- GBP/AUD benefiting from USD’s Fed-driven uplift

- May attempt recovery of 1.86 if USD rises further

- Could struggle after on cocktail of December risks

- Risks include BoE decision & continental virus tide

Image © Adobe Images

The Pound to Australian Dollar rate has reversed almost half of its August-to-November decline this month and may attempt to reclaim the 1.86 handle as December gets underway, although a looming cocktail of risks could mean that GBP/AUD ultimately struggles to sustain its rebound.

Sterling got off to a rocky start in November after a Bank of England (BoE) decision to leave Bank Rate at 0.10% caught an inattentive and mistaken market off guard, prompting steep losses for the Pound-Australian Dollar rate and other Sterling pairs at the time.

But an almost unrelenting advance by U.S. exchange rates throughout November has helped to steady Sterling’s ship and prompted the Pound-Australian Dollar rate to rise more than three percent over subsequent weeks.

Australia’s Dollar is often more susceptible to strength in the U.S. Dollar and this November instance has been no exception after losses for AUD/USD outstripped those seen in GBP/USD and a range of other similar pairs including NZD/USD and EUR/USD.

“USD is powering forward to new highs,” says Elias Haddad, a senior FX strategist at Commonwealth Bank of Australia. “AUD/USD fell briefly to fresh lows near 0.7200 overnight. The increased likelihood of a hawkish FOMC policy shift can drag AUD/USD down to its August lows near 0.7100.“

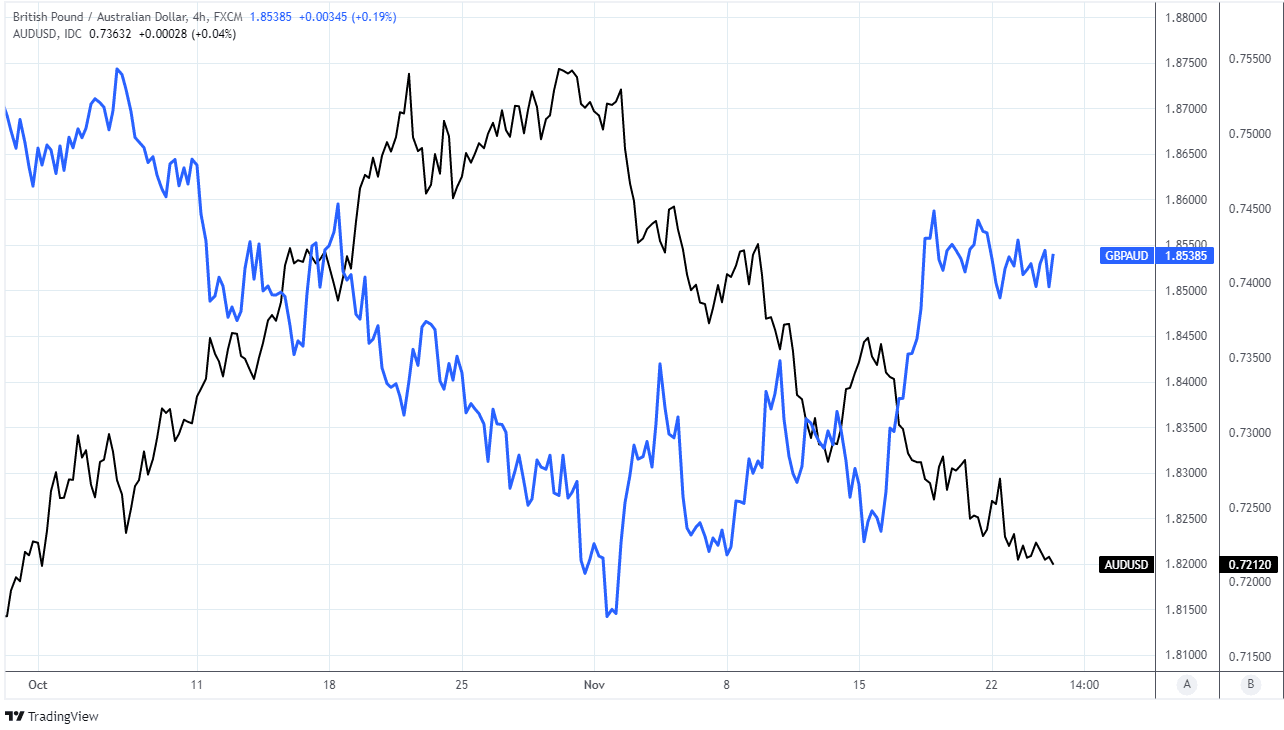

Above: Pound-to-Australian Dollar rate shown alongside AUD/USD at 4-hour intervals.

- Reference rates at publication:

GBP to AUD spot: 1.8530 - High street bank rates (indicative): 1.7880 - 1.8010

- Payment specialist rates (indicative: 1.8363 - 1.8437

- Find out about specialist rates, here

- Or, set up an exchange rate alert, here

The U.S. Dollar has advanced against developed and emerging market currencies alike since June, placing AUD/USD and GBP/USD under pressure in the process although the greenback was boosted this week by a White House decision on the leadership of the Federal Reserve.

Monday’s nomination from the White House was for incumbent Fed Chairman Jerome Powell to serve another four-year term from February 2022 with his chief rival Fed Board Governor Lael Brainard elevated to the position of Vice Chair.

“The market moved to price-in a modestly faster pace of monetary tightening with lower inflation,” said Mark Haefele, chief investment officer at UBS Global Wealth Management, in remarks to clients following the decision.

There were concerns in the market that a change of leadership at the Fed would lead to a slower pace of monetary policy normalisation and a later start to an anticipated cycle of interest rate rises that many expect will begin in the second half of next year.

The nomination came with the Dollar having been further boosted last week by statements from three other Fed Board governors who told audiences they would be likely to support an even faster winding down of the bank’s quantitative easing programme and earlier lift-off for interest rates.

“The removal of uncertainty over the Fed leadership has encouraged the US rate market to intensify its focus on the building likelihood of the Fed adopting a faster pace of tightening,” says Lee Hardman, a currency analyst at MUFG.

“We expect US yields and the US dollar to remain under upward pressure in the nearterm while US activity and inflation data is surprising to the upside,” Hardman said in a note to clients on Tuesday.

{wbamp-hide start} {wbamp-hide end}{wbamp-show start}{wbamp-show end}

The main measure of U.S. inflation climbed to more than 6% in October and still topped four percent even if changes in volatile food and energy costs are to be overlooked, with manufactured goods prices also contributing significantly to the uplift.

Speculation about a possibly hastier reversal by the Fed of the large package of monetary easing measures announced at the onset of the crisis has been supportive of the Pound-to-Australian Dollar and could yet lift it further over the coming weeks.

However, Reserve Bank of Australia (RBA) and Bank of England interest rate policies have also been key influences too and Sterling will face risks in this context during December, which could serve to limit or perhaps even reverse some of the Pound-to-Australian Dollar rate’s gains.

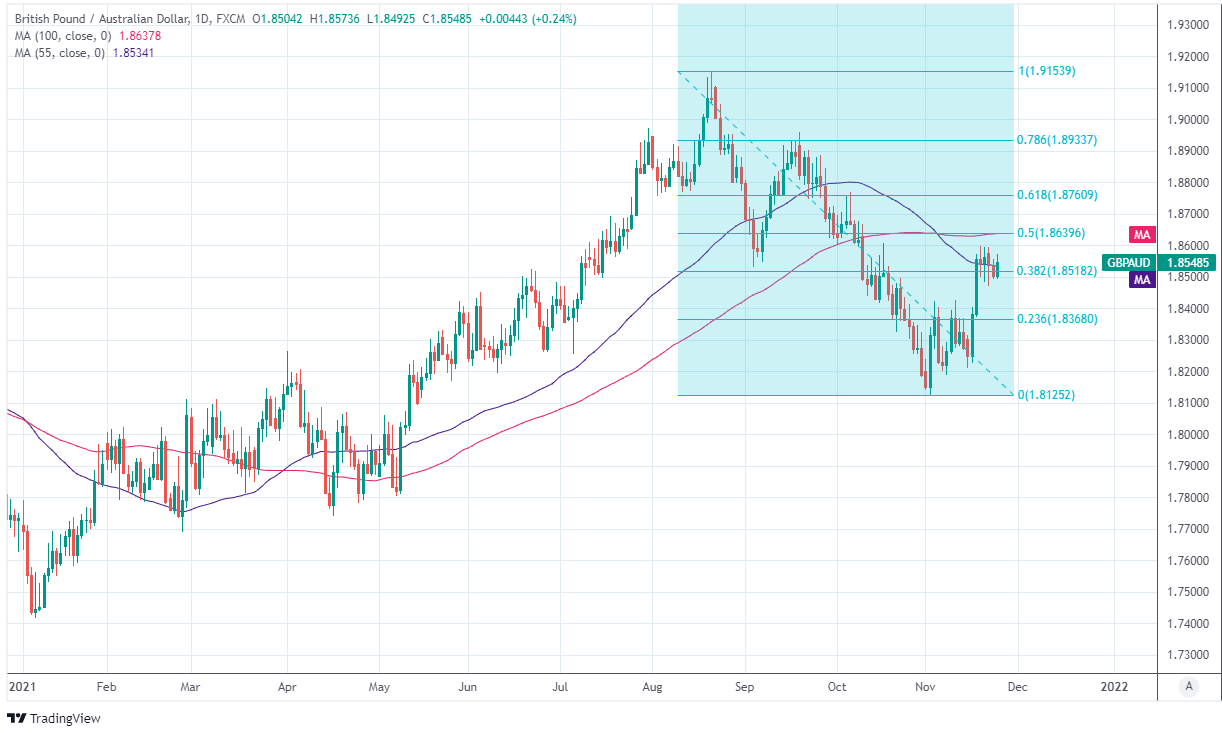

Above: GBP/AUD shown at daily intervals with major moving-averages and Fibonacci retracements of August decline indicating likely areas of technical resistance.

“The Aussie made steep gains against sterling in October, but with both the RBA and Bank of England starting November with more dovish than expected decisions, GBP/AUD may be in for a period of consolidation,” says Sean Callow, a senior FX strategist at Westpac, in a recent note to clients.

“We see near term risks of a test of GBP/AUD 1.85/1.86 but our year-end baseline is 1.85, then below 1.8200 in Q1 2022,” Callow also said.

Pricing in the overnight-indexed-swap market indicated on Wednesday that investors see around a 50/50 chance of the BoE lifting Bank Rate from 0.10% to 0.25% on December 16, reflecting the close-run and finely balanced nature of the call.

Such a balance of expectations means that any decision to actually lift Bank Rate in December could have an uplifting influence on Sterling and vice versa, although the December 16 announcement is also set to come against a backdrop of renewed ‘lockdown’ and other restrictions in Europe.

This continental context is a headwind for the UK economy that the BoE would be cognisant of, although even in the absence of a December rate rise from the BoE it’s possible that any downside seen by the Pound-Australian Dollar rate would be limited due to the RBA’s monetary policy stance.

“The RBA delivered a sharp blow to the Aussie at its 2 Nov meeting. While dropping the 0.1% Apr 2024 bond target, Governor Lowe made clear that the RBA’s base case was no rate hike until 2024, with 2023 possible but 2022 very unlikely. Meanwhile QE will continue until at least Feb 2022,” Westpac’s Callow says.

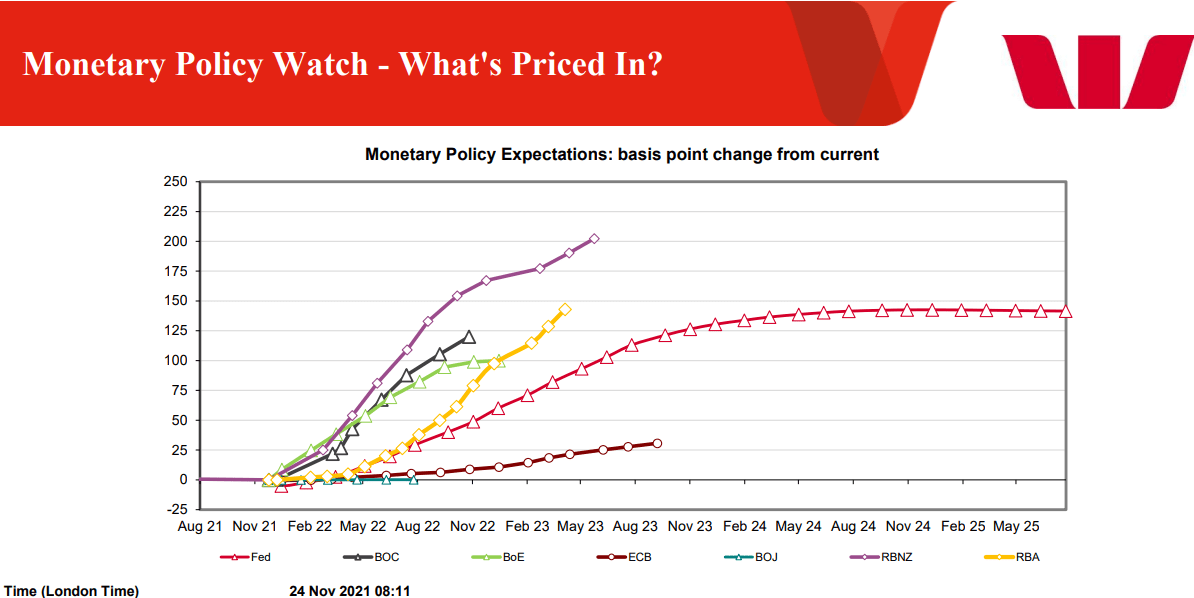

Above: Market expectations for changes in selected central bank interest rates.