© Stockyme, Adobe Stock

The Canadian Dollar and oil prices used to go together like the proverbial 'horse and carriage' until the linkage broke - however that link appears to be returning.

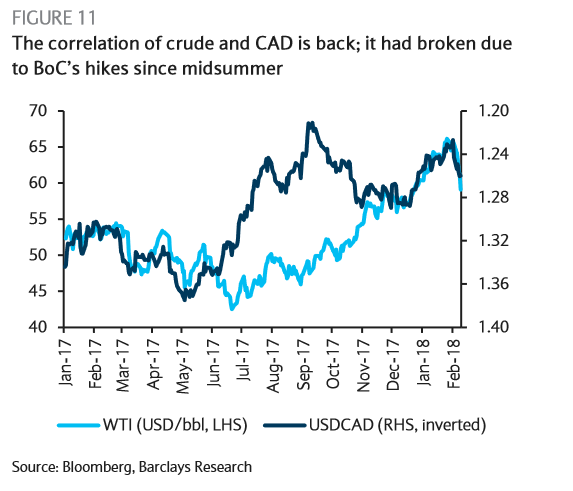

The correlation between oil prices and the Canadian Dollar is back argue analysts at Barclays bank, after the recent sell-off in oil below $60 per barrel coincided with a bout of weakness for the Canadian Dollar.

"The usually strong correlation between crude oil and the loonie has come back, after taking a break following the BoC’s hawkish shift: USD/CAD reached 1.26 for the first time since November, as WTI breached USD 60/bbl (Figure 11)," says Barclays FX analyst Dennis Tan.

The correlation used to be extremely tight, especially for the USD/CAD pair because of Canada's disproportionately large oil exports to the US.

Rises in the price of oil meant increased demand for Canadian Dollars from US importers who in turn had to sell their US Dollars to buy the oil, all in all leading to a fall in USD/CAD.

At the start of 2017, however, the correlation started to break down as the loonie increasingly took its cue from rising interest rates instead.

Increased economic growth spurred the Bank of Canada (BOC) to hike interest rates, and higher interest rates attract greater inflows of foreign capital drawn by the promise of higher returns, which in turn supports demand for the currency.

If the correlation between oil and CAD continues it may not be a very positive sign for CAD since oil prices are expected to remain stuck at a low level for a long period time due to a perpetual supply glut caused by the ever increasing number of US shale oil producers.

"Oil prices have not sustained the high levels see in January and this could put a drag on the Canadian current account," says a note from the trading desk at swiss-based UBS who recommend selling Canadian Dollars during February.

Recently the Organisation of Petroleum Exporting Countries (OPEC) revised up their forecasts for world production; increased production of oil typically has a downward effect on oil prices if there is no corresponding increase in demand:

"OPEC now believe that non‑OPEC oil supply will grow 1.4mb/d (or 1.4%) this year, up 0.32mb/d from the group’s previous forecast. The production upgrades largely reflect upward revisions to US output," says commodities analyst Vivek Dhar of Commonwealth Bank of Australia (CBA).

The oil market's only hope is that rising global growth will increase demand for oil and soak up for the extra supply, and there are signs of this happening, at least in 2018.

OPEC too have revised up their forecast for global demand, writes CBA's Dhar:

"Global demand was also revised a touch higher and now suggests growth of 1.59mb/d this year. The forecast of an incremental deficit in oil markets this year underpins OPEC’s hope that oil markets are re‑balancing."

As a consequence OPEC's strategy is to loosen supply constraints and allow the market to find its own level.

Yet it seems supply is a lot easier to forecast than demand as the Energy Information Administration (EIA) is of the opposite view to OPEC and thinks that supply will in fact outpace demand, leading to lower prices.

This also seems to be the view of CBA:

"Our concern is that supply is outpacing demand, which is consistent with the US Energy Information Administration’s (EIA) view," concludes Dhar.

Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here.