Image © Greg Brave, Adobe Stock

- GBP/AUD to go sideways with bearish tilt

- Longer-term charts look very bearish

- Pound to be impacted by leadership race

- Aussie by employment and Chinese data

The Pound is looking broadly negatively aligned against the Australian Dollar, but there appears to be the prospect for sideways movement in GBP/AUD over the coming week.

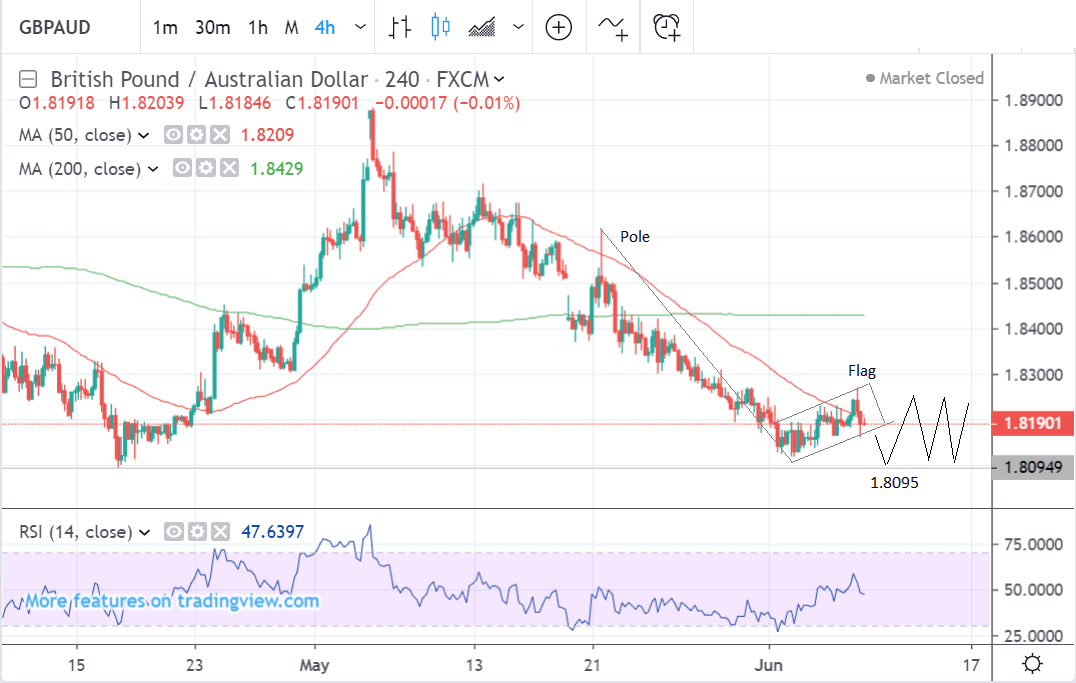

The Pound-to-Australian Dollar rate is trading at around 1.8190 at the start of the new week, after falling a tenth of a percentage point in the previous week. Studies of the charts suggest that the exchange rate will probably soon find a hard floor and the go sideways over the next 5 days.

The 4-hour chart shows the pair in a strong downtrend more or less since the beginning of May. Over the last few days, however, the downtrend appears to have pulled back and formed a type of consolidation rectangle.

The steep move down followed by the consolidation looks like a bearish continuation pattern called a ‘bear flag’. Normally this would herald much lower prices to come - as low as the length of the pole extrapolated down again - and whilst there is a risk of this happening, tough support from the April lows at 1.8090 - and a cluster composed of the daily and weekly moving averages - is likely to place a hard floor under prices, limiting further declines in the short-term.

Instead, we expect the pair to go sideways between 1.8200 and 1.81 roughly, once it has touched the 1.8090 level.

We use the 4-hour chart to determine the short-term outlook, which includes the coming week.

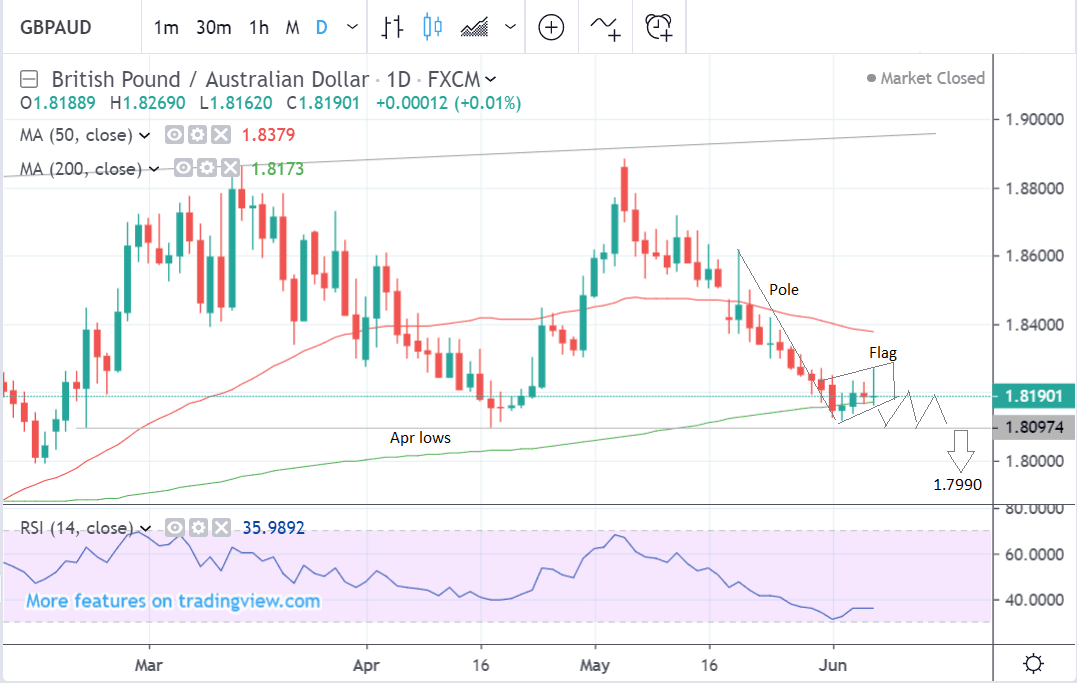

The daily chart is more bearish and given the downtrend is dominant we expect that in the medium-term the pair will finally break below the April lows and extend down to the next downside target at 1.7990. This is likely to transpire over the next 1-4 weeks.

We use the daily chart to give us an indication of the medium-term outlook which includes the next week to a month ahead.

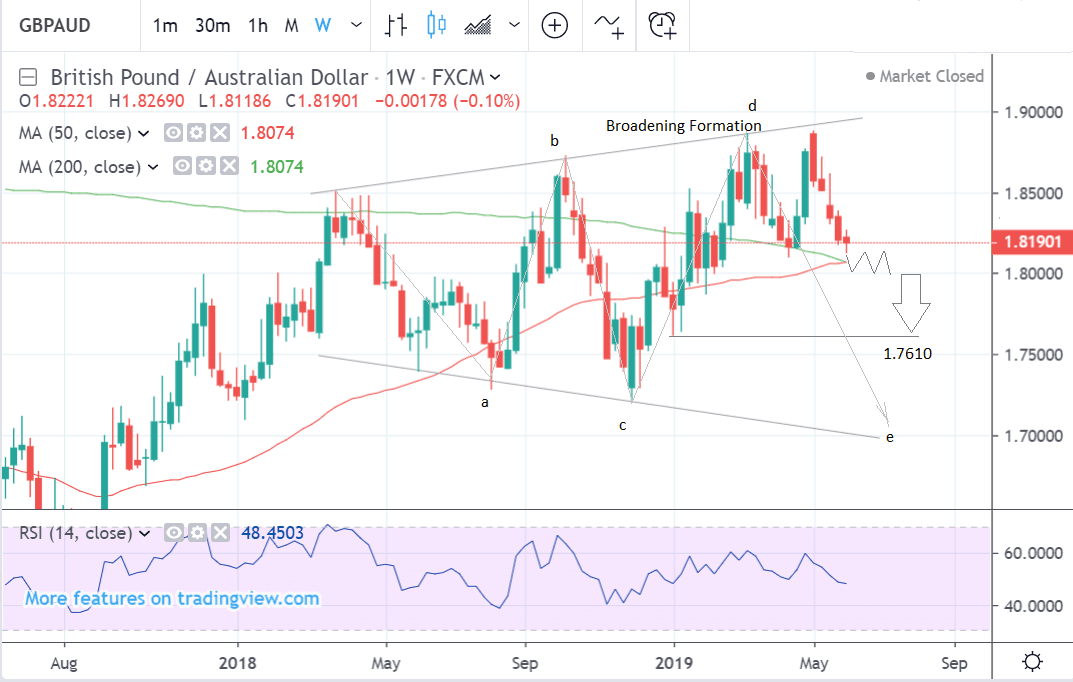

The weekly chart shows the long-term picture which is bearish owing to the formation of a broadening formation price pattern.

These are composed of steadily widening waves of buying and selling which open out into a loudspeaker-like price pattern. They are normally composed of 5 waves, labelled A-E and this one is probably in the process of forming wave E down.

Overall, the bearish long-term target lies at 1.7610 at the January lows.

We use the weekly chart to give us an idea of the longer-term outlook, which includes the next few months.

Time to move your money? Get 3-5% more currency than your bank would offer by using the services of foreign exchange specialists at RationalFX. A specialist broker can deliver you an exchange rate closer to the real market rate, thereby saving you substantial quantities of currency. Find out more here.

* Advertisement

The Australian Dollar: Scrutinising Chinese Data

Australian employment and Chinese industrial production data are the key releases for the Australian Dollar in the week ahead.

Australian employment data is expected to show a welcome drop in the unemployment rate to 5.1% (from 5.2% previously) when released on Thursday, June 13 at 2.30 BST.

Although this could provide the currency with some short-term relief, especially if the decline is greater than expected, it is unlikely to change the longer-term negative outlook, and the fact most analysts expect the Reserve Bank of Australia to support the economy with two more interest rate cuts before the end of the year.

“We have seen in recent months the unemployment rate ticking higher. That was one of the factors that led to the RBA cutting interest rates. So if we do see a somewhat more positive jobs report next week that could be slightly positive for the Australian Dollar but it is unlikely to significantly alter expectations that the RBA will be forced to cut rates possibly as much as twice later this year,” says Raffi Boyadijian, economist at broker XM.com.

Fears that the trade war between China and the U.S. could cause a slowdown in the Chinese economy are front of mind at the moment so analysts are closely scrutinising Chinese data for evidence of such a decline, and if they find it, it is likely to have a negative knock-on effect on the Aussie.

This is because China is Australia’s largest trading partner so the state of the Chinese economy can have a big impact on the Australian currency. If the Chinese economy weakens it can dampen demand for Australian exports such as iron ore, coal, and aluminium, reducing demand for the Aussie in the process.

The Chinese trade balance is probably the most significant release as it will show the impact of the U.S - China trade war.

It is forecast to rise to a surplus of $20.50bn in May, from 13.8 previously, when it is released on Monday, June 10 at 03.00 BST.

A higher-than-expected surplus could be a positive sign, both from the viewpoint of showing China’s resilience in spite of the trade war and because higher net exports raise GDP.

Chinese new loans data is also quite important because it reflects the ‘credit impulse’. This is also a contributing factor of growth as most businesses rely on credit to expand. It is expected to show a rise to $1.225tr in May.

Assuming actual data meets expectations it should support the Aussie. If it falls well below expectations it could raise concerns about the availability of credit to spur new business formation and growth.

Chinese inflation is forecast to show a rise of 2.7% in May compared to a year ago and 0.1% from the previous month, when released at 02.30 on Wednesday, June 12.

A higher-than-expected reading should be taken as positive/bullish for the AUD, while a lower-than-expected reading should be taken as negative/bearish for the AUD.

Higher inflation when accompanied by economic growth is normally a positive sign.

Industrial production data and fixed asset investment are also both scheduled in the coming week at 03.00 on Friday, June 14.

These are also both linked to growth and could impact the outlook for China and therefore its trading neighbours.

Commentary from RBA officials Kent and Ellis, out on Tuesday and Wednesday, are unlikely to impact as the RBA had its meeting last week and their stance is unlikely to have shifted so soon after - although there is a tail risk one of them might say something to upset markets.

The current RBA stance is neutral-to-dovish. Part of the reason the Aussie rose after last week’s interest rate cut was because the market had been expecting the RBA to be more pessimistic and explicitly state it was considering further rate cuts, however, it held back from that.

Clearly any hint of more rate cuts from assistant governors Kent and Ellis next week is likely to see that stance questioned and AUD decline further.

The Pound: Politics and Labour Market Data

Brexit politics are still likely to have the greatest impact on Sterling, with UK monthly GDP, unemployment and trade balance as the main hard data releases.

The next step in the conservative leadership contest will unfold on Monday, June 10, when candidates must declare at least eight nominations from fellow Conservative MPs in order to stay in the race. This will probably result in many of the weaker candidates being knocked out.

After that all candidates will need the votes of 17 Conservative MPs to stay in the first round ballot and at least 33 – or 10% of Tory MPs – to stay in the second round of voting.

At the moment, the leading contenders are Johnson, Gove, and Hunt, but if that changes - which is unlikely - and one of the big names gets knocked out it could impact on Sterling.

Johnson appears to be in favour of endorsing a ‘leave at all costs’ Brexit on October 31.

Michael Gove has a softer stance, aiming for a Canada-style free trade agreement and a possible further delay if necessary, which has infuriated the right of the party.

Jeremy Hunt has suggested he might be against leaving without a deal, although would so “with a heavy heart”.

The main data release is April GDP which is forecast to show a -0.1% fall compared to the previous month and a 1.7% rise compared to a year ago, when it is released at 9.30 BST on Monday, June 10. Any unexpected fall in GDP will probably weaken the Pound.

Unemployment data is expected to show the unemployment rate remain at 3.8% in April, when it is released at 9.30, on Tuesday, June 11.

Also important is average earnings which are forecast to rise by 3.1% (excluding bonus) and 3.0% (including bonus). If earnings are lower-than-expected, it will probably lead to a sell-off in Sterling.

The trade balance is expected to show a narrower -£12.96 deficit when it is released on Monday at 9.30. Generally, this is considered a positive background factor for the Pound.

Industrial and manufacturing production are expected to show a -0.7% and -1.0% decline in April when data is released on Monday, also at 9.30.

Since these are indicative of GDP growth they can also have an impact on the Pound, weakening it if they undershoot expectations and vice versa if they overshoot.

* Advertisement