Image © Greg Brave, Adobe Stock

- GBP/AUD to continue downtrend on Brexit tensions

- Break of key levels needed for confirmation

- Brexit news to drive the Pound; employment data main release for AUD

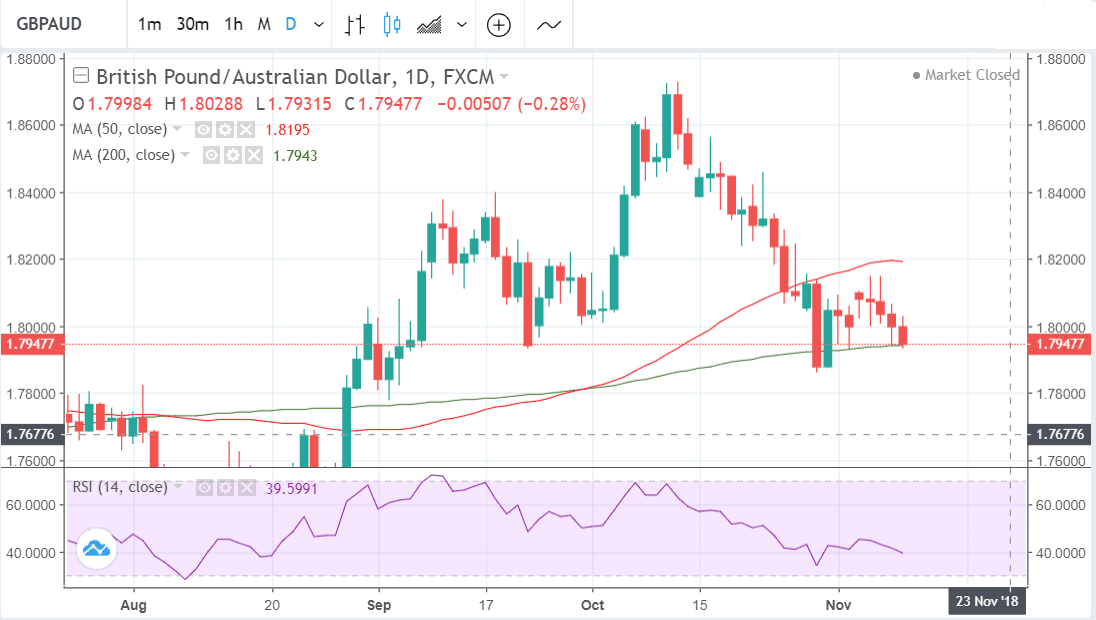

The Pound-to-Australian Dollar exchange rate starts the new week 0.45% in the red at 1.7872, its lowest level since September 05.

The pair has fallen for seven consecutive days and five consecutive weeks ensuring the trend is certainly one of weakness over short- and medium-term timeframes.

The fundamental backdrop for the exchange rate bodes ill amidst reports over the weekend that the E.U. have rejected U.K Prime Minister Theresa May's latest Brexit proposals.

Putting our technical cap on, we note some potential respite: the GBP/AUD pair has a now touched down on an important support level at the 200-day moving average (MA) at 1.7943. This is likely to provide a robust floor which could be difficult for the pair to break below.

Overall because of the 5-week decline from the 1.87 highs we see a continuation of this short-term downtrend as the most probable forecast in the week ahead.

Ideally, we would wish to see a break below the MA and the trendline tracking the rally from the August 2017 lows for confirmation first.

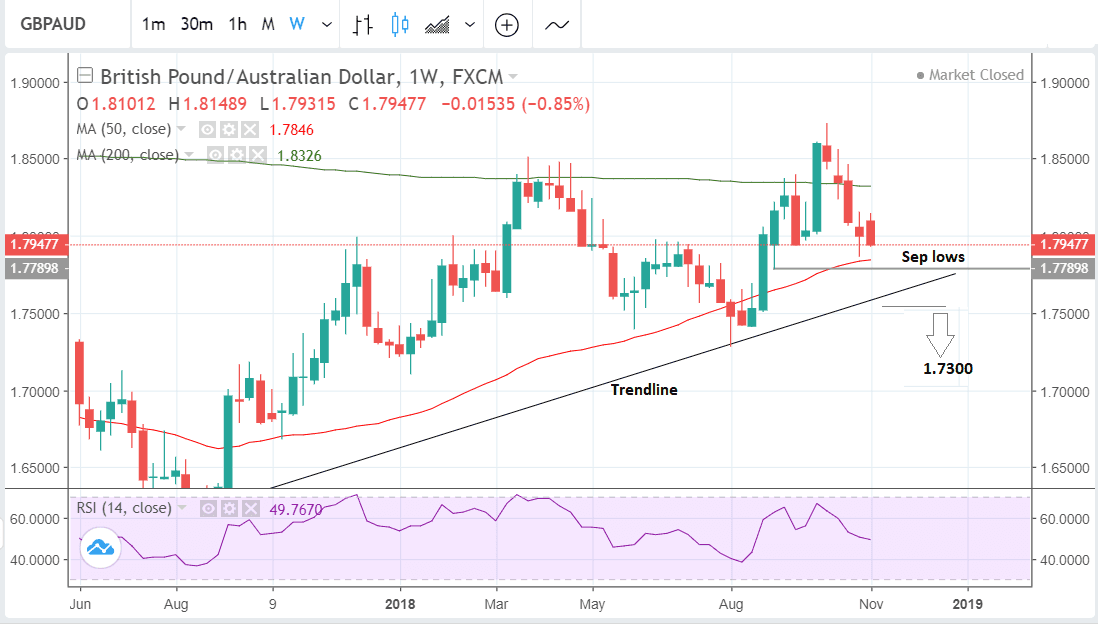

A break below the 1.7515 level would provide the necessary confirmation, opening up a downside target at the 1.7300 August lows.

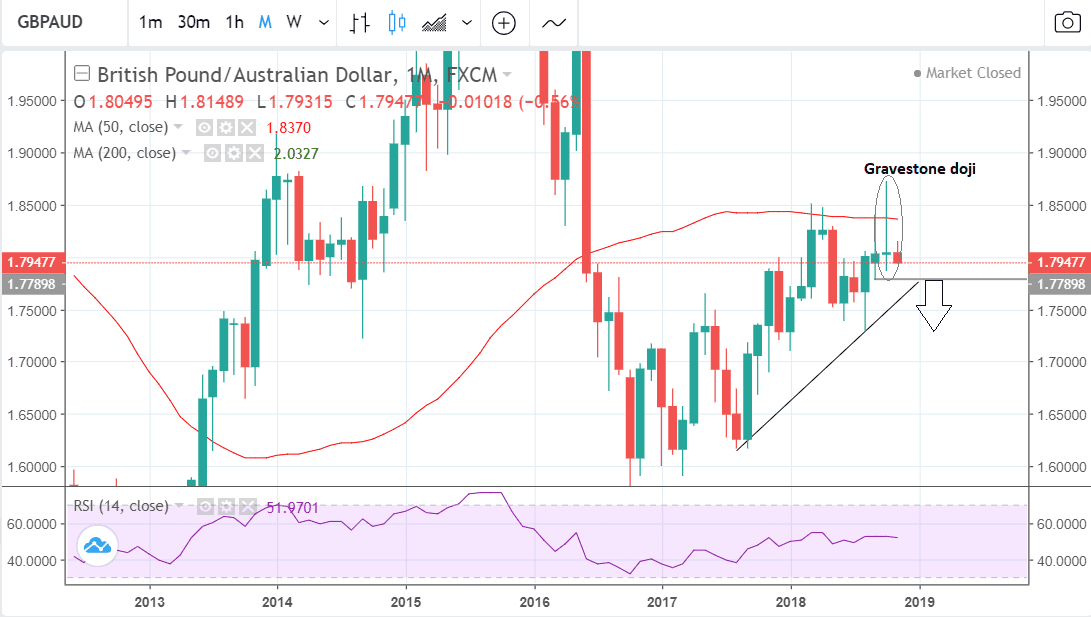

A move below the September lows at 1.7779 would also provide bearish confirmation as it would signal a pivot swing around the October peak and the gravestone doji candlestick pattern formed in October.

Advertisement

Bank-beating GBP/AUD exchange rates: Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here

The Australian Dollar: What to Watch this Week

The Australian Dollar remains highly sensitive to developments concerning China and global trade: we have noted of late the currency's tendency to mirror the fortunes of the Chinese Yuan.

Therefore, the global picture will matter. A question that we are particularly interested in getting answers to is that regarding how U.S. President Donald Trump will approach his trade war with China in the wake of his loss of the House of Representatives in the recent mid-term vote.

Does he ramp up the heat on China, or does he pursue the image of deal-broker?

The former scenario is likely to be highly negative for the Aussie, the later highly constructive.

Watch the headlines and Trump's Twitter account in this regard.

The main release for the Australian Dollar in the week ahead is employment data on Thursday at 00.30, which forecast to show the unemployment rate rising by a basis point to 5.1% in October and a 20.3k increase in total jobs.

Signs of an improvement in the labour market are likely to have a positive effect on the Australian Dollar, since they imply greater economic growth and therefore higher interest rates. Higher interest rates tend to strengthen a currency by increasing foreign capital inflows, drawn by the prospect of higher returns.

The other main release for the Aussie is NAB Business Confidence in October. In September the sentiment indicator showed a marginally positive balance of 6.

The Pound: What to Watch

The main driver of the Pound in the week ahead is likely to be Brexit news.

If it looks like a withdrawal deal is on the table the Pound will rise, and vice-versa if the opposite.

The headlines from the Sunday Times are indeed worrying: if true then it might be the case that Theresa May will have to walk away from negotiations as she simply won't be able to muster parliamentary support for a wildly unpopular deal that risks the U.K. being subjugated to E.U. law indefinitely.

Yet, we always knew these negotiations would go down to the wire and with December being the final deadline we are not surprised by these negative headlines.

Markets could be accused of becoming far too optimistic on the state of Brexit negotiations of late. The E.U. always negotiates until the very end; and we are seeing just this.

That is also possible gains on any deal may be short-lived as even if the government announces a deal it will still have to get approval from Parliament, and this could be an arduous process, presenting a risk to Sterling.

The conservative government only has a small majority and is reliant on support from the DUP and every single one of it MPs, so there is a risk that if either the DUP or Brexit rebels vote against the deal Theresa May may find she does not have the majority to push it through, and this could weigh on the Pound.

On the hard data front, one of the most significant releases in the week ahead is likely to be inflation data for October, which, according to the market consensus, is forecast to show a 0.2% rise on a month-on-month (mom) basis and 2.5% rise on a year-on-year (yoy) basis (for headline inflation) when it is released on Wednesday at 9.30 GMT.

A result in line with expectations would probably be bullish for Sterling as higher inflation puts pressure on the central bank to raise interest rates which appreciates the currency.

This is because higher interest rates tend to attract more inflows of foreign capital drawn by the promise of higher returns.

There is a chance, however, that inflation will disappoint because of the waning influence of the cheap Pound which has appreciated on Brexit hopes. Headline CPI has already fallen from a peak of 3.0% in January due to the bounce in the Pound, so more losses are possible - although if comments from the Bank of England (BOE) are anything to go by unlikely.

"In its most recent meeting, the Bank of England (BoE) noted that it does not expect inflation to fall much further, with price growth instead holding fairly steady near the 2% target," say Wells Fargo in a note to clients.

Another major release for the Pound is labour market data out on Tuesday at 9.30. Probably of most significance to Sterling is the average earnings component because of its influence on inflation. The current expectation is for a rise of 3.0% in Earnings (including bonuses) and for a rise of 3.1% in earnings excluding bonuses. A result in line with expectations could be positive for the Pound as it will reflect an even stronger rise in real earnings since the fall in inflation from its January peak.

Other results of note within the labour report are unemployment, which is forecast to remain at 3.0% and employment change which is forecast to rise by 34k.

The final major release for the Pound is retail sales on Thursday, which is forecast to show a 0.2% rebound in October, from a rather weak -0.8% previously, and a 2.8% rise yoy from 3.0% previously, when it released at 9.30 GMT.

Advertisement

Bank-beating GBP exchange rates: Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here