Above: Novartis, Basel, Swizterland. Image © Adobe Images.

For now, hopes of a trade deal are cushioning the Franc.

The Swiss Franc is at risk of "de-rating," warn analysts at Bank of New York (BNY) following the surprise announcement that Switzerland would be subject to a 39% U.S. import tariff.

Analysts at the bank warn that unless the country secures a trade deal, it could risk seeing its trade surplus wiped out, which would have significant implications for the currency.

"The U.S. remains Switzerland's largest single-country export destination and a significant drop in receipts presents a case for significant derating of the currency," says BNY.

Switzerland is reportedly ready to make a "more attractive offer" in trade talks, its government said on Monday, following a crisis meeting aimed at averting a 39% U.S. import tariff on Swiss goods that threatens to hammer its export-driven economy.

The Federal Council said it was determined to pursue discussions with the U.S., beyond the August 7 deadline that U.S. President Donald Trump has set for the tariff to come into effect.

The 39% tariff rate is among the highest the U.S. has imposed on another country and is certainly the highest among the world's developing economies.

According to BNY, Switzerland will struggle to maintain its trade surplus over the long term without its pharmaceutical exports, and the U.S. is by far the biggest market for the sector.

A trade surplus provides a fundamental source of support for a currency as it is the result of a country's earnings exceeding its outgoings. This, as well as the Franc's solid 'safe haven' features, have contributed to its outperformance over recent years.

Swiss total exports were valued at US$446.84BN in 2024, while the country's average trade surplus between 1970 and 2023 was 4.96% of GDP. In 2024, the surplus with the U.S. was reported to be around $38BN in goods, largely on account of pharma exports.

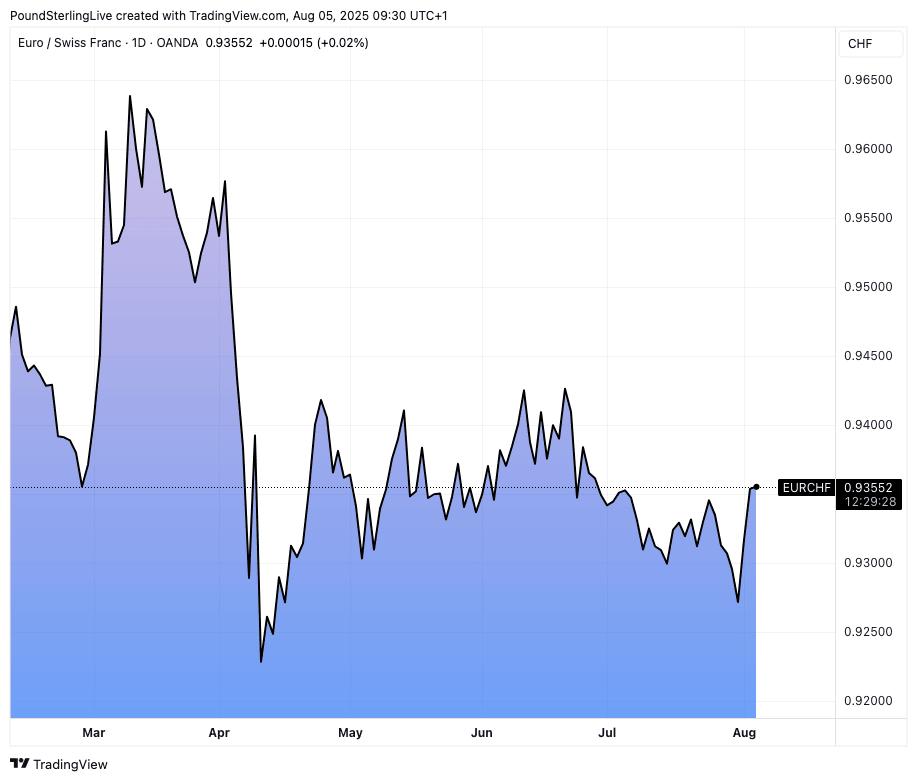

Above: EUR/CHF at daily intervals. CHF weakness has thus far been contained.

BNY warns that this surplus could be at risk if the U.S. were to implement current plans. For the Franc, the development could be significant.

Near-term, the effects would be felt via a "significant downturn in economic expectations domestically, which would strengthen the case for more assertive easing by the SNB in September," says BNY.

The SNB has cut rates to 0% and negative interest rates are now firmly back on the radar as a result.

However, some analysts think the Franc will prove resilient in the face of negative interest rates: "CHF safe haven status outweighs the drag to the currency from the likelihood of negative rates," says Elias Haddad, Senior Markets Strategist at Brown Brothers Harriman.

"In our view, the SNB still has room to lower the policy rate into negative territory. Inflation pressures remain benign and plans by the US to impose a 39% tariff (up from an initial 31% proposal) on Swiss goods from August 7 is a drag to growth," says Haddad.