Image © Adobe Images

- Q2 GDP shouldn’t be so low says data provider

- Could be a result of ‘smoothing’ Q4’s sharp drop

- All sectors, bar services, are performing well

The slowdown in China may not be as bad as recent GDP data suggests, says a leading authority on the Chinese economy.

Recent data showed the Chinese economy grew by a slower 6.2% rate in Q2, the slowest rate of growth since 1992, yet the data may not be reflecting an accurate picture of the true state of the economy, says Leland Miller, the CEO of China’s Beige Book.

China's Beige Book is a provider of survey-based data on the Chinese economy derived from interviews with 3300 Chinese firms which help paint a clearer picture of the Chinese economy's performance.

“I think the key here is that China’s GDP data is never accurate, there is a lot of reasons, but not all of it is political manipulation, some of it is simply lag, sometimes it takes a long time to collect the data,” says Miller.

Another reason for the inaccuracy is Chinese authorities’ habit of smoothing out dips in the data over subsequent reporting periods so as to disguise sharp falls.

In Q4 2018, for example, the Chinese economy suffered quite a sharp set-back due to the impact of trade tariffs but this was probably disguised by smoothing the drop over subsequent quarters, including Q2, which explains why the result may have been artificially low.

“When the Chinese see a particular problem period in the economy like the 4th quarter of 2018, they don’t want to show that growth indicators have fallen off a cliff so they smooth it out, they spread the weakness till later. A lot of what you are seeing right now as being reported is weakness, which we saw earlier in the year, is what we saw 4th quarter 2018. We are seeing much better metrics in our own data,” says Miller, in an interview with Bloomberg news.

The state of the Chinese economy is significant from an FX perspective because it has a direct impact on the Australian Dollar - often seen as a proxy for the Yuan - the new Zealand Dollar since most NZ trade is now with China, and safe-haven currencies such as the Yen and the Swiss Franc.

The antipodean currencies are positively correlated to the state of the Chinese economy, the last two are negatively correlated since they benefit when global investor sentiment breaks down.

As far as sectoral performance goes, all of China’s major sectors are doing well bar services, says Miller: “Manufacturing and retail are outperforming right now, services is going through a bump, property is doing fine.”

Retail is doing particularly well, says the Beige Book CEO, and his assertion seems to be backed up by recent earnings data from luxury clothes brand Burberry, whose profits in Q1 were driven mainly by double digit growth from Chinese consumers.

Indeed, not all the data released from China on Monday was bad - apart from GDP, retail sales, fixed asset investment and industrial production data for June were also released and they all beat forecasts.

Whilst some analysts argued the retail sales print was artificially high because of aggressive car sale discounting the numbers nevertheless support the notion that underneath the data the Chinese economy remains resilient.

The China Beige Book CEO is not the only person arguing perspectives on China are overly negative.

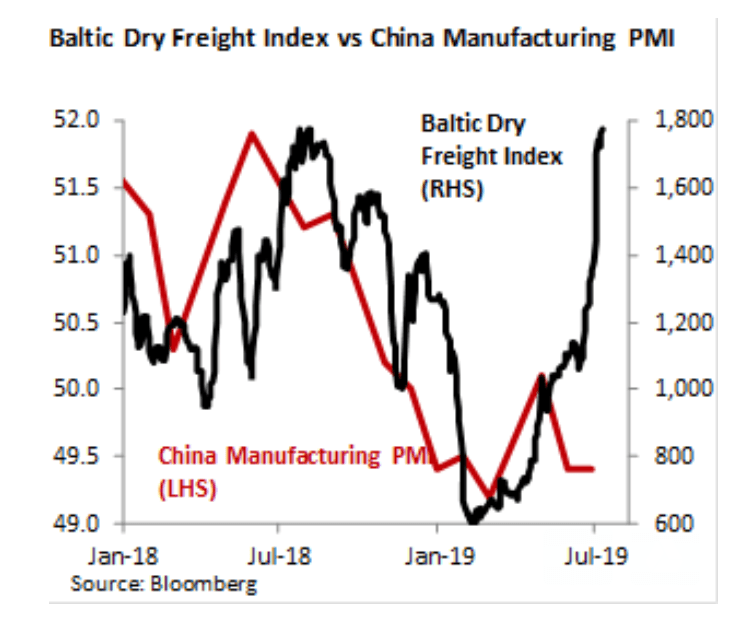

Taimur Baig, chief economist, at DBS group in Jakarta recently put out a note highlighting the high degree of correlation between the Baltic Dry Freight Index (BDFI) and Chinese Manufacturing.

Although the official Chinese data is showing a contraction in Manufacturing the rise in the BDFI in 2019 suggests Chinese manufacturing may be bottoming out and due a recovery.

“Looking at Chinese PMI data and global freight rates, we see some signs of stabilisation, perhaps even a rebound in June,” says Baig.

The Baltic Dry Freight Index tracks the cost of shipping freight. It is a reliable leading indicator of Chinese Manufacturing as can be seen from the chart above, and suggests that the current low readings for Chinese official and Caixin PMI data could change.

Another aspect of the Chinese economy which has raised concerns is the provision of credit which some economists have argued is now drying up. Yet this too is inaccurate, says Beige Book’s Miller, whose survey data shows quite the opposite.

“We have found an extremely active credit environment for all of 2019. So there is a lot more credit going out, so it shouldn't surprise people that there is more growth from it, because I think the Chinese are a lot more aggressive now than I think people think,” says the Beige Book CEO.

Part of the reason China is actually doing alright is that the Chinese government moved very quickly to support the economy at the end of its bad quarter in Q4.

The authorities prepared the economy for the worst case scenario, pumping in more support than was necessary, just in case the U.S. expanded tariffs on all Chinese imports. They may have overcompensated.

“Part of it is that the trade war is in a stalemate right now. The Chinese prepared their economy back in Q4 2018 to try to deal with a nightmare scenario. If President Trump went all 25% on all plus 500bn they wanted to be able to cushion the blow. That’s not happening right now and it doesn't look like it is happening anytime soon,” says Miller.

Nevertheless, looking out over the long-term and China’s worst-case- scenario over-preparation may come back to haunt them.

“Here’s the problem, every time the Chinese do what they are doing right now, they are kicking the can down the road. It means they are putting a lot of their credit into the riskier and riskier borrowers they are going to get a worse return on investment. That means growth is going to slow more in the future. So they are creating major obstacles in order to be able to fix this, next year and the year after,” says Miller.

Overall, however, the situation based on the Beige Book’s stats looks a lot better than the official data and suggests fears of a hard-landing may be overdone.

“Things are looking better. That doesn't mean they are great. It doesn't mean there isn't pressure from the trade side but it does mean that this entire narrative that’s been read off the headlines is overly confusing,” says Miller.