Image © Adobe Images

SNB signals franc intervention readiness, sending the Swiss currency sharply lower against peers.

The risk of intervention against a strong Swiss franc has risen sharply after the SNB used today's policy decision to signal a much greater readiness to step into the FX market if needed.

The SNB left its policy rate unchanged at 0% and made clear that the Middle East conflict has changed the balance of risks:

"Given the conflict in the Middle East, our willingness to intervene in the foreign exchange market has increased."

It added that it would act to counter "a rapid and excessive appreciation of the Swiss franc, which would jeopardise price stability in Switzerland."

This represents a shift in focus away from rates and toward the exchange rate as the main policy concern.

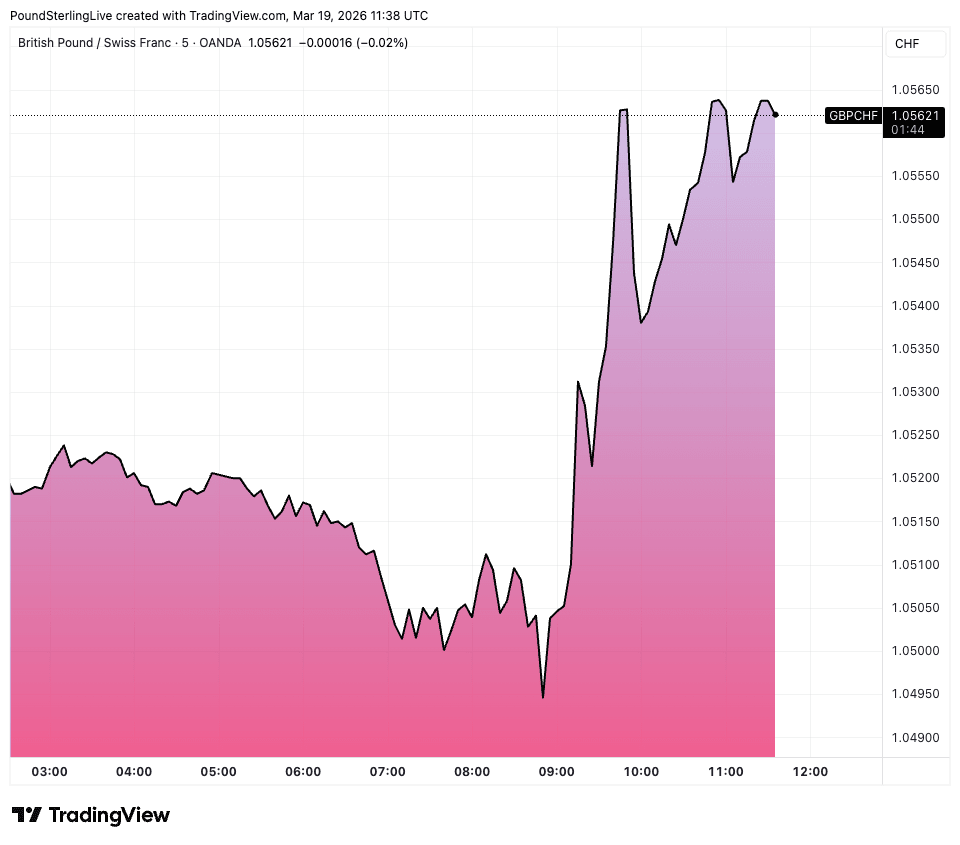

The pound-franc exchange rate rallied to 1.0562, a 0.45% daily gain that takes the pair to its highest since February 09. Euro-franc rises rises half a per cent to 0.9122 and dollar-franc to 0.7957.

"CHF is down against most major currencies after the Swiss National Bank (SNB) delivers a dovish hold," says Elias Haddad, Global Head of Markets Strategy at Brown Brothers Harriman.

The SNB's updated inflation profile contributed to the currency's weakness as average annual inflation is now seen at 0.5% in 2026, 0.5% in 2027 and 0.6% in 2028, meaning the central bank sees short-term inflation higher because of energy prices, but medium-term inflation is slightly lower because of the stronger franc.

"A rapid and excessive appreciation of the Swiss franc poses a risk to price stability. To counter this risk, our willingness to intervene in the foreign exchange market has increased," said Chairman Martin Schlegel in the press conference.

He explained the franc's rise has tightened monetary conditions, noting that "Swiss franc appreciation reduces imported inflation and dampens economic activity."

Karsten Junius, Chief Economist at J. Safra Sarasin, says currency intervention is now the preferred policy lever as the central bank showed no clear bias to cut or raise rates in coming quarters.

"We consider it absolutely appropriate for the SNB to consider FX interventions in the current situation rather than to change its policy rate," says Junius.

That assessment fits the official signal that interest rate policy is broadly in the right place, with Schlegel also stressing robust lending growth and a high hurdle for reintroducing negative rates.

The implication for markets is that the franc now faces a more explicit policy constraint which crimps upside potential and is a potential rally-ender.

Junius says, "The SNB sees FX interventions as appropriate," and adds that he would be surprised if the next published intervention data showed no activity.

That is especially relevant after Schlegel confirmed that Switzerland's memorandum of understanding with the U.S. does not prevent the SNB from intervening for monetary policy purposes, even if he declined to say whether the bank has already acted.