- UK seeing a v-shaped recovery says Haldane

- But risks tou outlook skewed to the downside

- Bank ready to act again if necessary

Above: File image of Bank of England Chief Economist Andy Haldane. Image courtesy of the Bank of England, accessed Flickr. Reproduced under CC conditions

The UK economy is currently experiencing a v-shaped recovery, that should be reinforced by a surge in consumer spending when pubs and restaurants open up on July 04, says the Bank of England's Chief Economist Andy Haldane who has given an update on how his team of economists see the UK's economic recovery progressing.

Haldane said that although the economic recovery might be running ahead of schedule, the risks to the outlook remained skewed to the downside and as such he would back any further interventions by the Bank to protect the economy and financial system, even though he believes the Bank is running out of road.

"There is a debate about which letter of the alphabet will best describe the path of the economy, with some scepticism about the V-shaped scenario path in the Bank’s May Monetary Policy Report (MPR). It is early days, but my reading of the evidence is so far, so V," said Haldane in a speech delivered to an online webinar.

Haldane's address revealed economists at the Bank of England might have underestimated the pace of recovery in the UK, particularly that related to consumer spending where data suggests activity is recovering faster than had been anticipated.

Economists now expect consumer spending to be around 20% lower in the second quarter of 2020, relative to the nearly 30% they had officially forecasted in May's Monetary Policy Report. By the end of the second quarter the Bank believes spending is likely to be around 10% lower than at the start of the year.

"Or, put differently, consumer spending in the UK is probably already above the level projected to prevail in Q3 in the May MPR scenario," says Haldane.

Driving a recovery in spending was the opening-up of non-essential retail stores on 15 June which was "quantitatively significant" as it represents around 13% of consumption spending and halving the share of goods and services consumers which were previously unavailable.

Bank economists note that initial indications from payments and footfall figures suggest this opening-up has accelerated, perhaps significantly, consumer spending.

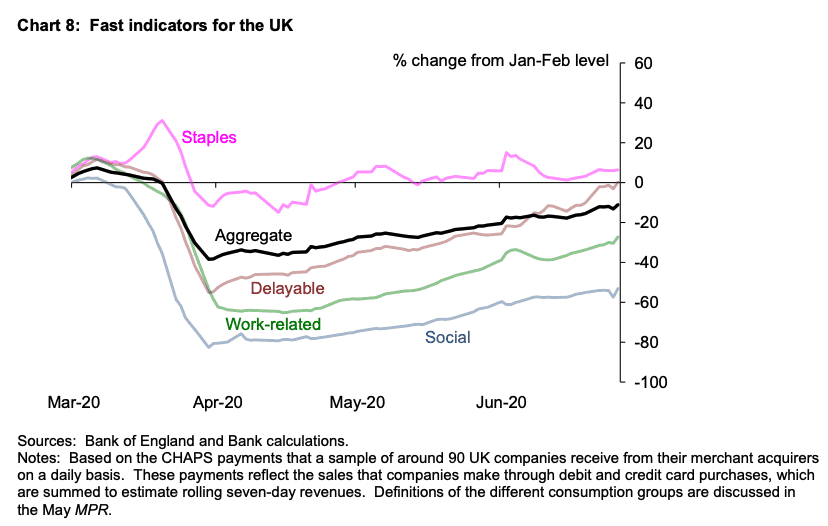

In particular, CHAPS data suggests spending on delayable goods has now returned to pre-Covid levels, well ahead of the corresponding May scenario profile.

Haldane says 'fast indicators" used to track the collapse in activity in the first part of this year can also be used to track its recovery.

"Generally speaking, these indicators suggest the recovery in both the UK and global economies has come somewhat sooner, and has been materially faster, than in the MPC’s May MPR scenario – indeed, sooner and faster than any other mainstream macroeconomic forecaster," says Haldane.

Concerning the outlook, Haldane says there is a potentially a significant degree of pent up consumer demand that will further aid the pace of the economy's recovery.

"Looking ahead, the opening of pubs, restaurants, hotels, cinemas and other hospitality outlets on 4 July will provide further impetus to spending. My own market intelligence suggests considerable pent-up demand. Together, these categories represent around another 10% of consumer spending. Initial reports from businesses in these sectors, including from the Bank’s Agents, suggest advance bookings are brisk," says Haldane.

Haldane however cautions that consumer spending is just one element of the UK economy, even if it is a significant component, and there is little data available on other key areas such as investment.

"For housing and business investment, there are even less data on which to make an assessment," says Haldane.

The Bank's economic forecasts made in May suggested peak-to-trough falls of 60% and 40% respectively, based in part on results from the Bank’s Decision Maker Panel (DMP). The latest results from the DMP appear broadly consistent with this.

The Bank of England's Nowcast model - which is designed to give an up to date snapshot of economic growth - forecasts a fall in second quarter GDP of around 20% relative to its pre-Covid peak.

"While this is an exceptionally weak number, that is not in itself news. The news is that it is 7 percentage points less than in the May MPR scenario," says Haldane.

There are however concerns as to how the employment scenario plays out in the third quarter, with Haldane expressing concern that the number of employees that are not rehired after the furlough scheme is ended is greater than had been anticipated.

"The May MPR scenario had unemployment rising to 9%, but assumed the risk of workers not being re-hired was small. Recent survey evidence, from both households and companies, suggests this risk could be larger. For example, survey evidence of companies by the DMP suggests private sector employment could be almost 10% lower by the end of 2020, implying an unemployment path somewhat higher than in the May MPR scenario," says Haldane.

If unemployment is greater than expected there could be a negative hit to spending in the third quarter, which would likely delay the pace of the economy's recovery.

However, it is believed that should firms expect a greater pick up in demand over coming months they might be hesitant to let staff go, noting that rehiring is more expensive than holding onto staff in order to ride out short-term dips in activity.

Indeed, while Haldane sees the recovery as being relatively robust at present, the risks to the outlook are ultimately skewed to the downside in his view and this could invite further intervention from the Bank of England.

"Looking ahead, risks to the economy remain considerable and two-sided. Although these risks are in my view slightly more evenly balanced than in May, they remain skewed to the downside. Of these risks, the most important to avoid is a repeat of the high and long-duration unemployment rates of the 1980s, especially among young people. Like the rest of the MPC, I stand ready to adjust monetary policy, at speed, if needed to support the economy and return inflation to its target on a sustainable basis," says Haldane.

However, Haldane gave a clear warning that the Bank's ability to support the economy has shrunk owing to the significancy interventions already announced, warning that the Bank cannot be relied on to offer an indefinite source of support.

"With interest rates along the yield curve close to zero, there is also simply less room for monetary manoeuvre than in the past," says Haldane.