Image © Filipe Frazao, Adobe Stock

- GBP/AUD turned higher last week

- Young uptrend is expected to extend higher

- Brexit vote result to lead Sterling; geopolitics to drive AUD

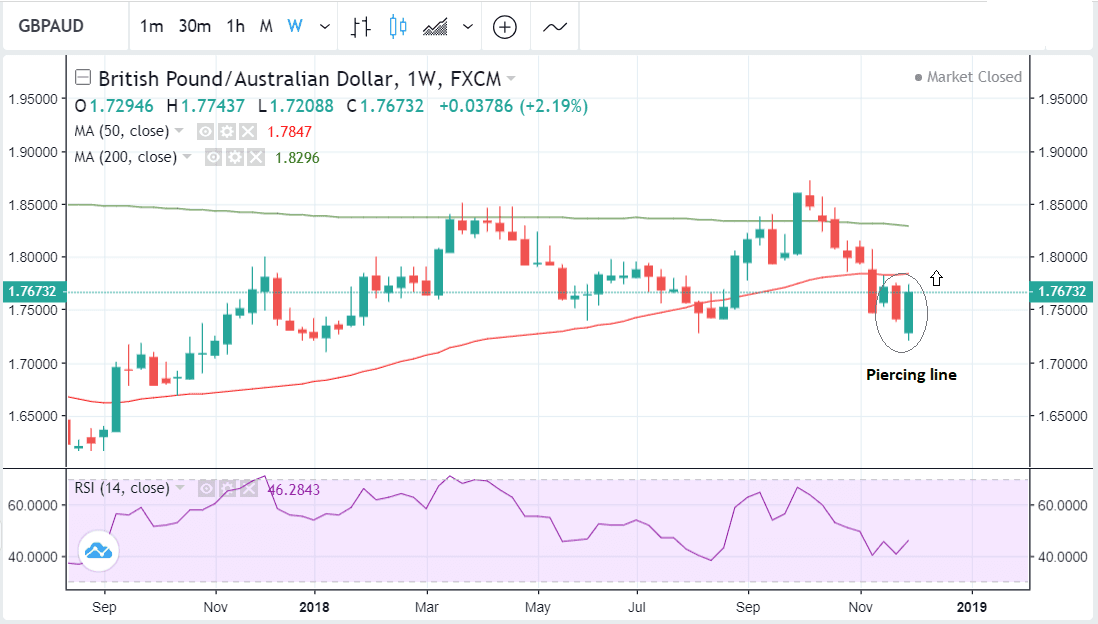

The Pound-to-Australian Dollar exchange rate rose over 2.1% in the previous week to close at 1.7673.

Although it is too early to say for sure, the Aussie fell so sharply against the Pound that it appears that GBP/AUD has now probably reversed its previous downtrend. The probabilities now marginally favour the start of a new uptrend in the week ahead.

From a technical standpoint, the pair is showing multiple trend-change signals. On the weekly chart, it has formed a bullish ‘piercing line’ Japanese candlestick pattern which augurs well for the future. Another bullish candle next week would provide added confirmation.

The 50-week moving average (MA) situated at 1.7847, not far above the ‘piercing line’, however, is likely to prove an impediment to further upside, and we expect the exchange rate to stall once it touches it.

A break above the 1.7743 highs is likely to run into resistance at the level of the 50-week MA and this is why we have adopted it as our initial upside target.

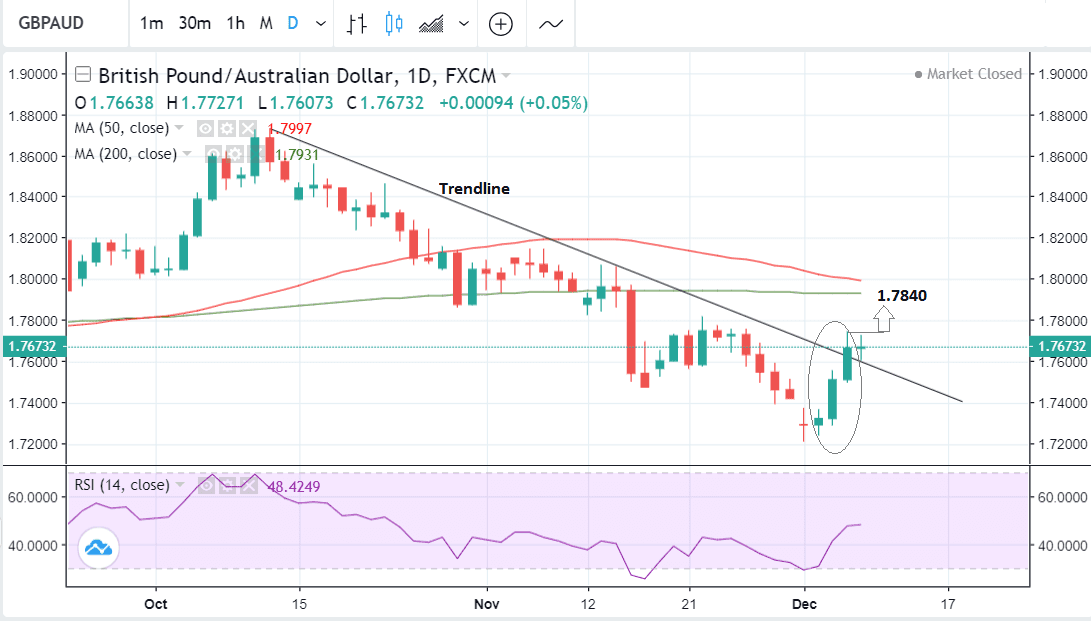

The daily chart shows that, after gapping down on last Monday morning, the pair appeared to bottom and then spent the rest of the week rallying. The gap is probably what analysts call an ‘exhaustion gap’ which comes at the end of trends. This further increases our confidence that the pair is changing trends.

The pair has also rallied straight through the trendline drawn down from the October highs. This is a further bullish signal and suggests more upside. Normally, the price is expected to extend the same distance above a trendline as the move immediately prior to the trendline. This suggests it has higher to go.

The fact the pair completed three green up-days in a row is also a sign the old downtrend has finished and a new trend higher has started.

Advertisement

Bank-beating GBP/AUD exchange rates. Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here

The Australian Dollar: What to Watch

The most important fundamental driver of the Australian Dollar in the coming week is likely to be external in nature.

Of interest is the growing diplomatic crisis between Beijing and Washington over the arrest of Meng Wangzhou, the CFO of Chinese mobile phone company Huawei, (and daughter of its owner) over her alleged fraud to avoid US-imposed trade sanctions on Iran.

Meng is being held in Canada pending extradition to the U.S. for trial. China has demanded she be released, saying her detention is, “unreasonable, unconscionable and vile in nature.”

There are concerns that the incident could sour the trade war ceasefire struck between the U.S. and China in Argentina at the G20 summit, an outcome that bodes well for global risk sentiment which in turn favours the Aussie Dollar.

"The long awaited squeeze in the AUD has materialised. This looks to be little more than a positioning adjustment, with few substantial changes in train. The domestic data flow has started to turn, but for now the global environment continues to dominate moves, and we see a number of risk events (U.S.-China tension, Brexit) that could take a toll on the AUD," says a Daniel Been, a foreign exchange strategist with ANZ Bank.

On the domestic data front, a major event to watch is the RBA economic Bulletin on Thursday at 00.30 GMT, which could provide investors with an insight into its stance on monetary policy.

Guy Debelle, the assistant governor of the RBA recently said further interest rate hikes were ‘a long way off’, and if this sentiment is reiterated in the Bulletin it is likely to weigh on AUD.

Other key data in the coming week includes a welter of housing data.

Home Loans out at 00.30 GMT on Monday are forecast to read at -0.5% for October, having fallen 1.0% in the previous month.

The quarterly House Price Index out at 00.30 on Tuesday is forecast to read at -1.5%, for the third quarter, a doubling of the -0.7% decline seen in the previous quarter.

New Home Sales are out at 00.00 on Thursday, and while new forecast is available we know the previous month's reading of -0.8% confirms a trend of a sector under pressure.

This could impact on the Aussie because the housing sector is in decline in metropolitan areas and many economists fear the situation could worsen and pose a financial stability risk (AUD negative).

Martin Elund, an economist with Nordea Markets says housing is a factor to watch as the risk growing in the sector "is alive and kicking still".

"For how long can the RBA watch from the side-lines with such a house price development? The weakness was noted by RBA last week, but they are still far from acknowledging the magnitude of the risks associated with the Australian housing market," says Elund.

The Westpac consumer sentiment survey in December is another key release for the Australian Dollar which is out on Wednesday at 23.00.

The Pound: What to Watch

Despite rumours the vote may be postponed, the coming week promises to be busy for Sterling if the crucial Brexit vote in Parliament goes ahead.

It is an event which has the potential to start a new era for the Brexit story and Theresa May’s future in her role as Prime Minister and leader of the Conservative party.

Parliament’s meaningful vote on the government’s Brexit deal is scheduled for Tuesday 11, at 19.00 GMT. The government is currently expected to lose the vote and this could cause some short-term weakness for the Pound.

Rumours have surfaced over the weekend that the vote could be delayed whilst Theresa May attempts to draw more concessions from Brussels, but further clarification from Downing Street confirm the vote will indeed progress as planned.

For Sterling, the extent of the loss is key. If the loss is smaller than expected, May will take heart that some further concessions on the political declaration from European leaders can help the deal go through.

"We would not expect Sterling to slump if she loses by a narrow margin," says Thomas Pugh with Capital Economics.

If the government loses by 200 or more votes Theresa May could resign. She could also simply head back to Brussels and insist talks are reopened telling the European Union if they do not a 'hard Brexit' becomes inevitable.

The Labour party may also force a vote of no-confidence which could lead to a general election if the government loses, however this would require some Conservative party MPs to vote with the opposition, which is unlikely.

"A decisive defeat could have a more significant market impact though. Theresa May might have to face down a vote of no confidence in the government and a leadership challenge, which would rattle markets," says Pugh.

A second referendum is also said to be a further possible outcome, however we doubt there is a majority in the House of Commons for this.

The bottom line? No one quite knows what will happen next.

"Political uncertainty is likely to continue to hang over the economy for at least the next few months," says Pugh.

Beyond Brexit, a major release for the Pound is GDP data, which is forecast to show a slowdown in October when it is released at 9.30 on Monday. The average over the previous 3 month period was 0.6% but this is expected to slow to 0.4% in the most recent period.

Industrial and Manufacturing production are also released at the same time and forecast to show a slowdown.

Industrial production is expected to show a -0.1% decline in October, and Manufacturing a 0.0% change.

Labour market data is forecast to show little change in November with the unemployment rate stuck at 4.1% and pay excluding bonuses at 3.2% whilst pay including bonuses continues to show a 3.0% rise. Overall employment change is expected to show a 20k rise.

"We expect to see another robust, if unspectacular, rise in employment in the three months to October. Meanwhile, wage growth probably edged up further," say Capital Economics.

Finally, balance of trade data is out on Monday at 9.30. The deficit in the previous month of September was a very marginal -£0.03bn.

"We think the trade balance slipped back in to deficit in October, as imports rebounded and the recent strength of exports came to a halt," says Capital Economics in a note covering the coming week. "Surveys also suggest that exports, which performed well in recent months, fell back in October."

Advertisement

Bank-beating GBP/AUD exchange rates. Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here