- AUD underperforms in wake of RBA update

- RBA says confident of Q4 economic recovery

- Comes on day record trade surplus announced

Above: File image of Governor Philip Lowe (left). Photo Source: RBA on Flickr, reproduced with permission from the RBA press office.

- GBP/AUD reference rates at publication:

- Spot: 1.8738

- Bank transfer rates (indicative guide): 1.8082-1.8213

- Money transfer specialist rates (indicative): 1.8570-1.8644

- More information on securing specialist rates, here

- Set up an exchange rate alert, here

The Australian Dollar was the G10 laggard in the hours following then Reserve Bank of Australia's October policy review which served up a reminder that interest rates were likely to be stuck at record-low levels for months to come.

While there was nothing substantively new from the RBA's statement, the 'lower for longer' signal on rates remains a drag on Australian Dollar valuations, although some insurance against a more substantive slide will be provided by the country's impressive trade dynamics.

Indeed, while the Aussie Dollar was seen softer in the wake of the RBA update the ABS said the country enjoyed a record high trade surplus in August as exports of coal and natural gas surged.

The developments illustrate the opposite forces impacting the Aussie Dollar: a downward drag comes from RBA policy and the domestic Covid situation, while upside is offered by strong trade dynamics.

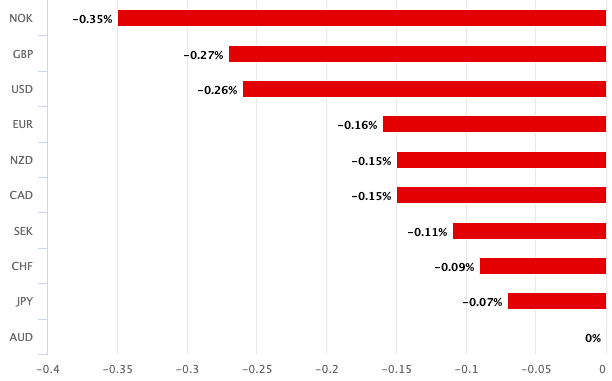

Above: The Aussie lagged all its peers on Oct. 05.

The RBA said it will continue to purchase government bonds at a rate of $4BN per week as widely expected having said last month it will next review the appropriateness of its quantitative easing purchases again in February.

The RBA says its central scenario for the economy is that conditions for higher interest rates will not be met before 2024.

But there was nothing in the Statement to cause economists at Westpac to change their expectation that an increase in the overnight cash rate of 0.15% can be expected by the March quarter 2023.

Money market pricing meanwhile shows investors are seeing interest rate rises at the RBA starting in 2023.

This puts the AUD at a disadvantage against those currencies belonging to central banks that are likely to raise interest rates imminently, namely NZD, NOK, GBP.

The Pound-to-Australian Dollar exchange rate rose a third of a percent to quote at 1.8720 in the wake of the RBA statement, the Australian Dollar-U.S. Dollar exchange rate fell a quarter of a percent to trade at 0.7270.

The RBA said the country's economy had been "interrupted" by the Covid crisis, however the setback "is expected to be only temporary".

It added the economy will return to positive growth in the fourth quarter as major restrictions in New South Wales and Victoria are expected to be lifted owing to key vaccination thresholds being reached.

Pre-delta outbreak growth rates would be attained in the second half of 2022, which signals rate rises can be considered from this point onwards.

Lee Hardman, Currency Analyst at MUFG says the Australian Dollar remains an underperformer: "it has been the worst performing G10 currency over the past month alongside the New Zealand dollar."

Investor concerns over slowing global growth, "especially in China continues to weigh heavily on the Australian dollar," he says.

{wbamp-hide start} {wbamp-hide end}{wbamp-show start}{wbamp-show end}

But positioning for further Australian Dollar downside is now reaching extreme levels as MUFG analysis shows the two-year z-score for short AUD positions is currently at around 2.5 standard deviations above the mean over that period.

"Such extreme positioning increases the risk of a short squeeze," says Halpenny.

A short squeeze is where a currency rises sharply as bets against it are closed out, forcing participants to buy that same currency.

Typically positioning is mean reverting, suggesting the extremes currently seen won't be sustained indefinitely.

Francesco Pesole, FX Strategist at ING Bank N.V. says the policy divergence between Australia and New Zealand may struggle to push AUD/NZD significantly lower in the near term considering that:

a) AUD, unlike NZD, can benefit from the energy crunch narrative

b) positioning on AUD/NZD is heavily skewed to net-short territory.

The RBA decision came on the same day the ABS reported Australia recorded its third successive record trade surplus in August, which is seen as offering a fundamental source of support for the Australian Dollar.

The trade surplus jumped by A$2.4BN to A$15.1BN in August, beating expectations for a reading of A$10BN.

"Looking through the month-to-month volatility, the key dynamic is that higher commodity prices have significantly boosted export earnings, driving the trade surplus to new record highs," says Andrew Hanlan, Senior Economist at Westpac.

Strong trade dynamics are supportive to Australian Dollar valuation and we wrote at the start of the week they offer insurance against major declines that might come from Reserve Bank of Australia policy and/or the domestic Covid situation.

Westpac's foreign exchange modelling now finds that the Australian Dollar's 'fair value' level is now at a seven year high "on the huge commodity price rise".

This yawning undervaluation gap will offer the currency support in the event of further U.S. Dollar strength, market stresses and an environment of 'lower for longer' interest rates at the RBA.