- ECB mulls “make-up strategies” to compensate for missed targets.

- Aka a symmetric interpretation, or averaging approach to inflation.

- Comes as review into ECB’s monetary policy strategy is renewed.

- Hints at perpetual ice age for Eurozone interest rates & savers.

European Union blue flag and German flag waving in front of Federal Constitutional Court building Bundesverfassungsgericht the supreme court for the Federal Republic of Germany

Savers could be facing a perpetual ice age of zero interest rates as policymakers covet a return of long-lost inflation pressures, European Central Bank (ECB) President Christine Lagarde hinted on Wednesday.

President Lagarde said at the ECB Watchers conference in Frankfurt that policymakers will consider whether to adopt so-called make-up strategies when continuing a now-renewed review into how the Eurozone’s central bank conducts its interest rate and quantitative easing policies.

The bank is charged with using its policy levers to foster annual inflation that is “below, but close to, 2%” over the ‘medium-term,’ which is a subjective and so flexible period of time that furnishes the bank with necessary discretion over when to lift rates to ward off rising price pressures or take action to lift inflation.

“The wider discussion today, however, is whether central banks should commit to explicitly make up for inflation misses when they have spent quite some time below their inflation goals, Lagarde told an audience hosted by the Institute for Monetary and Financial Stability, a part of Goethe University Frankfurt. “While make-up strategies may be less successful when people are not perfectly rational in their decisions – which is probably a good approximation of the reality we face – the usefulness of such an approach could be examined.”

The ECB’s framework review is expected to conclude by the middle of next year, later than originally intended after having been placed on hold by the pandemic, although the outcome of an equivalent period of self-reflection at the Federal Reserve (Fed) in America and Lagarde’s references to “make-up” strategies are a good indication of what the outcome might be.

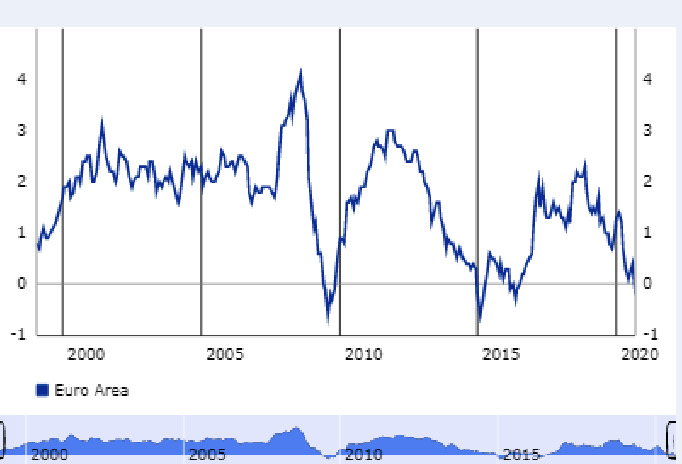

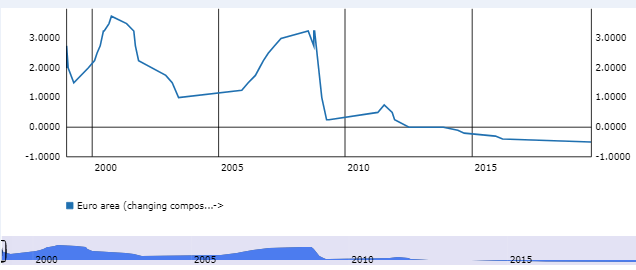

Above: Eurozone inflation. Source: European Central Bank.

Chairman Jerome Powell said from Jackson Hole in Wyoming back in August that Federal Reserve rate setters will now adopt an average-inflation targeting approach that sees the world’s pre-eminent central bank actively seeking to cultivate an inflation rate that is then allowed to exceed the 2% target for as long as price pressures have undershot it.

It’s far from clear that the Fed was sincere in that commitment, not least of all because Federal Reserve Bank of Chicago President Charles Evans then said in September that policymakers might still choose to raise interest rates before inflation even reaches 2%. The Fed has a history of doing that, most recently in response to tax cuts announced by President Donald Trump and before then, back in December 2015 when the U.S. economy and labour market were still recuperating from the financial crisis.

Nonetheless, it’s this kind of policy that Lagarde was likely referring to.

“A client asked us “If Christine Lagarde did a "Powell" and promised an average 2% inflation over time, would you then laugh or cry?,” says Andreas Steno Larsen, chief FX strategist at Nordea Markets in an August note to clients. “Core inflation is en route for new post 2000-lows according to our model framework. With an average core inflation below 1%, would anyone even take it barely seriously if Lagarde were to announce an AIT regime in Europe? Probably not.”

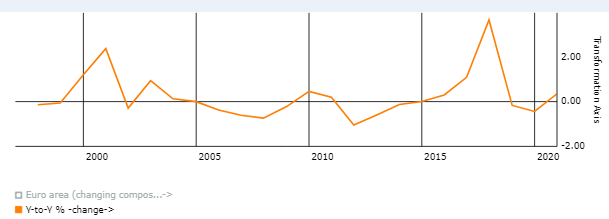

Above: Eurozone annual inflation rate excluding energy and unprocessed food. Source: ECB.

The upshot for the layperson and the average household from Wednesday’s speech is, if anything, that savers and interest rates could be facing an even longer ice age than before and one that could yet stretch into perpetuity.

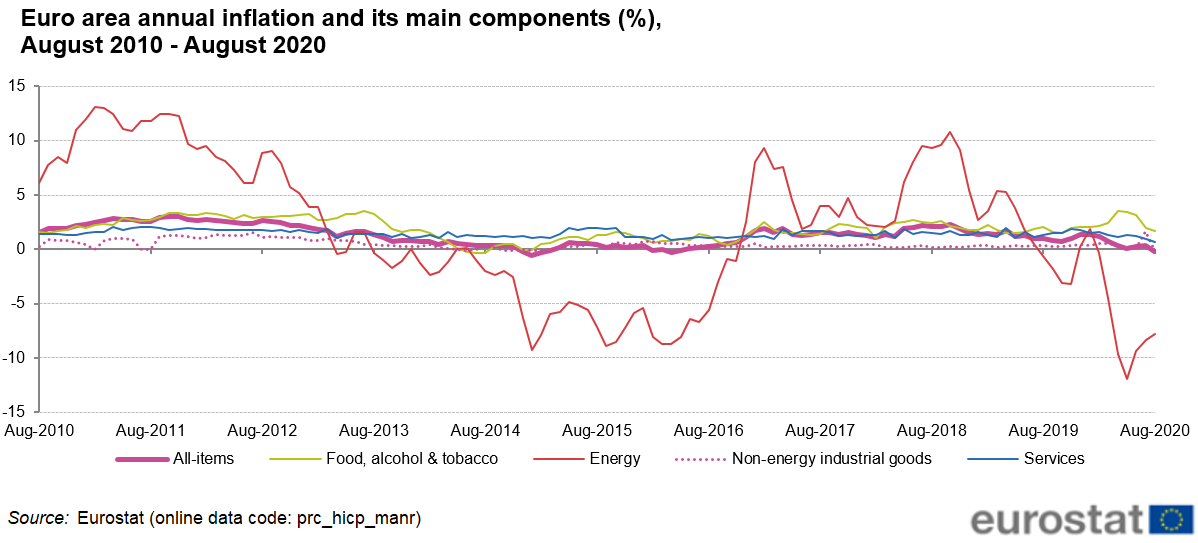

Fluctuations in oil prices have in recent years, and from time-to-time, contrived the appearance of an ECB that has met its inflation target.

But if the more-important ‘core inflation’ rate, which ignores volatile energy and food costs, is taken as the better approximation of price pressures faced by participants in the economy then the ECB has not met its inflation target since it and the Euro were born before the turn of the Millennium.

Rate setters might be tempted to, or even heard claiming that such an outcome - of low and often seemingly stable inflation - results from their own policymaking expertise and the technocratic operation of one half of society’s financial and economic power levers - interest rates - that has been a dominant fashion the world over in the last two decades.

Lagarde’s Wednesday contemplation of the Eurozone inflation landscape demonstrates that such belief or claim would be both inaccurate and foolhardy.

“Broadly speaking, three factors might explain why inflation responded so weakly,” Lagarde says, referencing inflation declines that have persisted even as and after one of the world’s largest central banks all-but exhausted its armoury in a fruitless pursuit of still-elusive inflation pressures.

Lagarde floated the possibility that “economic slack” may be larger than the bank perceives and mismeasured in the policymaking process, as a reason for persistent inflation weakness.

Conventional thinking dictates that inflation rises and falls in response to both supply and demand pressures in each case. This has been consistently borne out in economic history, although not so much in the new Millenium.

“Persistent structural forces” like technological change may have impacted the relationship between spare capacity in the economy (unemployment and underemployment) and inflation, Lagarde suggested on Wednesday, echoing a theory that’s proven popular among economists.

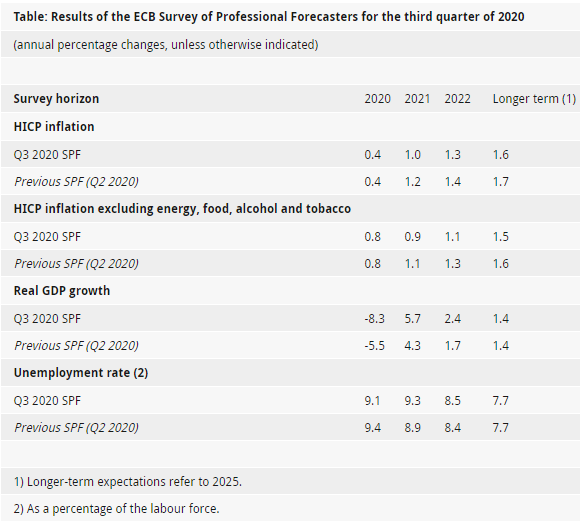

Above: ECB survey of inflation expectations. Third quarter 2020.

In addition, the “anchoring of inflation expectations might have loosened,” Lagarde said in tacit reference to a possible loss of market and public confidence in the ECB's ability to deliver higher inflation.

A so-called de-anchoring of inflation expectations would risk encouraging a self-perpetuating cycle of falling inflation expectations that then help to beget yet more declines in actual realised inflation, which would bring the spectre of ‘Japanification’ of the Eurozone a step closer.

“None of the recent rhetorical posturing from key ECB officials suggests investors need to worry much about 'QE disappointment risk' on this side of the October decision,” says Stephen Gallo, European head of FX strategy at BMO Capital Markets. “There is a reasonably good chance that the central bank will continue to soak up most (if not all) government net issuance through year-end.”

The ECB cut its main interest rate to zero in March 2016, where it remained on Wednesday. This was after reducing to below zero the deposit rate it used to pay commercial lenders who park money with it.

Officials often assert that they aren’t out of ammunition but with the derivative market aside, economists and observers all doubt the bank would want to cut rates further for fear of destabilising the banking sector.

Above: Deposit rate once paid but now charged to commercial lenders parking money at the ECB. Source: ECB.

Instead, the ECB has resorted increasingly to buying European government bonds under a quantitative easing programme that has been deeply controversial in parts of the bloc, notably its biggest financial backers like Germany and the Netherlands. Despite precious little evidence that such policies have been effective in generating inflation anywhere they’ve been tried.

The Federal Reserve and the Bank of England (BoE) were among the first to adopt QE and are the only two G10 central banks to have had the luxury of contemplating how best to head off above-target inflation pressures during this last and ultimately lost decade for prudent savers.

But these inflation privileges resulted not from QE or any other form of divine technocratic ability or policy innovation, but rather from electoral choices that arguably, neither central bank ever wanted to see made.

The Fed’s hasty 2018 interest rate rises came in response to exorbitantly costly tax cuts from President Donald Trump, the economic benefits of which were partially squandered by a panicky Federal Open Market Committee.

This is while the BoE has the Brexit vote, which it often subtly lamented, to thank for its November 2017 and August 2018 interest rate hikes.

In effect Wednesday’s speech shows that monetary policy is, for the time being at least, reduced to a game of poker in which technocrats contrive the illusion of influence and control over matters they readily acknowledge an imperfect, if-not absent understanding of. All the while fretting in private, and sometimes public, about what to do in response to the next disinflationary economic shock.