Above: File image of Governor Tiff Macklem (right). Image © Bank of Canada, Reproduced Under CC Licensing

Achieve up to 3-5% more currency for your money transfers. Beat your bank's rate by using a specialist FX provider: find out how.

The Canadian Dollar was buoyed on Wednesday when the Bank of Canada (BoC) said it expects "a sharp rebound in economic activity" this quarter but that it will still provide a monetary escort to the economy until it returns to dry land.

Canada's Dollar was in retreat from the U.S. Dollar following the July BoC announcement while winning back ground previously lost to Sterling, the Euro and others, although it soon swept away opposition from even the greenback.

This was after the BoC left its overnight rate at the new coronavirus-inspired record low of 0.25% and said it would remain there "until economic slack is absorbed so that the 2 percent inflation target is sustainably achieved."

To reinforce the message for markets, the BoC says it'll continue buying "at least $5 billion per week of Government of Canada bonds," through its quantitative easing programme, which brings the full weight of the bank to bear on the 'risk free rate' that gets baked into all interest rates charged across the economy.

"The Long and Winding Road would be the appropriate musical score for the Bank of Canada’s July’s message, underscoring that the path to a full recovery is both lengthy and uncertain," says Avery Shenfeld, chief economist at CIBC Capital Markets. "It’s base case scenario sees real GDP dropping 7.8% in 2021, with growth of 5.1% in 2021 and 3.7 in 2022."

Above: GBP/CAD and AUD/CAD shown at 15-minute intervals, falling in wake of July BoC announcement.

Above: GBP/CAD and AUD/CAD shown at 15-minute intervals, falling in wake of July BoC announcement.

The BoC said a sharp recovery began in the second quarter but that it will take at least until 2022 under its 'central scenario' for the economy to reach pre-coronavirus levels of output.

Its commitment to keep the cash rate at 0.25% until "economic slack is absorbed" could indicate that rock bottom borrowing costs will prevail for government, company and household alike until pre-virus levels of employment are achieved again. That could be a prerequisite for pre-virus levels of output.

"The bank wants Canadians to know that borrowing costs will remain low for a long time," says Josh Nye, a senior economist at RBC Capital Markets. "Governing Council is pledging to keep the overnight rate at its current level until the economy is back at full capacity and inflation is sustainably at the bank’s 2% target. Based on economic projections in the MPR, that won’t be until 2023."

The inflation target had been "sustainably achieved" when the coronavirus flew like a bat out of Wuhan in January, and unemployment was close to multi-decade lows. But statistical and economic quirks mean it does not necessarily follow that employment must recover fully for sustained 2% price growth.

Guidance on quantitative easing was different. It "will continue until the recovery is well underway," which could mean that bond buying continues until the virus is extinguished or a reduction in unemployment is sustained.

"This means short rates pinned to the floor and longer dated yields staying depressed. This suggests the BoC will play second fiddle to other short-term drivers of CAD: global sentiment, oil and US virus cases," says Francesco Pesole, a strategist at ING. "Global sentiment remains inevitably the key driver."

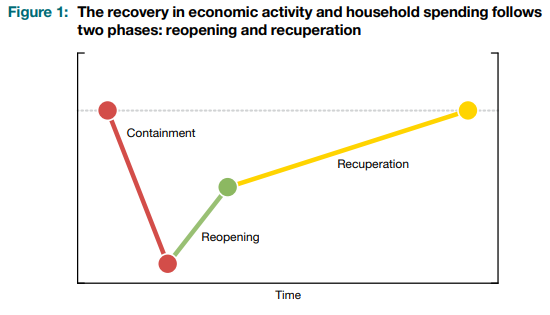

Above: Bank of Canada illustration of its central scenario for the Canadian economy.

Above: Bank of Canada illustration of its central scenario for the Canadian economy.

"In Canada, the number of new COVID-19 cases has fallen sharply from its April high, and the economic recovery has begun in all provinces and territories and across many sectors. Consequently, economic activity is picking up notably as measures to contain the virus are relaxed. This is a welcome sign. The Bank of Canada expects a sharp rebound in economic activity in the reopening phase of the recovery, followed by a more prolonged recuperation phase, which will be uneven across regions and sectors. As a result, Canada’s economic output will likely take some time to return to its pre-COVID-19 level. Many workers and businesses can expect to face an extended period of difficulty," the BoC says.

Markets hadn't expected any less than they got from the BoC, leaving only a clear eyed assessment of the challenges ahead and its commitment to escort the economy back onto dry land to explain the Loonie's relative resilience against a recovering U.S. Dollar and its pushback against other currencies.

Commitments to low interest rates and quantitative easing are not normally kind to currencies though it might matter more to investors in the unprecedented circumstances of 2020 that central bankers either help economies out of the mire they're in, or at least not get in the way of the recovery.

To the extent this is the case the BoC hit all of the right notes on Wednesday, and the Canadian Dollar appeared to fare better than many other currencies, although it has also undeperformed many in recent weeks.

USD/CAD was volatile owing to U.S. industrial production figures released around the same time, although GBP/CAD, EUR/CAD and even the previously rallying AUD/CAD were seen in retreat afterward.

Above: USD/CAD shown at daily intervals alongside Pound-to-Canadian Dollar rate (orange line).

Above: USD/CAD shown at daily intervals alongside Pound-to-Canadian Dollar rate (orange line).

"CAD has been unable to fully cash in on recent risk-on runs. One of the reasons is, in our view, the high exposure of the Canadian economy to fresh lockdown measures in the US," Pesole says. "The news that OPEC+ is set to unwind some of the cuts starting from August had already been largely priced in and is failing to significantly pressure oil prices. We remain positive on the oil prospects for the rest of the year and expect them to play a supportive role."

The greenback has fallen to a year-to-date loss on a Dollar Index basis this week, enabling Sterling and the Canadian Dollar to both rise against their U.S. rival although both have been underperformers relative to other major currencies. The Loonie has underperformed since a second wave of coronavirus infections began sweeping across the U.S., Canada's next door neighbour, while Sterling has lagged others due to economic weakness and lingering Brexit risks.

This dual underperformance has seen the Pound-to-Canadian Dollar rate trading in a stiflingly narrow range spanning the gap between 1.70 and 1.7170.

Brexit negotiations remain deadlocked although there is a chance that some form of progress is made in "accelerated" talks that run to month-end, more so given reports claiming the EU has softened some of its demands in relation to British waters and an ongoing attempt at imposing EU law and economic policy on a Brexiting Britain. The details of these compromises are not known but if they lead to movement in trade talks they could put a floor under Sterling.

A Brexit breakthrough could drive GBP/USD to 1.31 or above in a steady market for risk assets, which would lift the Pound-to-Canadian Dollar rate to 1.7685 if accompanied by the USD/CAD rate of 1.35 that's seen by Scotiabank.

"The 40-day MA (1.3611) continues to slow the USD’s advance on the daily chart and the USD’s inability to make a decisive break higher through resistance in the low 1.36s over the past week or so suggests limited upside potential for funds at this point. We look for more drift to the 1.35 area near term," says Juan Manuel Herrera, a strategist at Scotiabank. "The GBP is no stranger to the risk positive mood in markets as it tacks on a 0.6% gain for the day that has pushed it above 1.26 from as low as the high 1.24s through yesterday’s North American session. Aside from reports that of promising Oxford vaccine developments, there was no market-driving news from a domestic perspective."

Above: Pound-to-Canadian Dollar rate shown at weekly intervals alongside USD/CAD (orange line).

Above: Pound-to-Canadian Dollar rate shown at weekly intervals alongside USD/CAD (orange line).