Image © Adobe Stock

Research from HSBC shows why the war in the Middle East has proven to be a significant headwind to the Swiss Franc.

Of the currencies most negatively impacted by the war in the Middle East, the Swiss Franc stands out as a curious case: it's amongst the G10's most prominent laggards.

Underperformance is surprising given the Swissie is the ultimate safe haven, a go-to during times of geopolitical conflict and heightened inflation expectations.

To be sure, the franc jumped when the Iran conflict broke out, in a typical knee-jerk reaction, but it soon turned tail. Betting on the franc at the start of the war will have proven a costly mistake: it's down 3.70% from its highs against the pound, 2.25% lower against the euro and 3.70% lower against the dollar.

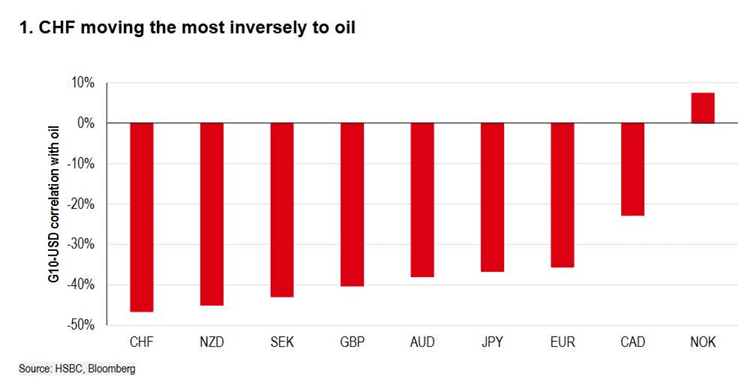

That underperformance is a "recent correlation with oil," says HSBC.

Analysts at the bank say since the beginning of the conflict in the Middle East, the CHF has exhibited the most inverse correlation in G10 FX to daily changes in oil.

"That correlation itself is surprising given oil-GDP intensity is at its lowest in Switzerland compared to the other G10 economies," say analysts.

HSBC says FX intervention fears are oftentimes blamed, particularly with the next SNB meeting only ten days away. But there's little evidence to suggest an active SNB behind the scenes.

The culprit then? Interest rate expectations.

"We believe that episodes of oil prices are leaving the CHF's low yield exposed as 1y1m CHF OIS has only moved c45bp higher since 27 February compared to a G10 (ex. CHF) average of close to 70bp," says HSBC.

That makes some sense: observe the GBP has been one of the better performers during the Iran war. That's because interest rate expectations have risen particularly aggressively in the UK in response to rising oil prices. That bolsters bets that the Bank of England will raise rates, lifting British bond yields.

Switzerland, with its notoriously subdued inflation rates, does not experience the same upshift in rates.

That means Swiss yields are left behind, and in a world where investors are chasing yield, that's a headwind to the franc.