Momentum favours the Pound in the near-term but longer-term the argument for further CAD strength is made by a notable analyst we follow.

The Canadian Dollar has been on the back-foot against the Pound for 13 out of the past 15 trading sessions confirming a decent head of steam that favours Sterling in the near-term.

GBP/CAD is rising in a mini-up-trend higher, clearly visible on the 4-hour chart below.

This is expected to extend higher with a break above the 1.6400 highs leading to a continuation up to 1.6425.

The long spike lower on the day of the flash crash was probably an exhaustion bar, signaling the end of the downtrend.

Any further extension higher is likely to be capped by overhead resistance from trend-lines in the 1.64s.

In the event of a break below the 1.6315 lows and the trendline for the move up would signal more downside towards a target at 1.6100.

Scotiabank’s Shaun Osborne sees price action in GBP/CAD as “delicately poised after last week’s squeeze higher.”

He sees the move higher after the flash-crash suffered in early October as being corrective in nature rather than the start of a new uptrend.

“Trend momentum has moderated on the daily study but remains bearishly aligned with the longer-term trend oscillator signals still. We think the set up here remains GBP-negative. We still rather feel that risks are geared towards a retest of the 1.52/1.55 range in the months ahead. Look to fade GBP rallies,” says Osborne in a recent client briefing.

Latest Pound / Canadian Dollar Exchange Rates

| Live: 1.8823▼ -0.37%12 Month Best:1.9044 |

*Your Bank's Retail Rate

| 1.8183 - 1.8259 |

**Independent Specialist | 1.856 - 1.8635 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

Friday the 4th will be Key for CAD

The Canadian dollar has recovered after Bank of Canada Governor Poloz’s most recent comments in which he suggested the Bank of Canada had no plans to change interest rates in the next 18 months.

CIBC Economics, however, read the statement as inferring a data dependent stance, not a commitment to keep rates unchanged.

“We want to emphasize that the BoC will be data dependent and sensitive to external events into the medium-term,” said CIBC’s Bipan Rai.

Oil is another major driver of the loonie.

The commodity has been highly volatile of late both rising in the OPEC-Russia deal and then falling.

Inventory data in the week ahead could therefore further materially impact the currency.

Friday, November 4 will be a big day for the loonie as it includes several major releases and events.

A speech from Governor Poloz at 1.35 AM (GMT) kicks off the day’s proceedings.

In his previous speech, Poloz took a more ‘wait and see’ neutral tone after rattling markets a month ago by suggesting an interest rate cut might be on the way.

Clearly, if there is another hint of more rate cuts in the pipeline that will weaken CAD.

Later at 13.30 (GMT) the BoC will release Employment data, which includes Employment Change, and the Unemployment rate (currently at 7.0% )

Also out at 13.30 (LT) is the Canadian Trade Balance for September and Ivey PMI for October.

The Pound: PMIs, Bank of England and High Court Challenge to Article 50

The key fundamental for the Pound is whether the Bank Of England (BOE) cuts interest rates any lower at its meeting on Thursday.

Markets appear to be attributing a roughly 50/50 chance to the possibility.

What will also be of interest are the changes made to growth and inflation forecasts in the Bank's Quarterly Inflation Report.

The Bank's forecasts could well hint at future policy decisions, particularly if they believe inflation will rise faster than previously anticipated.

The Bank will not tolerate inflation much higher than 2% and is expected to raise interest rates should this level be threatened.

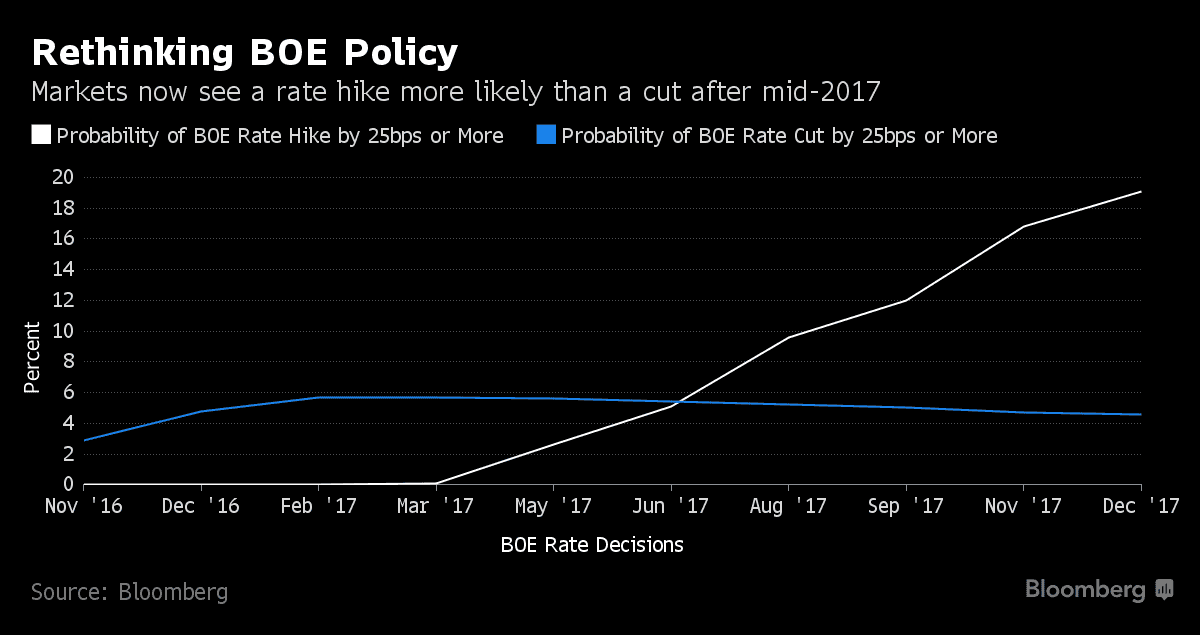

It is because of rising inflation expectations that markets are starting to price in higher interest rates in the future:

Overnight index swaps indicate that there is now more of a chance of an interest rate rise than a rate cut in 2017.

Rising interest rates are deemed to be supportive of a currency in that they attract capital inflows as global investors seek out yield. Clarity on Brexit, combined with rising interest rates, will be the ultimate catalyst for a longer-term and more sustainable Pound recovery.

Traders are re-evaluating how long monetary policy policy will remain accommodative following better-than-forecast economic growth data and BoE Governor Mark Carney’s suggestion two days ago that the prospect of faster inflation is diminishing the case for easing.

Carney also said the Bank would consider the impact of future decisions on the already weak Pound.

This suggests the BoE may hold fire for fear of weakening the Pound, which would make imports more expensive, and risk excessive inflation.

The other major theme for Sterling relates to the current high court challenge to the government’s authority to trigger Article 50 on its own without the agreement of parliament.

The failure of a similar challenge in a high court in Belfast is thought to have set a precedent which the London court is likely to follow.

If the challenge is unsuccessful the pound will fall; if not it will rally strongly.

It is not clear when the London court will make its decision but those with an interest in Sterling should keep one eye on the newswires.

The main data releases in the week ahead are the trio of October Purchasing Manager Indices (PMI) releases.

Tuesday, November 1 sees release of the final estimate for Manufacturing PMI for October at 10.30 GMT, which is expected to come out at 54.5 from a preliminary estimate of 55.4.

Construction PMI is out on Wednesday at 10.30 (GMT) and is forecast to moderate to 51.8 from 52.3.

Thursday sees the release of Services PMI at 10.30 (GMT), which is forecast to come out at 52.1 from a preliminary estimate of 52.6.