Image © Bank of Canada

- CAD stops USD and GBP in tracks after retail sale blowout.

- Sales ex-autos up strongly in June, keeping BoC cuts at bay.

- But Fed's Powell and USD are a two-way risk into weekend.

- USD and GBP tipped to head lower by TD and Scotiabank.

The Canadian Dollar stopped an advancing U.S. greenback and Pound Sterling in their tracks Friday after retail sales data for the month of June surprised strongly on the upside, although a speech by Federal Reserve (Fed) Chairman Jerome Powell is threatening to rain on the Loonie's parade.

Canadian retail sales were unchanged in June when markets were looking for them to fall by 0.3%, which was already an upside surprise for the market. But sales growth was even stronger when numbers for the car industry are excluded from the data, Statistics Canada figures showed on Friday.

Core retail sales were up by a blowout 0.9% in June when markets had looked for them to fall by 0.1%, which rounds off a strong second quarter for the Canadian economy and tees up for a decent start to the third quarter.

Sales were down in four of 11 subsectors in June, accounting for 48% of total sales Statistics Canada says, although most retailers saw trade grow. Sales were up in most sectors though and by an even stronger clip when measured in 'volume' terms, which is what counts for GDP, rather than by monetary value.

"This marks 3 out of 4 better than expected Canadian economic headlines for this week, and saw USDCAD spike lower," says Eric Bregar at Exchange Bank of Canada. "The market is now competing against “risk-off” flows that kicked in a half hour ago when China announced it will levy retaliatory tariffs of another $75bln on US goods, starting September 1st. This could make Jerome Powell’s speech at Jackson Hole at 10amET a whole lot more interesting."

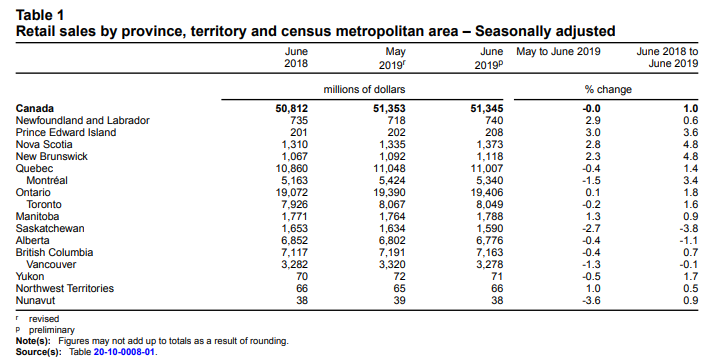

Above: Statistics Canada table detailing retail sales growth in the Canadian provinces.

"That represents a solid contribution to June GDP, which appears to be tracking 0.3% gain, leaving Q2 as a whole running above 3%," says Avery Shenfeld, chief economist at CIBC Capital Markets. "While Q2's nice quarter is mostly a rebound from two quarters of near-zero economic growth, the decent finish to the quarter gives some momentum for Q3, a reason why we see the Bank of Canada delaying a rate cut for several more months."

Markets care about the data because it reflects rising and falling demand within an economy, which is an important determinant of the inflation pressures that dictate interest rate policies. Changes in rates exert a push and pull influence over capital flows and short-term speculators. Capital flows tend to move in the direction of the most advantageous or improving returns, with lower rates normally seeing investors driven out of and deterred away from a currency while rising rates have the opposite effect.

"Global uncertainty and trade disputes have created legitimate concerns for the industrial sector and look to weigh on overall economic growth. But they have also contributed to a sharp decline in borrowing costs. Coupled with still solid-looking labour markets, signs of rising wage growth, and still-strong consumer sentiment, that suggests retail sales could look a little better over the second half of the year," says Rannella Billy-Ochieng’ at RBC Capital Markets.

Jerome Powell will deliver a speech titled "Challenges for Monetary Policy" at the Jackson Hole Symposium conference on central banking at 15:00 London time Friday, and markets are tipped to throw a tantrum if the Fed chief doesn't indulge them and the White House by signalling that a shift in stance on interest rates is afoot. Fed rate policy has the potential to upset currency markets during the months ahead, including the Canadian Dollar.

Above: USD/CAD rate shown at five-minute intervals alongside GBP/CAD rate (black line, left axis).

"Price action fatigue looks to be setting in USDCAD around the 200-day moving-average ~1.33). Given our expectations for Jackson Hole to disappoint, USDCAD's beta to rate spreads could be rekindled and help close the valuation gap relative to our HFFV estimate (~1.3150). We see this as a re-calibration to front-end rates rather than an inflection point for spot," says Mazen Issa, a currency strategist at TD Securities.

The USD/CAD rate reversed much of an earlier intraday gain following the data to trade only 0.15% higher at 1.3316 for the session, while the Pound-to-Canadian-Dollar rate was left only 0.12% higher at 1.6307. Both exchange rates are still down for the year though, by 2.08% and 6.61% respectively.

"We rather view recent price developments as a consolidation, ahead of a renewed push lower (below 1.60), than a reversal. Sustained gains through 1.6230 would give the GBP a little more stability in the short run but the cross has a long way to go before we can relax about downside risks," says Eric Theoret, a technical analyst at Scotiabank.

Above: USD/CAD rate shown at daily intervals alongside GBP/CAD rate (black line, left axis).

Investors have anticipated during recent weeks, that a mounting number of Fed rate cuts will be delivered later this year in order to insure the economy against a possible downturn related to the trade war as well as slowing global growth. Pricing in the overnight-index-swap market implies the midpoint of the 25 basis-point-wide Fed Funds range would sit at 1.52% on December 11, the date of the Fed's final meeting for 2019, when it currently sits at 2.12%.

"There’s a reason for the market’s intense focus on the Jackson Hole proceedings; while the outlook for Fed remains somewhat cloudy, this particular meeting has accumulated a reputation over the years for foreshadowing significant policy developments," says Shaun Osborne, chief FX strategist at Scotiabank. "Yellen tried to make the gathering less of a focal point for markets but the draw of Powell’s speech today is completely understandable given the apparent reluctance with which policy makers agreed to ease in July and the hammering the Fed is taking from the White House at the moment."

The U.S. Dollar was higher all G10 currencies other than the Yen Friday because investors are buying the higher-yielding greenback in anticipation that markets will be forced to rethink the collective view of just how many rate cuts the Fed is likely to deliver this year.

When the Fed cut rates from 2.5% to 2.25% on July 31, Powell characterised it as a "mid-cycle adjustment", not the beginning of an 'easing cycle'. Markets are looking for that to change Friday and if it doesn't, the U.S. Dollar could strengthen even further, sending the USD/CAD rate higher.

Fears on the FOMC have always been that a nascent global downturn will eventually hurt the U.S. through reduced demand for products made in America, although the Fed is constrained in the extent it can act by the elevated level of U.S. inflation and its statutory mandate to use interest rate policy to keep price pressures contained. However, since the July rate cut the context has changed notably, with the U.S.-China trade war flaring again and U.S. bond markets beginning to warn of recession.

"The CAD looks directionally challenged; while the short-term uptrend persists, the market has not made any headway above noted resistance at 1.3345/55. Equally, however, support at 1.3250 has held two tests this week so far and key support at 1.3195 looks distant," says Scotiabank's Theoret.

Time to move your money? Get 3-5% more currency than your bank would offer by using the services of foreign exchange specialists at RationalFX. A specialist broker can deliver you an exchange rate closer to the real market rate, thereby saving you substantial quantities of currency. Find out more here.

* Advertisement