The GBP/ZAR has been falling steadily for months, reaching a 2017 low of 15.56 ahead of the Bank of England’s March policy meeting.

In fact, the Pound to Rand conversion has fallen in value by 6.5% over the course of 2017 and is the worst-performing major Sterling pair.

A reversal in Sterling following the Bank's meeting put a floor under the pair and the GBP/ZAR charts show the formation of a hammer candlestick pattern. This is a technical term for a day with a small body in the upper part of the range and signifies the possibility of a reversal of the trend.

Therefore, the pattern has potentially important implications for those watching this market.

The hammer on its own is not enough to forecast a reversal but given the fact it came at the end of a long downtrend, and that the MACD momentum indicator has been failing to corroborate successive lows in the exchange rate – at least on the last three troughs - we see a much stronger possibility of a reversal.

As such a break above the 15.87 highs would help confirm the beginning of a young uptrend, with an initial target coming in at 16.00, followed by the 16.25 at the level of a major trendline. The pair would have to break above that to reconfirm further upside.

The Rand this Week

The news from the G20 meeting over the weekend was that the US had reaffirmed its commitment to protectionism which hurt global and emerging market risk appetite on Monday morning, and ZAR has suffered accordingly.

The one saving grace for South Africa, when compared to other emerging market countries at least, is its relative lack of direct exposure to the US.

Nevertheless, if the pace of protectionist rhetoric increases it may take a toll on the Rand.

The Rand has a major data dump on Wednesday when South Africa will publish CPI and Current Account data for February, at 08.00 GMT.

These are likely to show an improvement in the Current Account balance from -4.1% to -3.5% according to consensus estimates, which will be beneficial for the Rand.

Indeed, John Cairns of Rand Merchant Bank, sees the possibility of the deficit falling even further.

“Ongoing post-Fed dollar weakness remains the key driver but local data should also help: we expect only a 2.4% of GDP current account deficit in Wednesday’s release,” said Cairns in a note seen by Pound Sterling Live.

UK Inflation Dominates Outlook for Sterling

The main fundamental factors indicating the possibility of a bullish shift in GBP/ZAR is the assured tone concerning the UK economy put out by officials on the rate-setting committee of the Bank of England last week.

There is much debate about whether the BOE was right to be so optimistic at their meeting last Thursday, given data over the most recent quarter actually showed a marked decline compared to Q4 2016.

The risk of Brexit also hovers over Sterling, and may impact when Theresa May finally triggers Article 50, however, it is more likely to hurt the Pound when (or if) the direct economic ill-effects begin to be felt when the drastic cut in immigration and the severing of trade links take their toll on growth.

The main release for the Pound is CPI for February, out on Tuesday, March 21 at 9.30 GMT.

Market expectations of a rise to 1.8% are a little low according to both Capital Economics and TD Securities, who estimate a higher 2.1% and 2.2% rise year-on-year in Feb.

The main contributory factors are likely to be rising food inflation due to the weak Pound and the lagged effect of the rebound in oil prices.

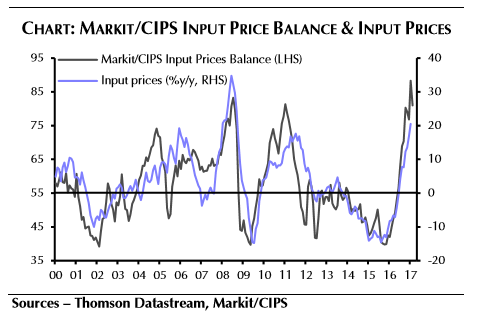

Producer Prices in the UK, out at the same time are expected to show continued extremely high yearly gains in ‘Input prices’ due to the rise in imported component prices because of the weak pound.

Capital expect Input prices to rise by 21.7% year-on-year.

Manufacturers are not passing the higher costs on, however, as output prices are only rising at a fraction of the level, of 3.5% currently, rising to 3.8% according to Capital.

“Meanwhile, the survey evidence suggests firms have been taking a hit to their margins. Indeed, the output prices balance of the Markit/CIPS survey has not risen by nearly as much as the input price balance. As such, we expect output prices to have increased only a little further, from 3.5% to 3.8%.,” said Holingsworth.

On Tuesday, March 21 at 9.30 Public Borrowing data is released and should show a small 1.0bn rise in February.

Nevertheless, borrowing remains below previous forecasts – down 22% on the previous year allowing the public finances some breathing room.

Given the government’s U-turn on increasing National Insurance contributions from the self-employed and lower-than-expected borrowing, the government does now have a buffer it can use to stimulate the economy in case of a Brexit-related slowdown, factors Sterling’s current rebound may be based on.

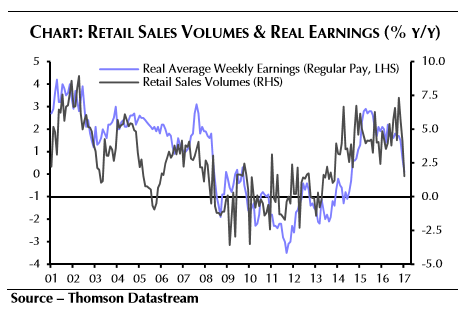

The final big news release for the Pound is Retail Sales at 9.30 on Thursday, March 23.

“February’s retail sales figures are likely to suggest that consumer spending is on track for a disappointing first quarter,” said Capital’s Hollingsworth.

He further notes this appears to be as a result of a correlated fall in real earnings growth.

The consensus market estimate is for sales to have risen by 0.4% month-on-month and 2.6% year-on-year, whilst Capital are slightly more optimistic seeing 0.5% and 2.7% rises respectively.

Notwithstanding this slightly brighter forecast the remain pessimistic about the outlook for Retail Sales in Q1.