio between 100% and 110% over the next five years. So taxes need only rise if the government wants spending to be higher than before the crisis and not to fill a fiscal hole" Dales says. "In fact, an early fiscal tightening could undermine the economic recovery, lead to a permanent loss in output and create the very fiscal hole the Chancellor is aiming to fill!"

Source: Capital Economics.

The government's wage and job subsidy scheme is set to remain in place at least until the end of March so the above near-record borrowings may be set to persist at least through the first quarter given the renewed national 'lockdown' announced in January and which has been indicated by the Prime Minister to be intended to last until Spring.

This means that turnover for many businesses faces ongoing disruption for months yet, which is why some analysts, economists and investors have spoken up preemptively against tax increases that weekend reports from the Ft and others suggested Chancellor Sunak may be entertaining for the March budget.

They argue the budget deficit would fall back naturally as the economy reopens and recovers from the pandemic so long as the government doesn't pull the rug out from underneath companies and households by either raising taxes or prematurely ending its various support programs.

"The Tories are falling into the old austerity-mantra trap," says Neil Wilson, chief market analyst at Markets.com. "Or are they? We should note, cynically, that it is never about doing what’s right for the country, only about getting re-elected. So, keeping the lid on spending, being ‘responsible stewards’ of the public finances and showing they are not spendthrifts like the other lot, is all terribly important....It’s going to take a long time to repair the damage of the government’s actions."