Image © Gov.uk

- Spot rates at time of writing: GBP/EUR: 1.1287, -0.82% | GBP/USD: 1.2681, -1.09%

- Bank transfer rates (indicative): GBP/EUR: 1.0972-1.1061 | GBP/USD: 1.2311-1.2400

- Specialist money transfer rates (indicative): GBP/EUR 1.1097-1.1165 | GBP/USD: 1.2464-1.2540 >> More details

The government’s maiden budget has been widely credited with backstopping the economy against a mounting coronavirus crisis while also positioning the UK for faster growth in future years, but it’s met with a mixed reaction from currencies and economists alike, who’re increasingly making their views known.

Chancellor of the Exchequer Rishi Sunak announced the newly elected government’s first budget on Wednesday to much fanfare, revealing a range of measures that were presented as lifting spending across the board and marking a break with the austerity of the past.

Sunak’s policy announcements came in the shadow of a large and “in concert” monetary stimulus from the Bank of England (BoE) aimed at supporting the economy as authorities and citizens brace for a possible coronavirus epidemic on home shores. And it also followed an election that raised market expectations for spending in the years ahead, with Prime Minister Boris Johnson having promised investments and funding to lift growth, raise living standards and “level up” the less prosperous north.

Economist expectations were high heading into the announcement and more so after the resignation of former Chancellor Sajid Javid, who was cast as an impediment to the government’s plans to deliver on its election promises. But the Pound saw only a short-lived boost in the wake of the budget, which also failed to put a floor beneath London’s still-crumbling stock markets and the government’s tumbling bond yields that might normally have been expected to rise after a large spending announcement.

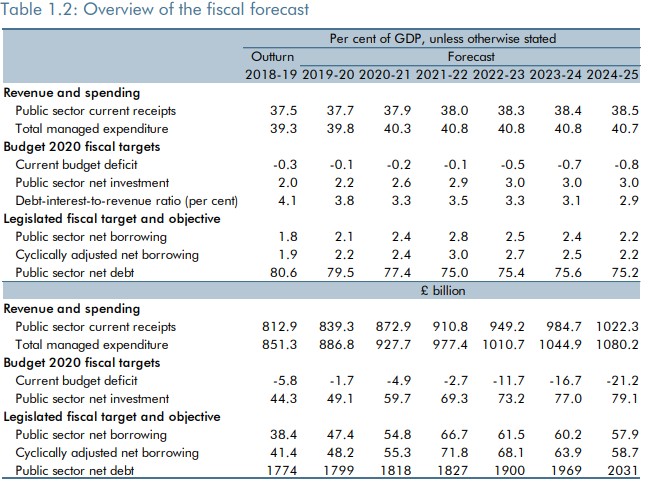

"Bold fiscal action will soften the economic impact of the Covid-19 pandemic and should support sterling," says Kit Juckes, chief FX strategist at Societe Generale. “The OBR's fiscal arithmetic doesn't overly alarm me. Even an independent analysis of the outlook should be treated with a little scepticism but while the forecast for public sector net borrowing rises from 1.8% in 2018/19, to a peak of 2.8% in 2021/22, that is still sufficiently far from the post-GFC peak above 10% that I'm not alarmed.”

Above: Office for Budget Responsibility forecasts and analysis of budget implications for various ratios.

Sunak announced a three-point plan to support to the economy through the coronavirus outbreak, which was declared a pandemic by the World Health Organization on Wednesday, that will see a total of £12 bn of new funding made available to public services and businesses. The National Health Service and local authorities will receive £5bn of new money under the plans while individuals and businesses are in line for relief through tax breaks.

The Chancellor also claimed that when combined with other measures, the economy would receive a £30 bn increase in government spending this year, which is equal to around 1.5% of GDP. And that was before Sunak got to announcing the planned increases in day-to-day spending and investment, which will take effect over the life of the current parliament and have been billed as positioning the economy for faster growth in the years ahead.

Juckes says extra spending contained in the budget will help the UK to outgrow the Eurozone in the coming years and that “bold fiscal action” is made possible by the austerity and restraint of the previous government. He’s told clients to bet on an increase in the Pound-to-Euro rate this year as a result, given that exchange rates are sensitive to changes in bilateral economic growth differential, although others are less excited about the measures unveiled.

“The narrative from the financial press and the OBR was that yesterday's announcements constituted a sizeable new easing of fiscal policy. This is misleading in our view. Yesterday's increased borrowing numbers largely reflect old news: namely spending announcements made since the OBR's last set of forecasts in March 2019, not fresh money,” says Sanajay Raja, an economist at Deutsche Bank. “While the MPC rolled out a range of policy measures to shore up financial conditions, the Treasury's response was far more limited than we expected with the increase in the rate of fiscal easing limited to approximately GBP 7bn of emergency measures from the Chancellor.”

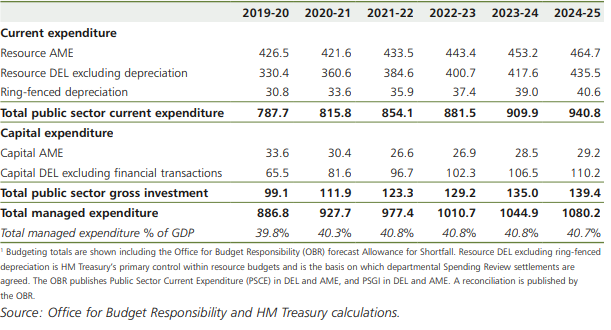

Above: HM Treasury projections day-to-day spending, public investment and total government spending.

Sunak says day-to-day spending will rise by £100 bn over the life of this parliament and that July’s Comprehensive Spending Review will deliver an uplift in this category from £360.6 billion per year in 2020-21 to £417.6 billion by 2023-24.

Public-sector-net-investment will rise to £640 bn for the five-year parliament after annual spending rises from 2.2% of GDP to 3%, and when combined with everything else, those measures are expected to take the government’s share of spending in the economy up from 39.8% of GDP last year to 40.7% in 2025.

But Deutsche Bank’s Raja says the budget has delivered plans for little additional spending that wasn’t already he expected by the market. He cites earlier market expectations for government borrowing to rise by £13bn more this year than it will do under the new plans as being behind the muted response to Wednesday’s budget. Deutsche Bank estimates the government has “left significant amounts of cash on the table” that could be worth as much as £70bn.

“We would focus on the near-term. Medium term plans can and probably will change. Likely growth downgrades will raise borrowing, for instance. And the Chancellor started a review that will in our view eventually result in more medium-term spending. That is for another day. Today the key point is a large near term stimulus that targeted all the right areas: extra health spending through guaranteeing loans to small businesses to enhancing sick pay and business rates relief. This helps justify the growth bounce-back we forecast for late 2020,” says Robert Woods, an economist at BofA Global Research.

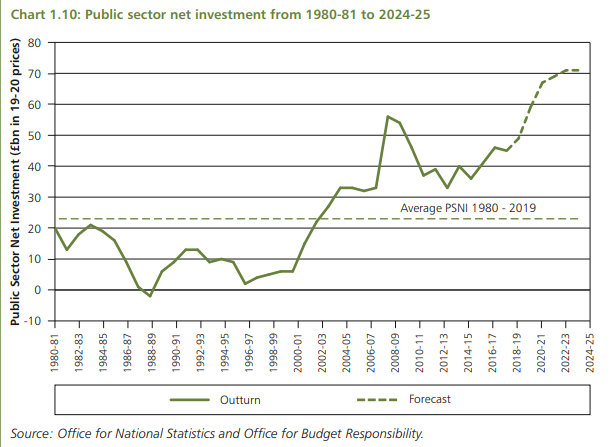

Above: HM Treasury projections public investment as a percentage of GDP.

The budget and Thursday’s reactions to it come as the Prime Minister and cabinet host an emergency meeting that is expected to result in the government moving to the “delay” phase of its coronavirus management strategy, from the current “containment” phase, which could see more home working encouraged and unecessary travel discouraged as part of a “social distancing” strategy.

This is after coronavirus infections lept to nearly 500 on Wednesday, with nine dead in the UK and as the viral pneumonia prompted other governments to take increasingly stringent measures in order to contain outbreaks of the disease that were labelled a pandemic by the World Health Organization.

Efforts to combat the disease are stepping up in order to protect health systems from collapse amid increasing hospitalisations in some countries, although they’re expected to deal a severe blow to the affected economies in at least the first and second quarters.

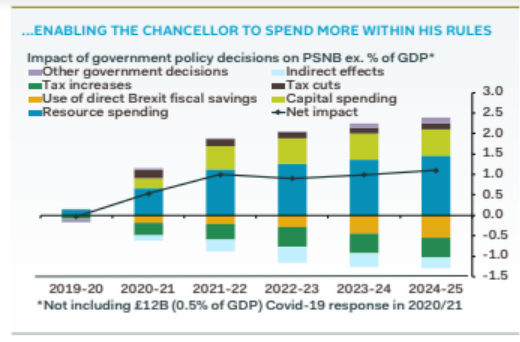

“Chancellor Sunak’s “temporary, timely and targeted” fiscal response to the Covid-19 outbreak, and the BoE's accompanying stimulus measures, won’t prevent GDP from falling over the next couple of months. But they greatly improve the chances that the economy rebounds later this year,” says Samuel Tombs, chief UK economist at Pantheon Macroeconomics. “The Chancellor also went on a long-term spending spree…. Our chart below shows that he signed off a discretionary boost equal to 0.5% of GDP in 2020/21 and 1.0% in 2021/22, relative to the prior baseline. Most of the 2020/21 uplift had been announced in the Spending Round in September, but the additional 0.5% of GDP uplift in 2021/22 was new money.”

Above: Pantheon Macroeconomics graph showing contributions of budget measures to GDP.