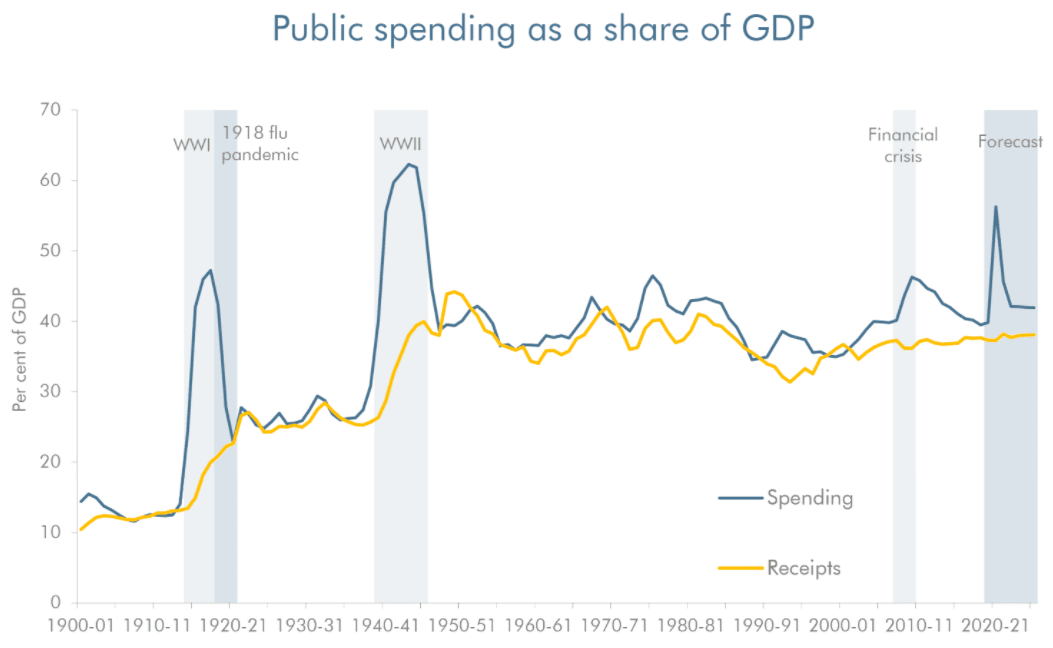

- UK at post-war record

- Tax hikes will be needed - Pantheon Macroeconomics

- PwC says economy can grow itself out of debt

- Economic output forecast to fall 11.3% in 2020

Above: The Chancellor Rishi Sunak leaves 11 Downing Street on his way to parliament where he will deliver his Spending Review. Image copyright Gov.uk.

The UK government announced mid-week that it would borrow significantly more money than at any other point in its peacetime history, but one economist says the bill is affordable provided the economy is encouraged to grow and debt repayments remain near record historical lows.

Despite the largest slump in the UK economy in more than 300 years, the UK government has committed to increase spending to support the economy and continue the fight against the covid medical crisis.

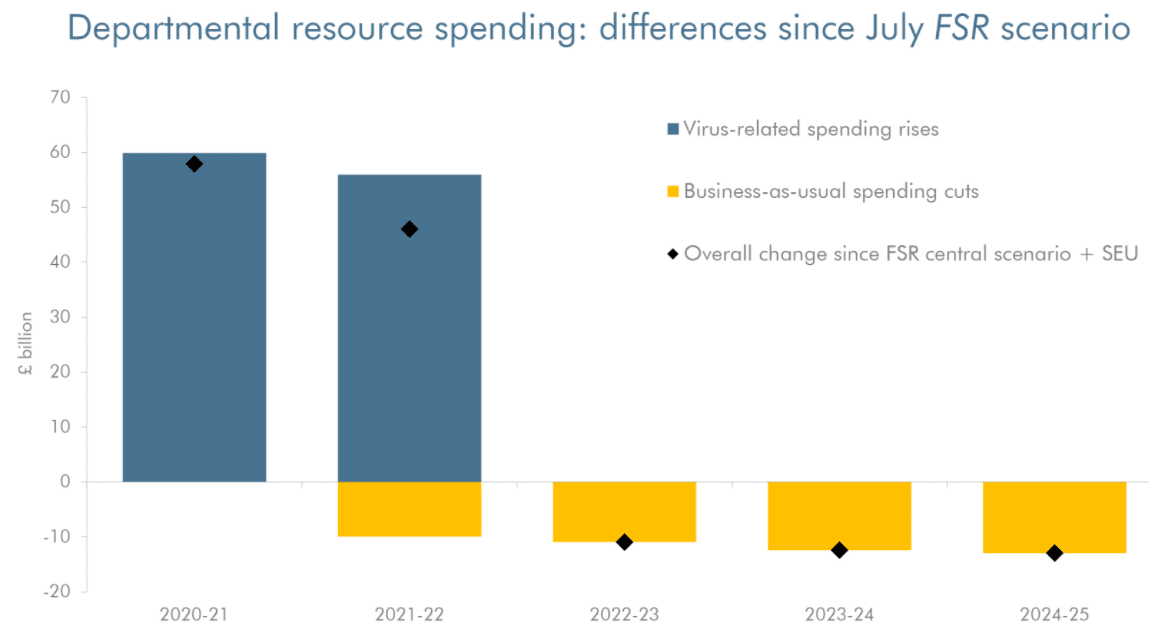

Chancellor of the Exchequer Rishi Sunak announced in his Spending Review that core day-to-day departmental spending would rise by £14.8BN in cash terms next year compared to 2020/21. From 2019/20 levels, that is an average growth of 3.8% a year, which the Treasury says is the fastest rate in 15 years and confirms that a return to the austerity that characterised the early years of the previous decade won't be repeated.

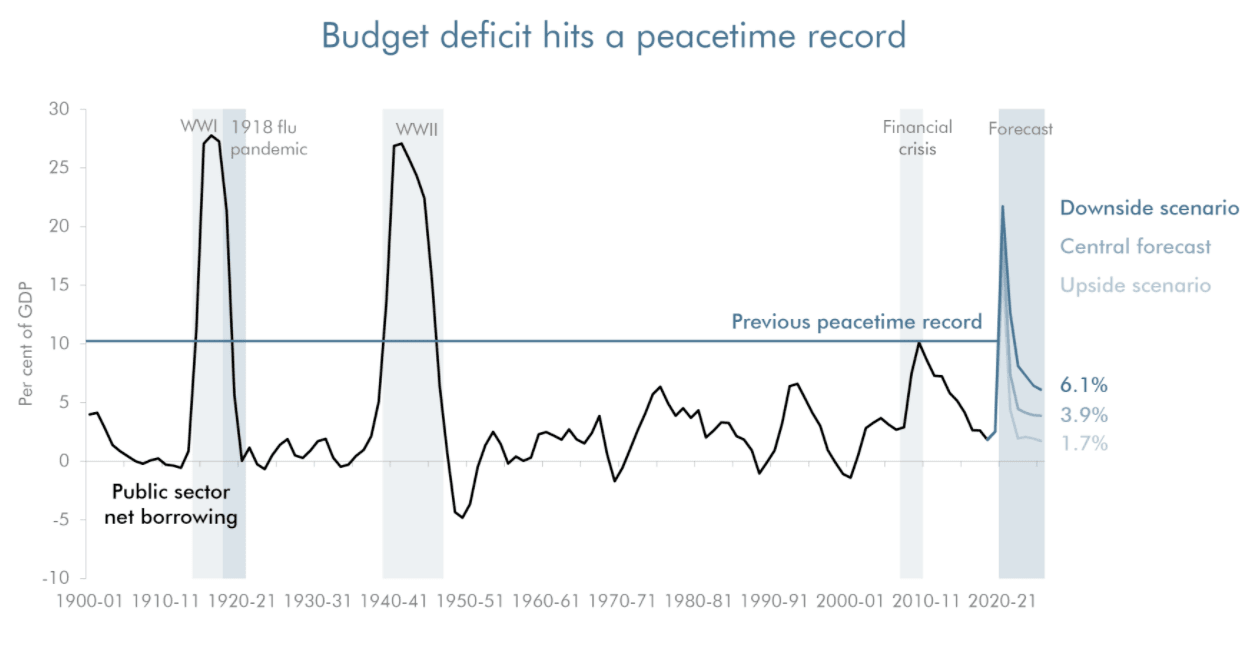

The independent Office for Budget Responsibility (OBR) has said in response to the Spending Review their central forecasts show the government will receive an income that is £57BN lower than last year, while it is on target to spend £281BN more than it did last year thanks to the crisis.

The deficit between what is earned and what is spent will therefore grow to a sizeable £394BN for the fiscal year ending in March 2021.

To lower the UK's debt burden, economists are warning significant tax rises and/or spending cuts will need to be executed in the future.

"With the demographic pressure on spending on health and pensions set to increase over the coming years and the government committed to spending more in 'left behind' communities, big tax rises look inevitable," says Samuel Tombs, Chief U.K. Economist at Pantheon Macroeconomics.

But, fears of sharp tax rises or deep spending cuts in future years to fund the gap between income and expenditure could yet prove premature, according to economists we follow.

"We knew that the UK borrowing figures would be eye watering. However, despite borrowing forecast to reach £394 billion this year, there are reasons to be optimistic - with a vaccine rollout on the horizon, the UK economy should be able to grow itself out of the deficit. So, despite a sharp increase, the deficit should come down sharply once the economy starts to recover," says Jonathan Gillham, PwC chief economist.

The OBR estimates borrowing this year will be at £394BN - or 19% of GDP - and will fall to 7.4% of GDP in 2021/22, 4.4% in 2022/23, and 4% in 2023/24.

"Fiscally hawkish Conservative members of parliament as well as some senior civil servants are apparently urging the government to begin – perhaps as soon as the next budget in March 2021 – a period of austerity to reduce debt and balance the public sector finances," says Kallum Pickering, Senior Economist at Berenberg Bank.

But Pickering says there is a case to be made for doing nothing yet as borrowing levels will settle back down to sustainable levels "relatively quickly"based on OBR forecasts, unlike was the case following the 2008 financial crisis when a "gaping structural deficit" opened, which could only be closed by cutting spending says Pickering.

"The benefits of spending aggressively to finance job and income support as well as public investment programmes, at a time when economic output is more than 10% below normal, far outweigh any distant risks that could materialise from the ongoing rise in public debt," says Pickering.

Despite the government's commitment to increase departmental spending, the OBR says the spending increase would largely fall in areas focussed on fighting the medical emergency and that a large temporary boost to departments’ budgets masks cuts to future budgets relative to the totals set out by the Chancellor in the March Budget.

"The Chancellor's decision to maintain higher public spending levels with a real term rise of 3.8% is welcome, but core spending is £10 billion less than what was announced in Budget 2020. Nonetheless, a refocusing of spending on growth priorities combined with ongoing emergency COVID spending, a rise in the national living wage and additional support for the long term unemployed, should help those who have been hardest hit by the economic consequences of the COVID pandemic," says Gillham.

A £100BN spend on infrastructure projects was confirmed while local government would have access to a £4BN fund for local projects. Defence was a winner as it secured a longer-term settlement than most departments to the tune of £24BN.

In tackling the covid-19 health emergency, the government committed a further £38BN for public services to continue to fight the pandemic this year - recall the government's fiscal year ends in March 2021 - and a further £55BN in 2021/2022.

The NHS will receive a £6.3BN cash increase in 2021-22.

While a pay freeze for the majority of public sector workers was announced, the Chancellor said pay increases for an estimated 2.1 million public sector workers who earn below the median wage of £24,000 would proceed, amounting to a pay rise of at least £250 each for the group.

Devolved governments received an income boost with Northern Ireland set to receive an additional £900M, Wales £1.3BN and Scotland £2.4BN.

{wbamp-hide start} {wbamp-hide end}{wbamp-show start}{wbamp-show end}

The OBR announced three forecast scenarios for the country's economic growth given the levels of uncertainty associated with the medical crisis. In a central base-case scenario UK economic output falls 11.3% in 2020 and unemployment peaks at 7.5% in the second quarter of 2021.

By historical standards, the OBR points out that the economy is suffering the sharpest contraction since the Great Frost of 1709.

In a better-than-expected outcome the economy would shrink 10.6% this year and unemployment will peak at 5.1% in the second quarter of next year.

But in a worse-than-expected scenario the economy shrinks 12% in 2020 and unemployment peaks at 11% next year.

The cost of funding the response to economic and medical crisis could also follow three seperate paths, based on which scenario transpires:

The government announced spending commitments that would likely require borrowing in 2020/2021 to rise £339BN, the lion's share of this borrowing (75%) will be owed to increased spending while a quarter is likely to result from the slump in economic growth, according to the OBR.

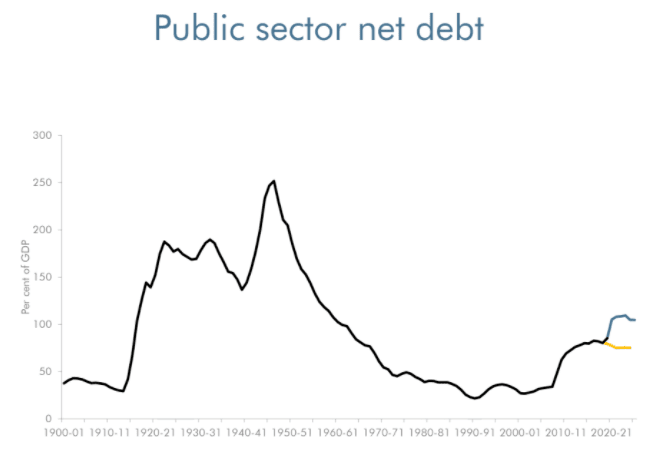

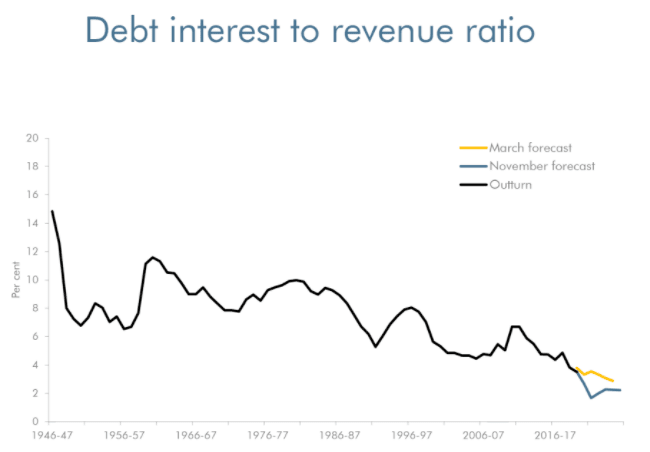

Funding the crisis through borrowing means UK public sector debt has risen above 100% of GDP for first time since 1960-61, i.e. the value of debt is greater than the entire value of the output of the economy in a year.

But despite the surge in debt, the OBR says the government will likely be able to comfortably fund the cost of borrowing given record-low interest rates which are forecast to come in lower than anticipated back in March:

The OBR meanwhile said the cost of the second national lockdown would be less than the first, primarily because schools have stayed open and businesses were largely better prepared. It is estimated the cost of the second lockdown would be three-fifths of the cost of the first:

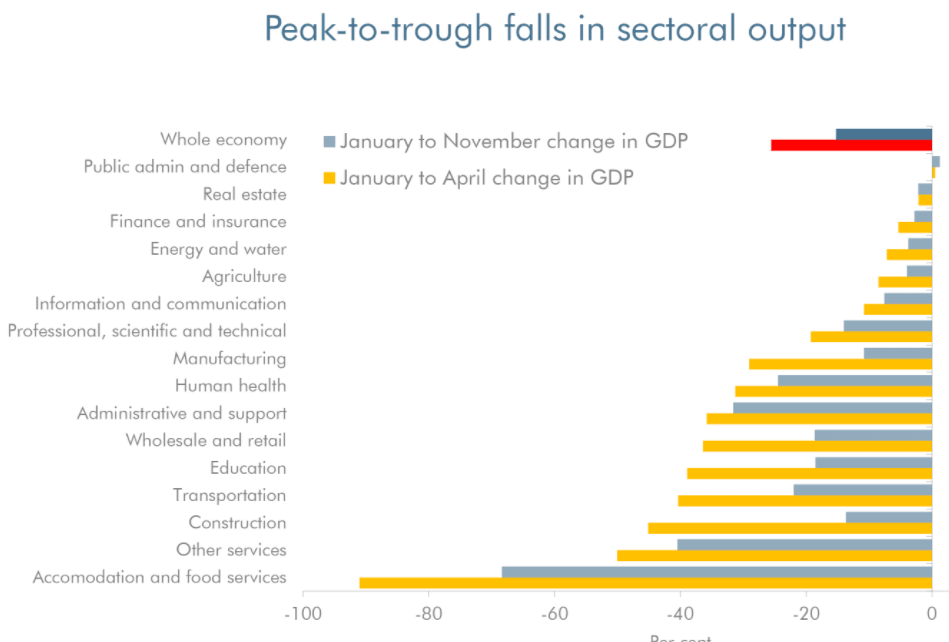

According to the OBR, while economic activity rebounded more strongly than they expected following the ending of the first national lockdown, a second wave of infections and a second lockdown in England took the wind out of the recovery heading into the autumn.

How the economy fares going forward now depends on how strict the phased reopening of England proceeds on December 02 and whether or not the EU and UK strike a post-Brexit trade deal. The outcome to ongoing talks might only become known in December.