Image © Adobe Stock

There are two weeks of oxygen left in the European economic coal mine before the Eurozone’s final quarter rebound fades like a quieting canary, economists at Berenberg suggested Friday, after IHS Markit PMI surveys warned of an October collapse in the continent’s services sector.

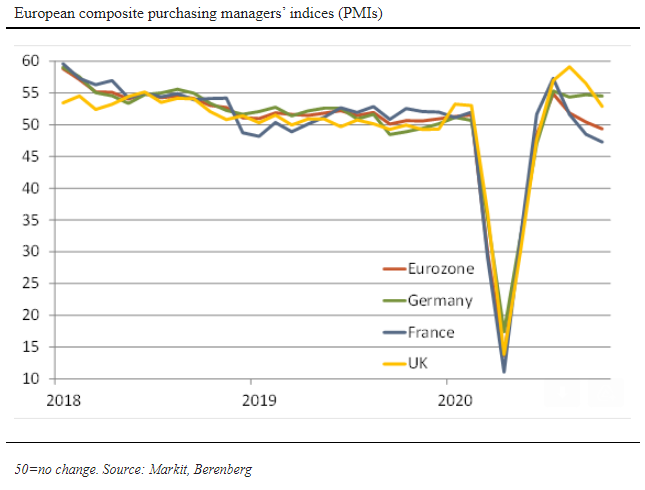

IHS Markit’s flash services PMI for the Eurozone fell from 48.0 to 46.2 in October, below the 47.1 anticipated by consensus, after Germany’s services sector saw its national PMI fall back below the 50.0 threshold that separates denoting industry expansion from those warning of contraction.

For Germany’s economy this was more than offset by sharp gains for manufacturers, who saw their PMI rise 46.4 to 58.0, which then helped to lift the Eurozone manufacturing PMI from 53.7 to 54.4.

But for the Eurozone as a whole the services sector matters enough for losses there to have pushed the bloc's composite PMI lower from 50.4 to 49.4.

That leaves the broadest barometer of the bloc’s overall economic momentum languishing at recessionary levels again.

“The wave of curfews and other social distancing rules to contain the near-exponential surge in coronavirus infections is taking their toll on the European economy,” says Florian Hense, an economist at Berenberg.

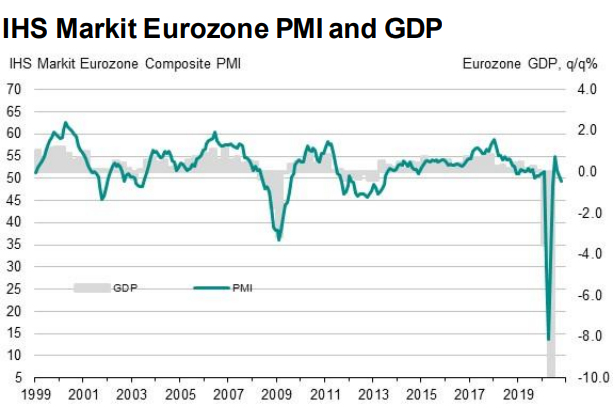

Above: Source: IHS Markit.

“For now, we have to treat the PMI data with some degree of caution and judge them in combination with the broader and more detailed surveys such as the German Ifo (due on 26 October) and the European Commission’s sentiment index (due on 29 October) to assess the performance of the European economy in October,” Hense adds.

PMI declines are a warning of turbulence ahead as increasing numbers of governments in Europe tighten restrictions on social contact and business activity in response to a surge of coronavirus infections, with Germany, France, Spain, Netherlands and Sweden among others having made meaningful changes.

PMI surveys measure changes in industry activity by asking respondents to rate conditions for employment, production, new orders, prices, deliveries and inventories. A number above the 50.0 level indicates industry expansion while a number below is consistent with contraction.

They often correlate well with GDP growth but also come with a health warning having frequently under or overestimated turns in activity. Steep earlier falls are also thought to lessen their reliability given the structure of the surveys used.

“Virus trends over the next few weeks will matter much more for the Q4 outlook than any economic survey for October. We base our call for near-stagnation rather than a decline in Q4 GDP in the Eurozone and the UK on the assumption that the restrictions that are being imposed now will contain the spread of the virus with a lag of roughly two weeks. If daily infection rates continue to rise beyond early November, GDP would likely contract noticeably in Europe in Q4.”

Source: Berenberg.

Eurozone coronavirus infections have grown exponentially, alongside both an increase in testing capacities as well as a loosening of earlier more draconian restrictions that saw much of the continent placed in ‘lockdown’ for months.

But after a strong rebound in the third quarter from the resulting historic second-quarter trough, the recovery was already expected to lose momentum even before curbs on social contact and some businesses were tightened again.

Berenberg estimates that final quarter Eurozone GDP could fall meaningfully if the current impositions are maintained more than another fortnight, before the rebound resumes again in December or the first quarter of 2021.

The risk might be on downside, at least in the UK, given that politicians have continued to call for a return to the all-out ‘lockdown’ of the first half and the government has warned of tighter, more widespread curbs.

“We expect a stagnation in all but name relative to Q3. The growth we still project for Q4 reflects a statistical overhang from a still solid September rather than further gains from October through December,” Hense says. “A new wave of much harsher restrictions to contain the spread of the virus would likely force us to revise our base case and further downgrade our near-term economic outlook. But even in that case, the setback would have to be extreme to invalidate our big picture story that, following the Covid-19 recession, the advanced world has entered the sweet phase of a new business cycle."

Hence and the Berenberg team look for Europe’s manufacturing rebound to continue, aided by an economic recovery in China, and suggest that a final quarter setback might need to be larger than the -11.8% seen in the second quarter in order to fully derail the recovery.