- ZAR steadies after SARB holds rates in split November decision.

- Two SARB rate setters vote for a cut as inflation expectations fall.

- Risks to recovery rise with fresh shutdowns in U.S. and Europe.

- 'Lockdown' drives USD rebound & curtails emerging market rally.

Image © GovernmentZA

- GBP/ZAR spot rate at time of writing: 20.42

- Bank transfer rate (indicative guide): 19.71-19.85

- FX specialist providers (indicative guide): 20.12-20.24

- More information on FX specialist rates here

The Rand steadied late in a third consecutive session of losses Thursday after the South African Reserve Bank (SARB) left its interest rate unchanged, although with the Dollar resurgent alongside coronavirus containment measures in North America, the risk is of a further move lower for the currency.

South African Reserve Bank policymakers voted by three-to-two to hold the cash rate at 3.5% in November and until the New Year, with the dissenting two rate setters having voted for a cut to 3.25%, leaving the balance of risks tilted to the downside for interest rates also.

The SARB cited inflation that remains below the midpoint of the 3%-to-6% target and market expectations for even weaker price pressures ahead, a sombre environment for an inflation-targeting central bank that's expected to use rate changes to encourage an average 4.5% consumer price uplift each year.

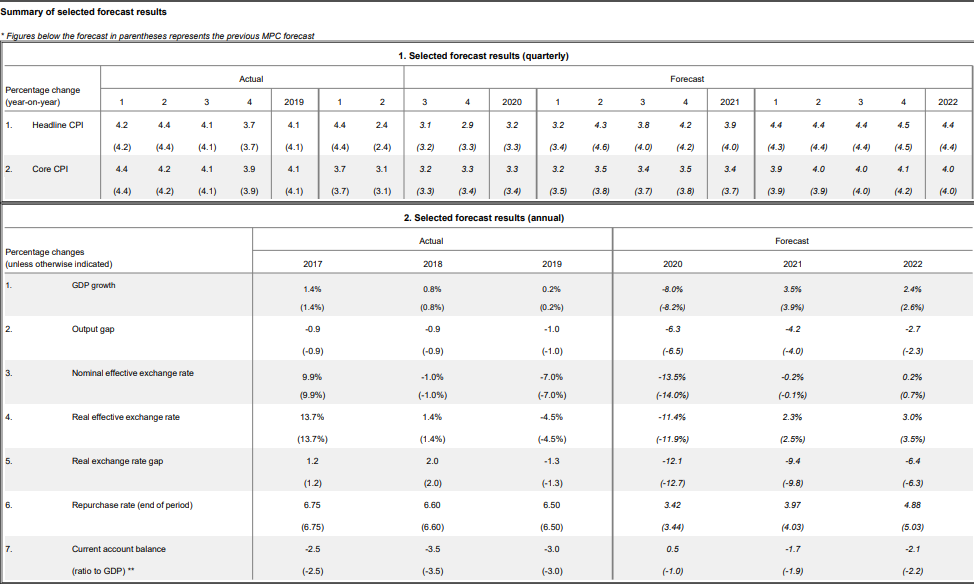

Above: South African Reserve Bank forecasts from November 2020. September forecasts in parenthesis.

Such an outlook might be expected in more ordinary times to prompt further cuts to the cash rate to spur economic growth which then lifts price pressures, although rates are already at a historic low and there comes a point for all central banks where cuts to borrowing costs can do more harm than good.

"The accommodative policies in many advanced economies and the improved economic outlook have supported a partial recovery in global financial markets. But this has so far resulted in only a trickle of fresh capital flows to emerging markets, and financing conditions remain uncertain," Governor Lesetja Kganyago said in a statement. "The yield curve remains exceptionally steep, reflecting elevated levels of risk associated with high public borrowing needs."

The SARB's quarterly projection model again that no further rate cuts should be implemented in the short-term while prescribing two 25 basis point rate hikes for late 2021, with one in the third and another in the final quarter.

Above: USD/ZAR shown at hourly intervals alongside Pound-to-Rand rate (blue line, left axis).

Inflation prospects weren't the only thing diminished as the SARB also downgraded forecasts for growth over coming years, which is now expected to lift GDP 3.5% and 2.4% in 2021 and 2022 respectively. Before, the SARB tipped increases of 3.9% and 2.6%. It now says risks to this outlook are "balanced" but also "tentative," due to the ongoing pandemic among other things.

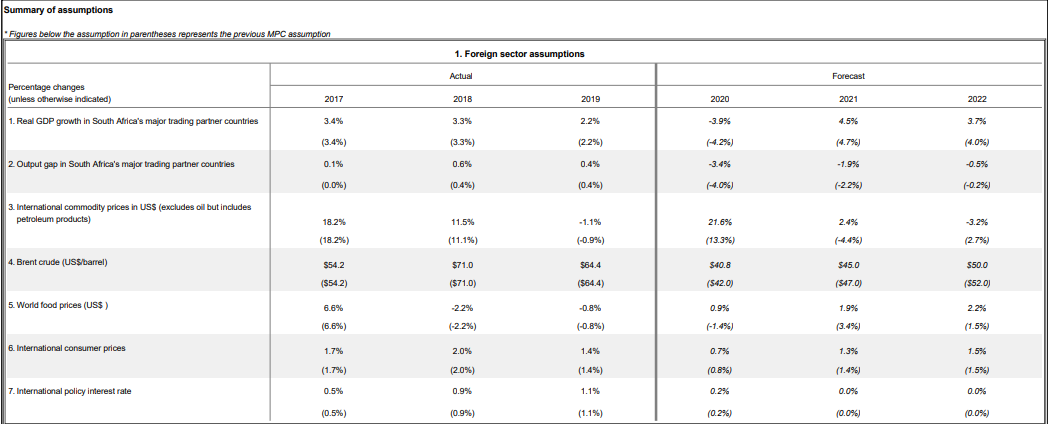

But domestic data was stronger than the SARB expected between September's decision and Thursday, indicating that reduced expectations for developed world recoveries could be behind its own more downbeat outlook for South Africa. Policymakers downgraded assumptions for trade-weighted GDP growth in major South African trade partner economies including the Eurozone, China, United States, Japan, Great Britain and India.

Three of those trading partners, notably the Eurozone, Britain and the U.S., were either already mired in a form of second 'lockdown' this week or were fast slipping into one. New York City Mayor Bill de Blasio was reported saying on Thursday that it's only a matter of time before the 'Big Apple' closes restaurants and bars again, just hours after schools were instructed to shut for a second time and as other U.S. states disrupted their own economies in the same way.

Above: South African Reserve Bank assumptions from November 2020. September assumptions in parenthesis.

"USD/ZAR has gone from its pre-COVID-19 pandemic peak of 19.00 to slightly shy of 15.00. We note that South African fundamentals have weakened amid this. Public debt is likely to hit 90% of GDP, levels of industrial and electricity production remain stagnant if not outright trending lower, unemployment has formally hit 30% and inflation remains at 3%. On net, we view most, if not all, of the fall in USD/ZAR as due to global tailwinds, not domestic," says Jacob Ekholdt Christensen, head of emerging market research at Danske Bank, who forecasts USD/ZAR to bottom out at 15.0 in the coming months.

Fresh shutdowns are already thought to have turned a final quarter European recovery into a double-dip recession but with the same fate now befalling the U.S. economy, the rally in risk markets has been curbed and the Dollar has risen broadly. Thursday's Dollar strength crimped the emerging market rally that had dragged USD/ZAR down near to 15.0 by Monday, while questioning the outlook for the greenback, stocks, commodities and risk currencies.

"We could see more emerging market strength in coming months as the reopening continues but on net, we cautiously suggest that we have seen the better part of this emerging market story. We recommend utilising these levels to lock in emerging market income, especially in countries where the rate differential has narrowed, where the currency has strengthened since March and where commodities or inflation are a key theme" says Danske's Christensen.

Above: USD/ZAR shown at daily intervals alongside Pound-to-Rand rate (blue line, left axis).

America's still-divided Congress had repeatedly failed to agree additional fiscal support for the U.S. economy even before the November 03 election appeared to make a 'lame duck' administration of the one which currently occupies the White House. If there is any stimulus that comes from Washington in response to fresh acts of economic self-flagellation by U.S. cities and states, it may ultimately be of a limited kind and not first without a stop-start and ever acrimonious political process taking place first.

This isn't necessarily conducive to investor confidence in the growth outlook or a weaker U.S. Dollar, nor for further upside in stocks and emerging market currencies, although there is a consensus in some parts of the market and among analysts that argues a possibly inevitable Federal Reserve (Fed) response to this set of circumstances will be dilutive of and harmful to the Dollar. As a result, many forecast continued declines for the greenback and further gains for the Rand in the months ahead.

"The logic is that a divided US Congress is expected to be less efficient at providing fiscal stimulus, which will require monetary policy to do more of the heavy lifting, i.e. rates should remain lower for longer. In addition, it’s expected that tensions between China and the US may ease now that electioneering is over," says Nema Ramkhelawan-Bhana, head of research at Rand Merchant Bank, which forecasts a final quarter range of 15-to-17.10 for USD/ZAR. "We believe that the next few months at least should be dominated by a weak dollar and a continued recovery in commodity prices.