The South African Rand’s dramatic slump over recent days has left it looking notably undervalued, and therefore the prospect of a recovery over coming weeks is elevated argues the foreign exchange research team at ING Bank N.V in London.

ING have updated their clients with their latest forecasts for the Rand following the recent upheavals in the country and while some further losses for the currency are likely near-term, the currency should head back to fairer valuations.

The Rand is however trading as a political currency and any expectations for recovery do therefore rely on the assumption that the South African administration will settle down and keep previous policy decisions intact.

“Unless the new team start to undermine Gordhan’s 2017/18 fiscal plans or the SARB is pressured into early rate cuts, we expect investors will continue to find value in the ZAR,” says ING analyst Chris Turner in a note to clients dated April 6.

The Rand had been steaming ahead and was one of the better-performing global currencies before President Zuma purged key members of his cabinet including Finance Minister Pravin Gordhan.

The move came at a time when Rand assets, particularly debt, were in strong demand.

Best Performer

Up until the cabinet re-shuffle of 30 March, the ZAR had been one of the best performing emerging-market currencies this year.

Driving that strength, say ING, was the global reflationary story – not just Trump’s possible fiscal stimulus, but also the prospect of more synchronised global growth.

“Expectations of higher growth in 2018 have lifted growth prospects amongst the commodity exporters in particular. South Africa’s key exports, precious and industrial metals, have performed well in such an environment,” says Turner.

It was all going so well until politics intervened.

Politics: What to Watch

For Rand watchers, the political pulse will be key going forward.

President Zuma’s purge of Pravin Gordhan and six other cabinet ministers has naturally un-nerved investors.

The move has proved divisive within the ANC executive team and the opposition has proposed a No-Confidence motion in Zuma – to be debated on 18 April.

“However, it seems unlikely that an ANC dominated National assembly would allow such a motion to pass,” says Turner who will be watching the ANC Congress in December, when a new leader will be chosen.

“While Jacob Zuma will retain Presidential power until general elections in 2019, the choice of a new ANC leader (and likely future President) will give an indication as to the direction of travel,” says Turner.

Sovereign Debt Ratings and Junk Status? It’s in the Detail

South Africa’s financial system and economy require large external funding requirements as the country is a net importer and ongoing portfolio inflows are critical to financing South Africa’s current account deficit.

This requires that investors continue to see value in South Africa’s large stock of debt and equity assets.

Notably this year’s inflows into South Africa have largely been into sovereign bonds - otherwise known as debt markets.

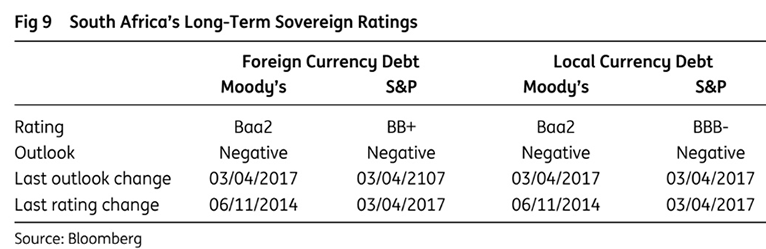

South Africa’s ability to issue debt in local currency means that South Africa’s share of hard currency in its external sovereign debt is a relatively small 10%.

The credit rating downgrade assigned in the wake of Gordhan’s dismissal was only assigned to foreign currency debt which is now loosely termed as junk.

The local currency rating, while also cut one notch, still sits as investment grade.

This is a subtlety that many might have missed amongst the shock of being ‘downgraded to junk’ and is important for the currency.

As a result, the impact on the Rand and financial system was not as bad as it could have been - what would really matter is the downgrading to junk of local debt which as we have noted accounts for about 90% of South Africa’s debt.

According to the IMF US$2bn of outflows would result from the downgrade to junk status of the foreign currency rating, but a more sizeable 2.5% of GDP (around US$8bn) of outflows should be realised were the local currency rating be cut to junk.

ING note that the reason for this much larger reaction to the local currency, rather than the foreign currency rating, is because of key local currency sovereign bond indices such as Citi’s WGBI and Barclays Global Aggregate Index which require Investment Grade status for inclusion.

Turner notes that a move by both S&P and Moody’s is required to prompt removal from the index.

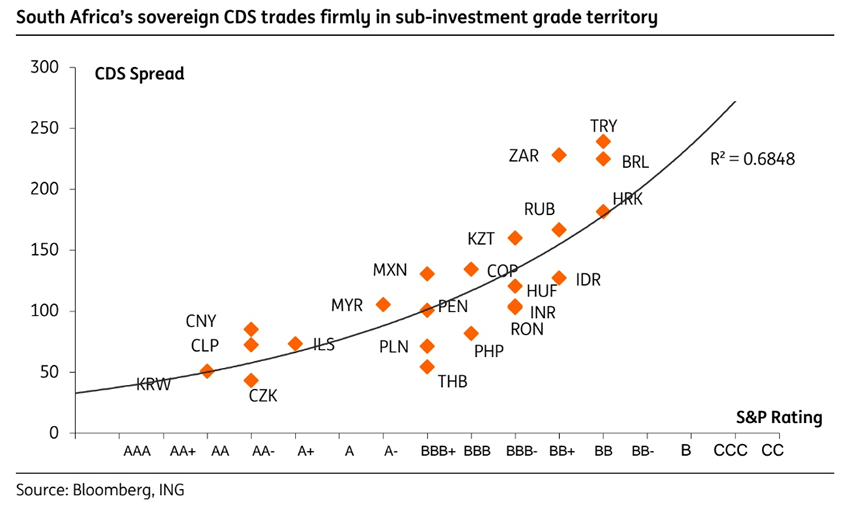

How far is the South African local currency sovereign rating away from junk?

As per the above, S&P is one notch away from junk, Moody’s two.

Moody’s has South Africa on a negative outlook, which looks likely to result in a downgrade over the next 30-90 days.

“Whether Moody’s keeps South Africa on a negative outlook, after a downgrade, will be important. Even a negative outlook could take another 12-18 months to resolve. That means the more dangerous scenario of both S&P and Moody’s local currency sovereign ratings being cut to junk may only be a 2018 story, if at all,” says Turner.

Rand Undervalued, Should Move Higher

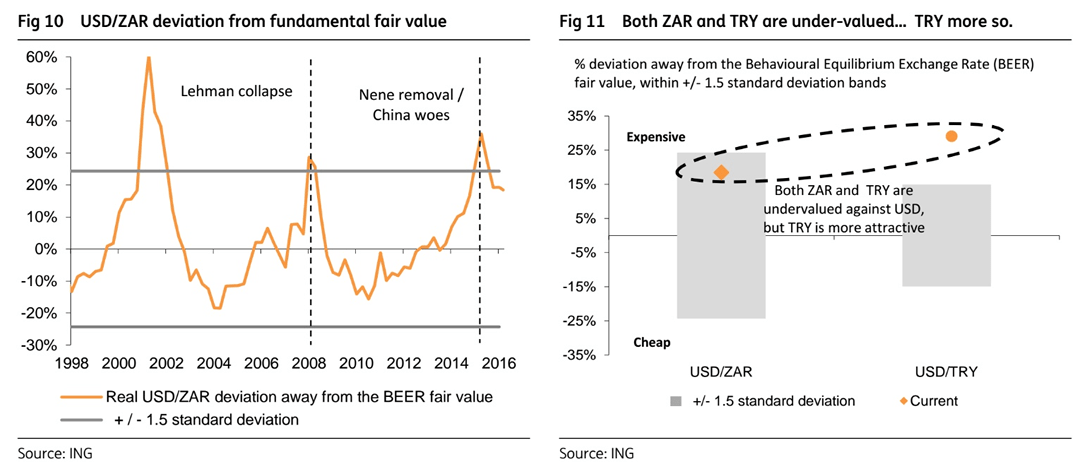

Another key reason as to why ING believe the recent ZAR sell-off has been quite limited this time when compared to previous episodes is owed to valuation.

ING’s Petr Krpata’s has worked on medium term fundamental valuation (BEER) and he sees the Rand being undervalued against the US Dollar by around 18%.

This compares to around 9% undervaluation during the ZAR’s recent peak two weeks ago.

“While meaningful in absolute terms, it is important to note that the current ZAR misvaluation is not far away from the upper 1.5 standard deviation band limit,” says Turner.

The deeper into undervalued territory a currency goes, the harder it becomes to push it even lower.

The last two times the Rand persistently traded through these valuation limits were during:

(1) the post Lehman collapse EM sell-off;

(2) the extreme Rand fall in late-2015/early-2016 (a mix of both internal political woes and external concerns about China).

“This suggests the scope for another large scale sell-off looks limited from here,” says Turner.

While the current ZAR valuation does look attractive, ING note that on a comparative basis it is not as attractive as the Turkish Lira’s valuation.

The Turkish Lira is meaningfully more undervalued than ZAR (following the large scale Lira sell-off during 2H16 and the early part of 2017), with the Lira being extremely stretched even by its own standards.

In addition to the benign environment supporting the carry trade, rising policy uncertainty in developed markets has encouraged diversification into emerging-market assets.

ING argue that the convergence of developed-market economic uncertainty on to that of emerging-market is one of the reasons why the recent ZAR sell-off has been more limited than that seen in December 2015 – when President Zuma removed Finance Minister Nene and his replacement survived three days.

South African Rand to Recover

The Rand is therefore a currency that is undervalued and still - arguably - a currency that is underpinned by investment-grade debt.

“On the assumption that key institutional/fiscal confidence does not erode – and that the central bank does not come under any pressure for easier policy (no signs as yet) - we think ZAR under-valuation will dominate over coming quarters,” says Turner.

A firmer ZAR would be consistent with ING’s generally bullish view on the commodity currencies which sees AUD/USD back to 0.80/85 on a 12/24 month basis and USD/CAD back to 1.30.

ING think continuity of the Zuma administration, surviving a no-confidence motion, could see USD/ZAR trade into the 14.00/50 region in 2Q17.

“Thereafter valuation metrics should come into play and expectations of stronger global growth into 2018, helped in part by clarity on what Trump can achieve, stand to drive USD/ZAR closer towards fundamental fair value levels closer to 12.00,” says Turner.

ING’s valuation models show the ZAR to be cheap on both a short-term financial fair value and also a medium-term fundamental basis.

In a benign reflationary environment, the bank sees USD/ZAR upside limited to 14.00/50 and favour 12.00 in a year.