Image © Adobe Images

Bullish bias on the Swiss franc intact at UBS.

The Swiss franc has proven to be one of the biggest losers in the G10 currency basket during the Middle East conflict, which might seem odd for a traditional haven currency: times of stress should benefit it.

However, a new note from the UBS investment banking division says it anticipates strength to return, citing the following:

● Month-end rebalancing flows that weakened the franc are time-sensitive and expected to fade, removing a temporary headwind.

● Swiss domestic investors are structurally reducing foreign asset exposure, creating sustained home-currency demand.

● The yield incentive to hold foreign assets is too small to reverse that behaviour: the FX-hedged US Treasury/Swiss government bond differential sits at around 38bp at the 10-year tenor.

● Swiss exporters are actively selling USDCHF on rallies to around 0.80, with franc-buying rebounding from historically depressed levels.

● The franc's real effective exchange rate has retreated from its early 2015 spike back to 2025 levels, reducing the SNB's most powerful argument for intervention.

● ECB rate expectations are far more aggressive than the SNB's: around 82bp priced versus 31bp, meaning a growth-focused policy repricing hits the euro harder than the franc.

● EURCHF has historically traded uncorrelated with rate differentials, meaning the recent widening that pressured the franc is unlikely to persist.

● Swiss activity data remains resilient, with the March PMI surprising to the upside, reducing the case for SNB easing.

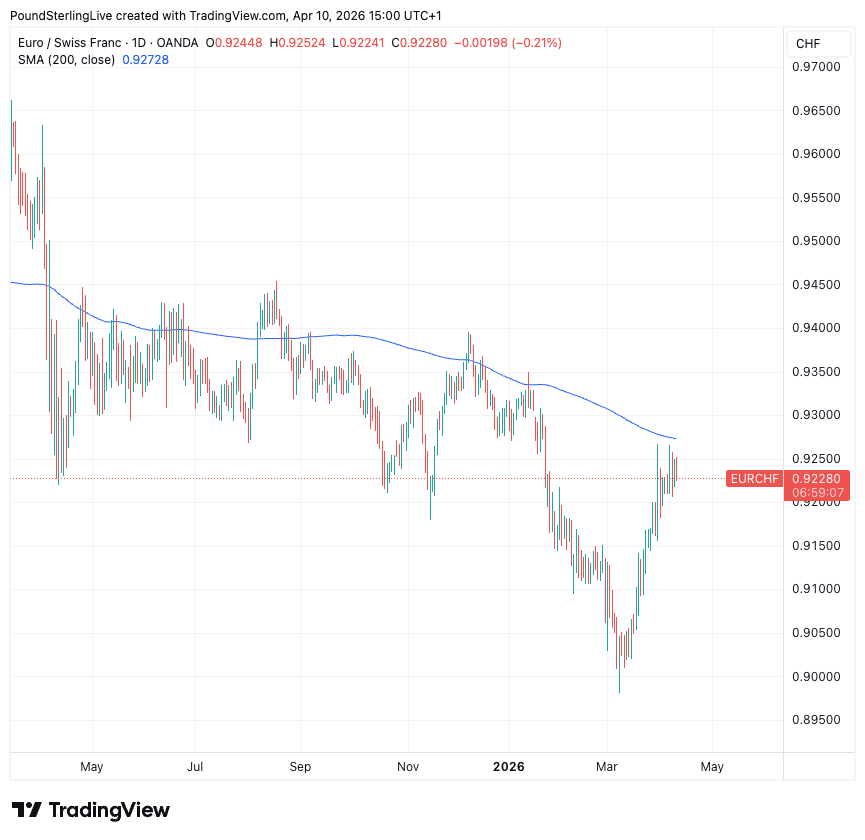

UBS sees EURCHF near its 200-day moving average as tactically attractive to the downside (see chart above), with the end-Q2 target at 0.90.