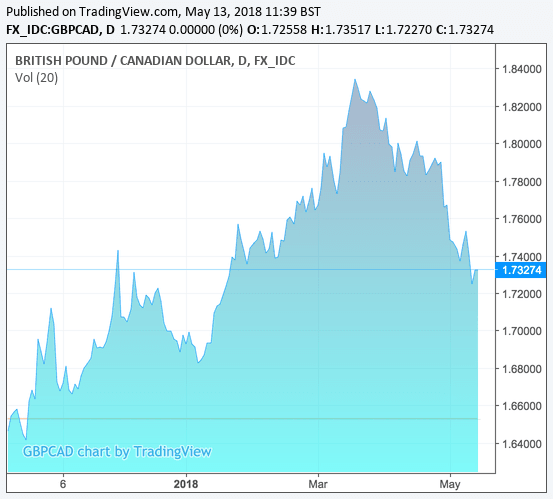

- GBP/CAD heading towards "1.71 zone at least"

- Sterling's week ahead dominated by release of wage, employment data

- Canadian Dollar eyes inflation numbers on Friday

The Pound-to-Canadian Dollar exchange rate's long-term period of recovery came to an end in mid-March, and it appears that the 2018 best for the exchange rate at 1.84 is now well out of reach.

To us, near- and medium-term momentum appears to favour the Canadian Dollar, and as such we will be looking for more of the same over coming days and perhaps, even weeks.

After eight consecutive weekly losses, Shaun Osborne, a technical strategist with Scotiabank in Toronto says, "GBPCAD weekly patterns reaffirm the soft undertone for this market. Weakness below bull trend channel and the loss of retracement support at 1.7431 suggests more downside risk towards the 1.71 zone at least, we feel."

Furthermore, Osborne notes intraday and daily trend studies are bearish while the weekly signal is flipping to negative.

"This implies limited scope for countertrend corrections, notwithstanding today’s slightly better bid tone for the market. At best, we think the bear trend is stabilising but downside risks are high and overshoot potential is not insignificant. We see resistance now at 1.7400/25," adds the analyst.

Advertisement

Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here.

CAD: What to Watch this Week

The Canadian data calendar is relatively light in the coming week so we would expect the currency to take cues from global dynamics: Watch moves in the US Dollar as the recovering Greenback has pretty much been the driving force for global financial markets over recent weeks, and the evolution of the USD should have implications for USD/CAD and the cross rates such as GBP/CAD.

Friday, May 18

The highlight on the data calendar in the week ahead is the release of inflation and retail sales at 13:30 B.S.T.

With regards to inflation, CPI is forecast to read at 0.4% on a month-on-month basis for April, up on March's 0.3%. The annualised inflation rate is forecast to read at 2.3%.

The Bank of Canada is in the midst of a gentle cycle of interest rate rises; something that tends to be supportive of the Canadian currency. However, of late markets are yet to be convinced the BoC is likely to accelerate future moves, and this has weighted on the Canadian currency.

If inflation beats expectations, it could however trigger a CAD rally as markets bet the BoC might have to bring forward additional rate rises.

"High household debt levels are an ominous threat to the Canadian economy, and NAFTA-related uncertainty continues to lurk in the background. With inflation under control and economic growth having come back down to Earth, we continue to hold the view that the Bank of Canada will hike its main policy rate just once more in 2018. A pick-up in inflation is one catalyst that could force the BoC’s hand and alter our view," say economists at Wells Fargo in a note detailing their expectations for the Canadian economy next week.

Retail sales are meanwhile likely to give some insight into how the consumer is feeling; typically strong retail sales betray robust underlying economic activity, and should the data beat market expectations we would expect CAD to catch a bid.

Markets are looking for monthly retail sales to read at 0.4% for March, unchanged on March. The core retail sales number is forecast to deliver the same. Core read at 0% in February.

GBP: What to Watch

Data is back to the forefront for Pound Sterling now that markets are trading the currency on expectations for future interest rate moves at the Bank of England. Indeed, we saw Sterling come under pressure on Thursday May 10 after the Bank chose not to raise interest rates at their May policy event, despite clear signals over preceeding months that they were likely to do so.

What we do know is that the Bank will only deliver a Sterling-supportive interest rate rise should UK data show signs of a strong recovery from a soft start to the year, and this week's data releases will therefore be key.

Tuesday May 15

Foreign exchange markets will be eyeing labour market statistics for March and April at 09:30 AM B.S.T.

The claimant count for April is forecast to have risen to 7.5K from 11.6K previously, while the unemployment rate is forecast to stay unchanged at 4.2% in March.

The three-month-on-three-month change in employment will be key, but we are yet to see market forecasts for the outcome.

Analysts at Lloyds Bank Commercial Banking are looking for a rise in employment of 150K, saying "the employment gain for the three months to March will provide a measure of the underlying strength of the economy." A rise if 150K "would be a substantive increase for the quarter, consistent with the view that the slowdown in output was most likely temporary."

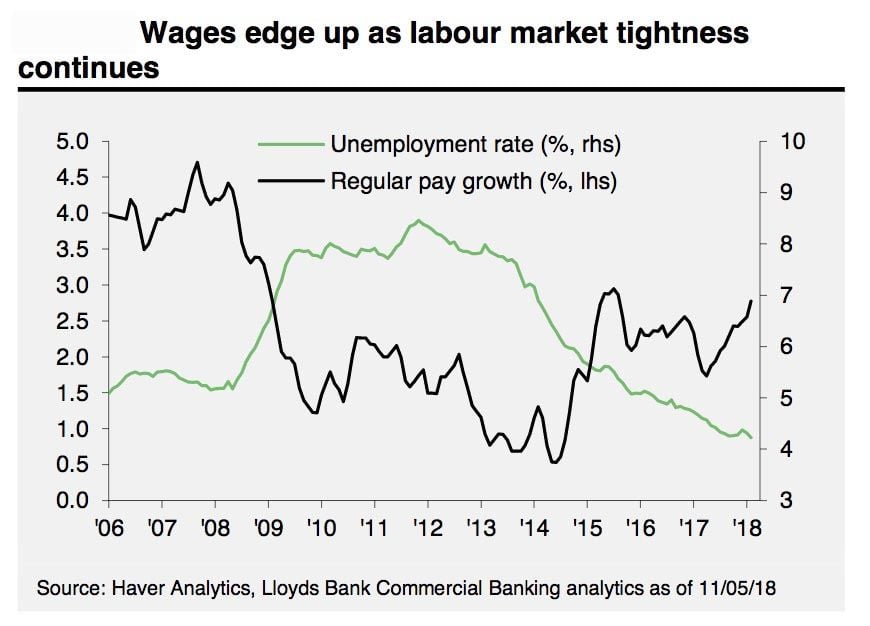

For Sterling the most important release of the day is however likely to be the wage data - the average earnings index + bonus for March is forecast to have registered growth of 2.6%, down from the previous month's 2.8%.

Should wages beat expectations we would expect Sterling to rally as it suggests there is a real risk of domestically-generated inflationary pressures rising in coming months. Such an observation would likely steer the Bank of England's hand towards delivering an interest rate rise in August.

At 10:00 AM Mark Carney and some of his lieutenants will be under the spotlight when they are questioned by the Treasury Select Committee in Westminster on their current guidance for interest rates and expectations for the UK economy.

Expect some criticism from MPs on the apparent u-turn performed by the Bank of England when they opted to not raise rates in May, despite having dropped some significant hints that such an outcome was likely over preceding months.

The Bank will no doubt point at the data. What could move markets is any strong hint on future rate prospects for the economy, so keep an eye on the newswires.

"The market now assigns a greater-than-even chance that the MPC will be on hold for the rest of the year. We are not so sure, because we look for GDP growth to rebound in coming quarters. We acknowledge the downside risks that Brexit uncertainty imparts to the economic outlook, but we still forecast that the MPC will raise rates 25 bps at the August 2 policy meeting. After that rate hike, we then look for the MPC to remain on hold through the end of the year," say analyst at global investment bank Wells Fargo in their latest assessment on the future of UK interest rates.

Advertisement

Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here.