Image © Adobe Images

The UK recovery has been placed on ice already by fresh government restrictions on activity, according to Capital Economics, although the risk is that further measures are implemented in the coming weeks and send the economy into reverse during the final quarter.

Pubs, gyms and some other hospitality businesses were instructed to close in the Liverpool City region this week, where residents joined those of other areas in the North that had already been subjected to enhanced interventions from London, although this could be just the tip of a winter iceberg.

“New COVID-19 restrictions will put the economic recovery on ice for the next few months and will prevent the economy from climbing back to its pre-crisis level until the end of 2022. The possibility of even tighter COVID-19 restrictions and of a no deal Brexit at the end of the year mean there’s a risk that the recovery goes into reverse,” says Paul Dales, Capital Economics' chief UK economist.

Dales’ prognosis was given in a Tuesday research briefing but already further and even more damaging restrictions have been rolled out elsewhere in the UK, adding to measures announced for the North of the country by Prime Minister Boris Johnson on Monday.

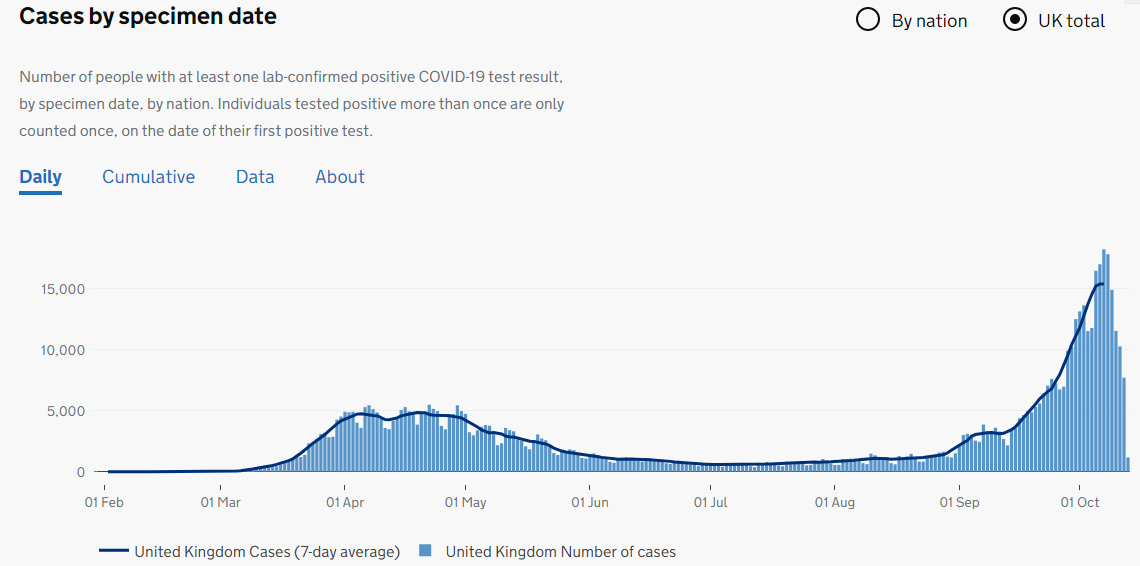

Source: UK Government.

Northern Ireland ordered the closure of schools, pubs and restaurant businesses on Wednesday as part of its own coronavirus containment effort, with the announcement coming as Welsh officials toyed with the idea of similar measures for the UK’s third largest national economy.

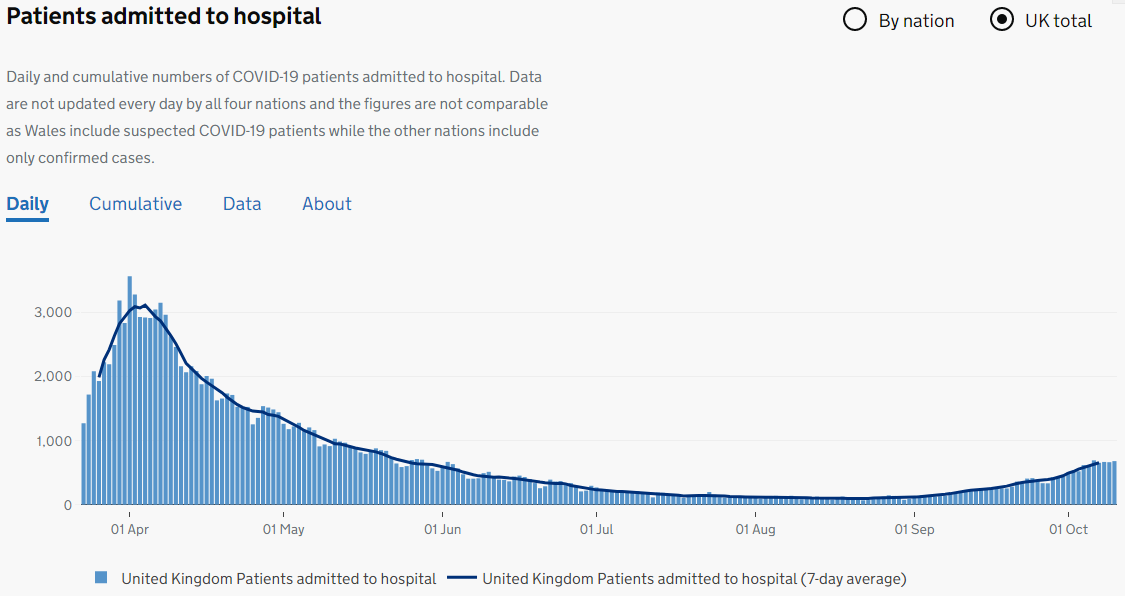

Source: UK Government.

Restrictions are tightening in response to a second wave of coronavirus that at least purports to be larger than the first, although hospitalisations and fatalities are far lower than in the initial outbreak.

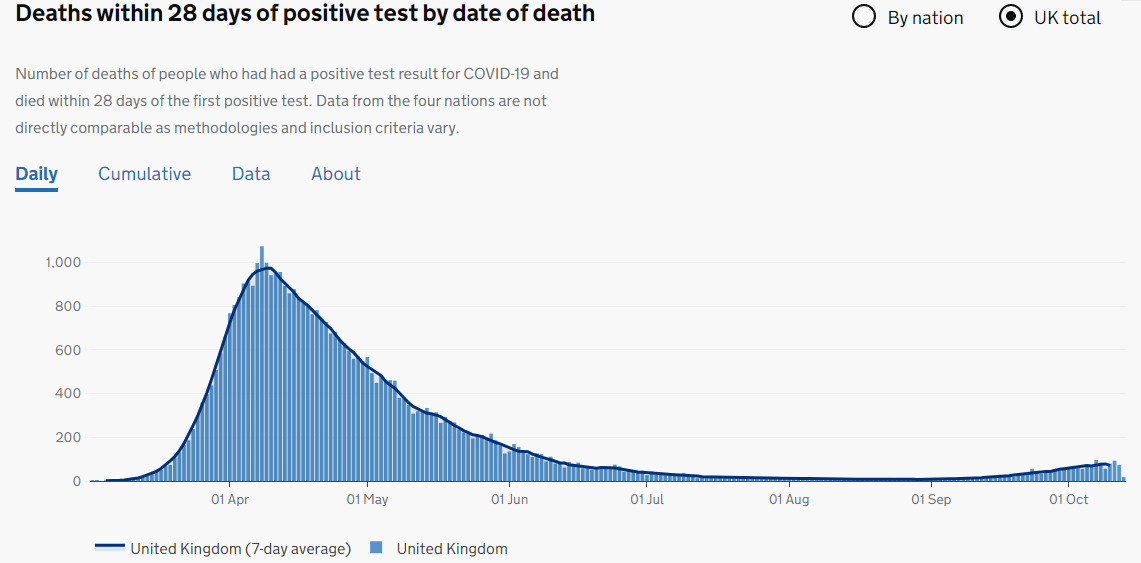

Source: UK Government.

The economic recovery was already slowing but now faces further setback and the winter period is only just beginning.

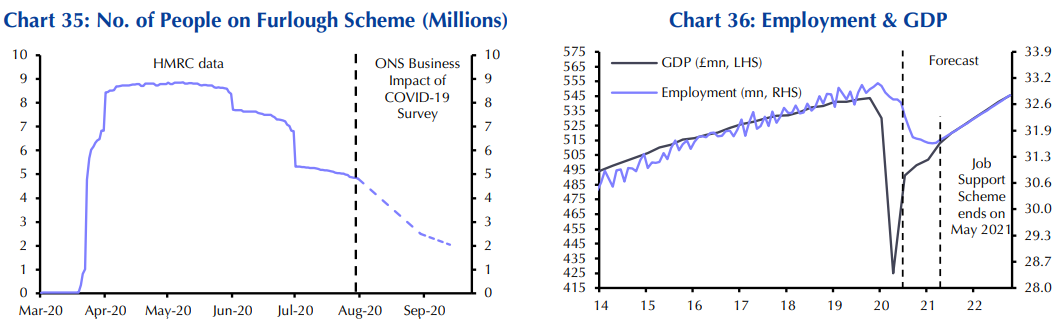

“This next phase of the recovery will be more painful for households and businesses,” Dales says. “Although the government’s new Job Support and local lockdown furlough schemes will cushion some of the blow from the end of the national furlough scheme, the jobless rate will probably still rise from 4.5% in August to almost 8.0% during next year.”

GDP growth was just 2.1% in August when economists had looked for a larger 4.6% increase, and despite a more-than one percentage point gain from Chancellor Rishi Sunak’s innovative Eat Out to Help Out scheme.

August saw the recovery slow from an earlier 6.6% pace of growth around the same time that cracks began to appear in the job market, where unemployment rose from 4.1% to 4.5% for the three months to the end of September.

Source: Capital Economics.

Still however, the millions of jobs that are at risk from government measures are currently being kept alive by the HM Treasury furlough scheme that ends with October only to be replaced by a less generous alternative.

Many economists see this as a catalyst for a winter surge in unemployment that would be sure to add to the economy’s woes and weigh heavier on the recovery.

“Overall, the economy is entering a harder and slower phase of the recovery,” Dales says. “We now think that GDP won’t rise at all in the last three months of the year and won’t get back to its pre-crisis peak until the end of 2022. That’s based on our assumptions that the new restrictions are tightened a bit further, that they last in some form for at least six months and that a “thin” Brexit deal is agreed before the status-quo transition period ends on 31st December 2020.”

It’s not clear how far the government is willing to go in its bid to contain the coronavirus, but already Prime Minister Boris Johnson is claiming not to want a second national ‘lockdown’ while simultaneously alluding to the possibility of a government attempt to impose one.

But what’s certain is that irrespective of whether the economy is further encumbered by more measures or not, businesses and households will not be able to count on HM Treasury in the same way as they could previously.

Source: Capital Economics.

Eat Out to Help Out ended with the August month while October 31 marks the transition to a less generous furlough scheme that pays only two thirds of salaries to employees of shuttered businesses, which are set to receive as compensation for the troubles, government grants of a mere £3,000 per month.

“There is a risk that many of the 2 million or so people who in mid-September were still on partial or full furlough lose their job when the national scheme is wound down at the end of October. That’s particularly the case in the light of the tightening restrictions to stem the resurgence in new COVID-19 cases that will hamper the economic recovery,” Dales warns. “Although the MPC has already cut interest rates to 0.10% and raised the stock of announced QE from £475bn to £775bn this year, our forecast of sustained high unemployment suggests it will have to do more.”

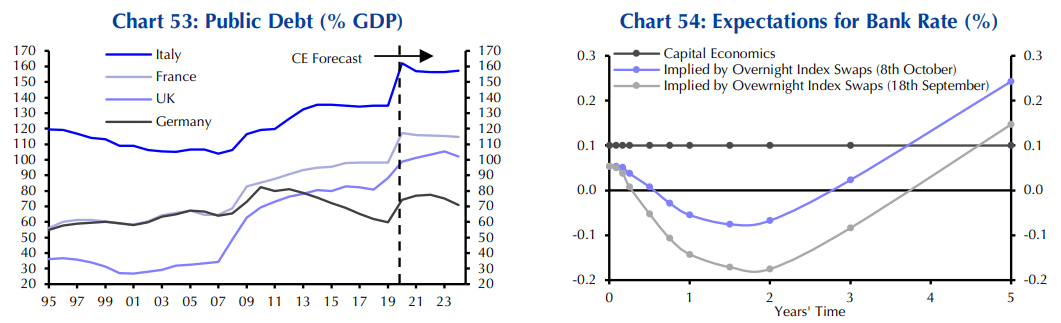

Dales and the Capital Economics team forecast the Bank of England (BoE) will leave Bank Rate at 0.10% for at least five years and increase the quantitative easing (QE) programme under which it buys government bonds by a further £250bn over the next year as a result of damage done to the economy and the resulting extraordinary funding requirements of the government.

Source: Capital Economics.

More QE will reduce government funding costs, although only by negligible amounts given that bond yields are either negative or next to zero across much of the maturity spectrum or ‘yield curve’. On Wednesday market prices implied that investors and savers would have to lend the government money for a 30-year period simply in order to earn 0.77% per year.

The BoE’s anticipated actions will however, do almost nothing whatsoever to ease the current burden for the average business and household.

Not least of all because monetary policy works with a lag of up to two years, but also because of the negligible level of existing borrowing costs and the fact that loans are only made to businesses which are perceived by lenders to be viable. The viability of all businesses is called into question by the government’s approach to coronavirus containment.

“New fiscal measures and the slowing recovery mean that government borrowing will probably reach £390bn this year (20% of GDP),” Dales says. “That would be the highest budget deficit since WWII. The deficit is likely to come down quite quickly as the hit to activity and tax revenues should be shorter than in the financial crisis, and many of the most expensive support schemes have already ended. Our forecast is that the deficit will fall to 9% in 2021/22 and to 7% in 2022/23.”