Above: Prime Minister Scott Morrison retained his position after an unexpected victory in Australia's national vote. File image © Pound Sterling Live, Still Courtesy of ABC

- Australian Dollar jumps on election result

- GBP/AUD remains pressured to the downside

- 1.8430 could be the key confirmation level for bears

- Pound to be driven by growing 'no deal' Brexit odds

The Australian Dollar jumped at the start of the new week, following the national election that unexpectedly returned the Liberal‑National government.

"After consistent polling in favour of the opposition Labor Party winning the Federal election, Australia has voted for no change. With the uncertainty from the election now out of the way, there could be a boost to confidence," says Besa Deda, Senior Economist with St. George Bank in Sydney.

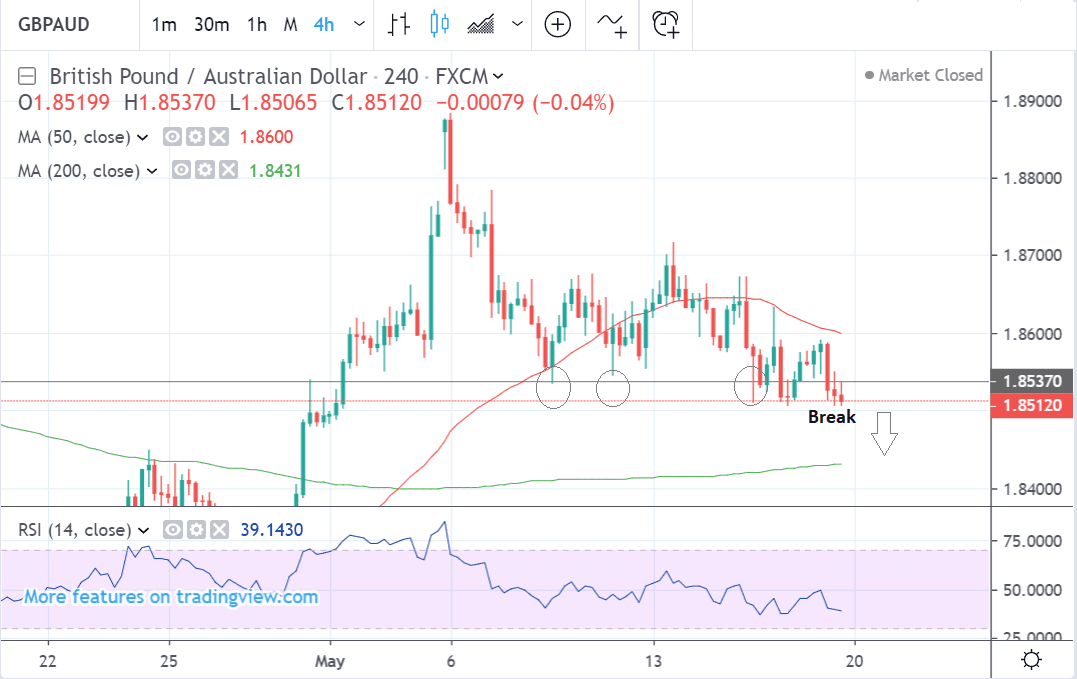

The Pound-to-Australian Dollar is trading at 1.8402, having closed the previous week at 1.8521.

Last week's 0.3% decline was largely down to Sterling weakness after cross-party Brexit talks broke down and the countdown began on Prime Minister Theresa May’s premiership. Expectations are high she will this summer be replaced by a leader who will be more 'hawkish' on Brexit and deliver a 'Brexit at all costs' on October 31.

From a technical perspective, the Pound-to-Australian Dollar outlook suggests further losses are likely.

The pair has now successfully broken below the 1.8530 support line which was highlighted in our previous analysis piece on the pair as a level which was likely to break.

The market has repeatedly attempted to break below but been unsuccessful. When a level comes under repeated attack like this it is often the case that the market will eventually prevail.

An illustrative metaphor would be that of a stone being skimmed across a smooth pond - although it is likely to bounce off the water several times, eventually it will penetrate the surface and sink.

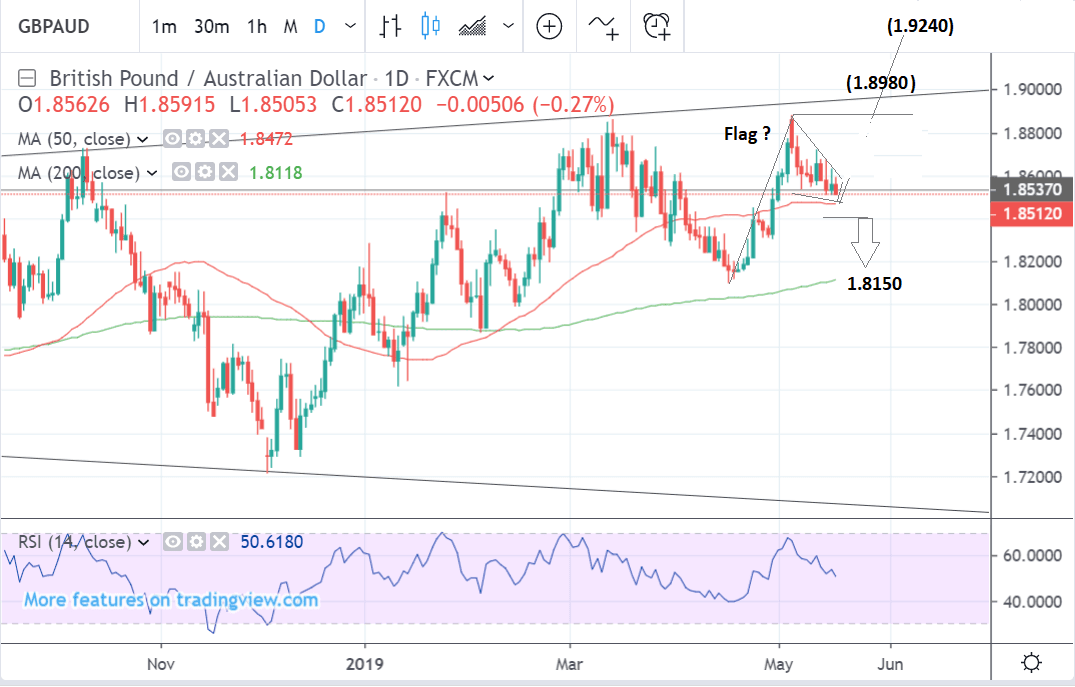

The daily chart is more ambiguous. The pair shows a possible bullish flag continuation pattern forming which seems to raise the possibility of a continuation higher rather than lower.

Yet overall our forecast remains bearish and we expect price action to continue to decline despite the obstruction of the 50-day moving average (MA) which is situated just below price action at 1.8474, and is likely to present significant support going ahead.

For a stronger bearish confirmation, the pair would have to break clearly below the 50-day MA, confirmed by a move below 1.8430. Such a decline would suggest a continuation down to a target at 1.8150, just above the 200-day MA.

It is still possible the bull flag hypothesis may play out. If the pair goes higher and clearly breaks above the 1.8883 flag pole highs would flip the outlook and signify a likely continuation to a possible initial target at the top of a trendline at 1.8980, followed by an eventual target at 1.9240.

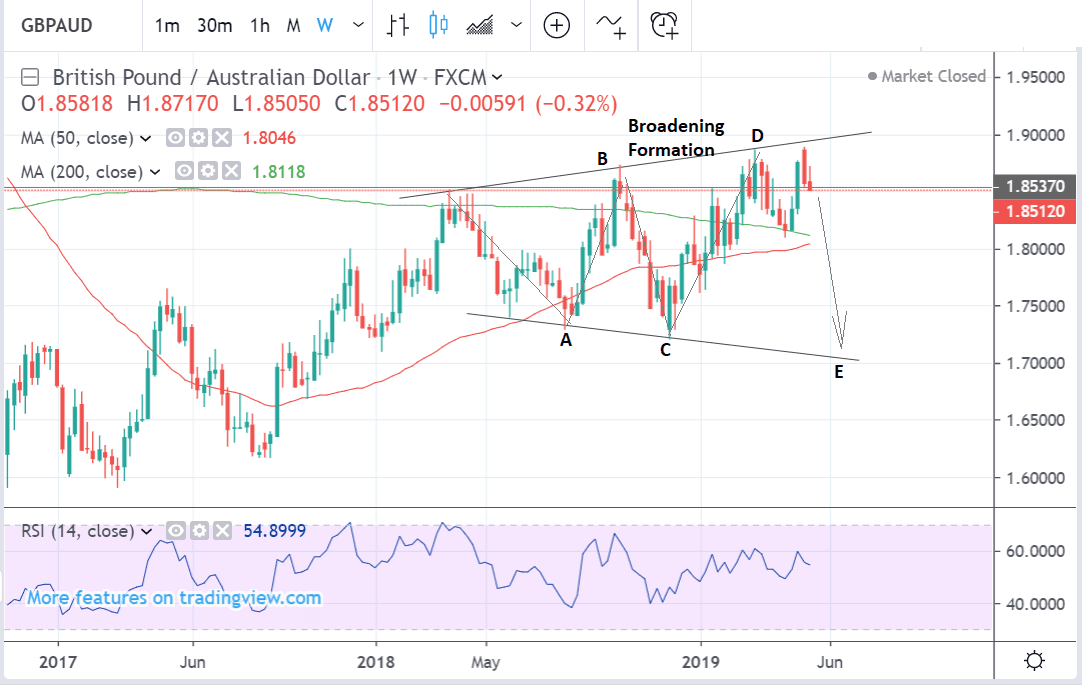

The weekly chart adds further bearish evidence as it shows the possible formation of a broadening formation (BF), which looks like a loudspeaker and shows a widening market. Normally when these occur at tops such as this, it results in an eventual break lower.

BF’s are usually composed of 5 waves, labeled A-E, and we have probably just completed wave D and are on our way lower in the next wave, ‘E’, which should stretch all the way down to 1.70-72 and the bottom of ‘D’.

Time to move your money? Get 3-5% more currency than your bank would offer by using the services of foreign exchange specialists at RationalFX. A specialist broker can deliver you an exchange rate closer to the real market rate, thereby saving you substantial quantities of currency. Find out more here.

* Advertisement

The Australian Dollar: Election Bounce to be Short-Lived

The main fundamental drivers for the Australian Dollar in the coming week are likely to be global risk trends, the Reserve Bank of Australia (RBA) meeting minutes and Australian PMI data.

"With the uncertainty from the election now out of the way, there could be a boost to confidence, but the question would be for how long. The global environment remains uncertain and trade tensions continue to linger," says Besa Deda, Senior Economist with St. George Bank in Sydney. "The Australian dollar is higher after the election result, but attention will quickly return to global issues and developments in the trade war."

Global risk trends are currently predominantly driven by trade tensions between the U.S. and China. This affects the Australian Dollar because of its exposure to China which is its most important trade partner. Relations worsened recently after both superpowers decided to increase tariffs on each other's goods. This hit the Australian Dollar hard, which fell on the news.

Responding to the news of the Liberal-National coalition's victory, China's English mouthpiece the Global Times said: “Australian election result will continue current poor relations with China. Canberra took the lead among Western countries to boycott Huawei, plus a series of anti-China decisions, making Chinese believe Australia is the most radical Western country in helping the U.S. suppress China”.

There appears to be little basis for optimism tensions will improve in the short-term, not until Trump and Xi meet at the G20 summit on June 28-29.

One major risk factor is that the U.S. widens tariffs to impact on a wider array of Chinese imports, and China retaliates by, perhaps, increasing the already high tariffs it charges on U.S. goods. This would further undermine the Australian Dollar.

The key domestic release for the Aussie Dollar this week is PMI survey data for May, released on Wednesday, May 22, since PMIs are widely seen as a leading indicator for the economy, which has been slowing of late.

Previous Manufacturing PMI stood at 50.9 in April and Manufacturing at 50.1. Any declines could weigh on the Aussie Dollar, particularly if they take PMIs below the 50 level which distinguishes expansion from contraction.

“Leading economic indicators suggest the economy will continue to slow, although next week’s manufacturing and services PMIs may give markets an indication of just how pronounced the deceleration may be,” say Wells Fargo in a note to clients. “As of now, both PMIs remain in expansion territory, but been trending lower since the end of 2018.”

Finally the Aussie could be impacted by the minutes from the RBA’s May policy meeting, out at 2.30 BST on Tuesday.

The Australian Dollar is currently at risk from the Reserve Bank of Australia (RBA) deciding to cut interest rates.

"A potential upcoming RBA rate cut remains on the cards, providing further event risk for the AUD. After a lift in the unemployment rate released last week, the odds for a rate cut by the RBA have lifted to around 70% for June, and nearly fully-priced in for July," says Deda.

The RBA decided not to cut interest rates at its last meeting citing continued labour market resilience as a reason. Recent data brought that into doubt, however, after unemployment rate rose to an 8-month high of 5.2% in April.

The minutes will provide more detail on the decision taken in May and may have an impact on the exchange rate if it reveals a surprise change from the official neutral stance or reasons to expect one imminently.

The Pound this Week: Euro Elections, Inflation Data

Overshadowing most data for Sterling will probably be Brexit risks and political uncertainty from the EU elections.

The Pound has nosedived since news cross-party talks fell apart. One catalyst for the disintegration has been the strong support polled by the new Brexit Party in the run up to the EU elections, on Thursday May 23, and correspondingly weak support polled by the Conservatives.

The inference is that Tory voters have changed allegiances and joined the Brexit party. This seems to be hardening the Conservative Party's stance on Brexit, widening the gulf between them and the other major parties.

Pressure is now also growing for the Prime Minister to resign, especially if her deal fails its fourth and final meaningful vote at the start of June, and Boris Johnson, who is a Brexit 'hawk', is the frontrunner to take over.

If he does it will increase the risks of ‘no-deal’ as we believe the next Prime Minister will pursue a policy of 'Brexit at all costs' come October 31.

“A poor showing by the UK Conservatives in the European Parliament elections could make it even more likely that Theresa May is replaced with someone that wants to deliver Brexit ‘no matter what’, keeping the Pound on the back foot,” says Raffi Boyadijian, an economist at FX broker XM.com.

Other events, however important during ‘normal’ times, are likely to be overshadowed by political risks, even inflation data out at 9.30 BST on Wednesday, May 22, and the testimony of the governor of the Bank of England (BOE), Mark Carney at 9.30 on Tuesday, May 21.

Inflation is expected to show a big rise in April, increasing by 0.7% on a monthly basis and 2.2% compared to a year ago. This would reflect a considerable acceleration from March when inflation only rose by 0.2% and 1.9% respectively.

Core inflation, which strips out volatile food and fuel components, is forecast to rise by 0.4% month-on-month and 1.8% compared to a year ago. This compares to 0.2% and 1.8% respectively in March. The core figure is not expected to show the same acceleration as broad CPI, as inflation recently has been driven primarily by rising oil prices, which impact on petrol prices.

Commentary from the governor of the BOE, Mark Carney, and other members of the BOE rate-setting committee, also potentially moving markets.

Although Governor Carney’s comments to the Parliamentary treasury committee may move the Pound, heightened Brexit uncertainty may make him ambivalent, and there is a risk of a U-turn from his May meeting confidence when he said investors should guard against complacency over inflation. The BOE’s stance at its May policy meeting was that it planned to raise interest rates over coming months at a "gradual and limited" pace.

Retail sales data is the final major release on the calendar, and is forecast to show a -0.4% slowdown from March, partly because of the outlying stellar performance in April when it rose 1.4%. It is forecast to rise by 4.6% compared to a year ago, after it grew 6.7% in March compared to the previous year. If sales are strong it could boost the Pound as it will show consumers continue to spend generously, which is a key indicator of overall economic growth for a nation.

* Advertisement