Image © Adobe Images

- Short-term bounce meets tough resistance

- Uptrend to continue assuming break above highs

- Pound driven by BOE meeting; Rand by fortunes of U.S. Dollar and global sentiment

The Pound-to-Rand exchange rate is trading at 18.53 at the time of writing, 0.86% higher than where it was located at the same time last week.

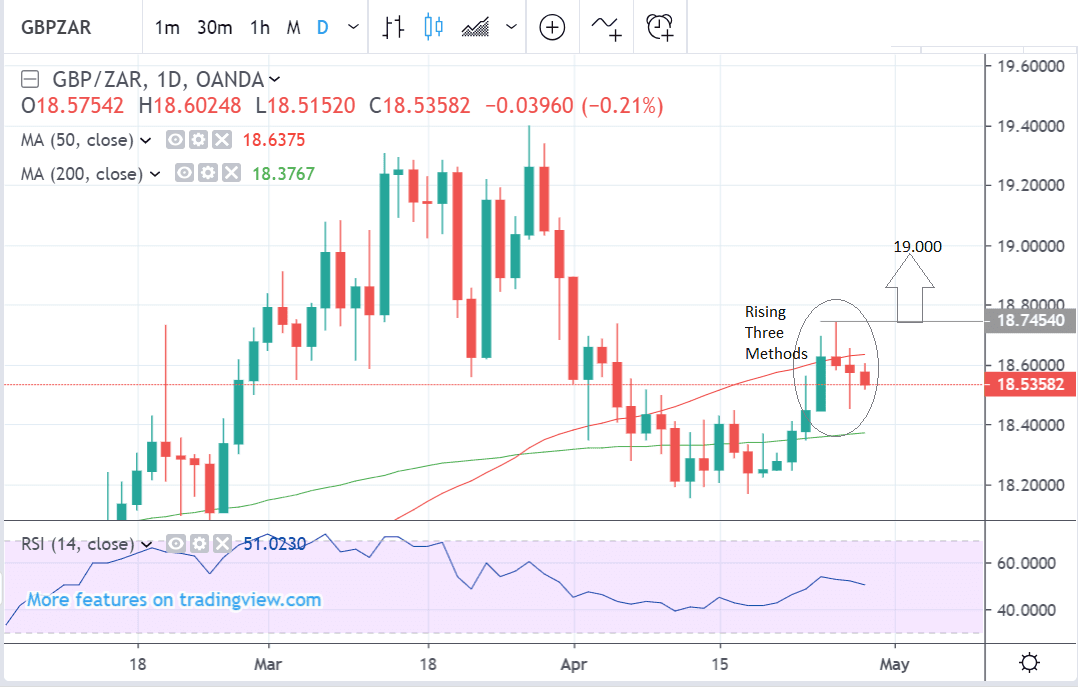

The pair’s steep short-term downtrend during March appears to have stalled and reversed. The strong rebound witnessed since the mid-April lows has probably flipped the short-term trend into positive territory.

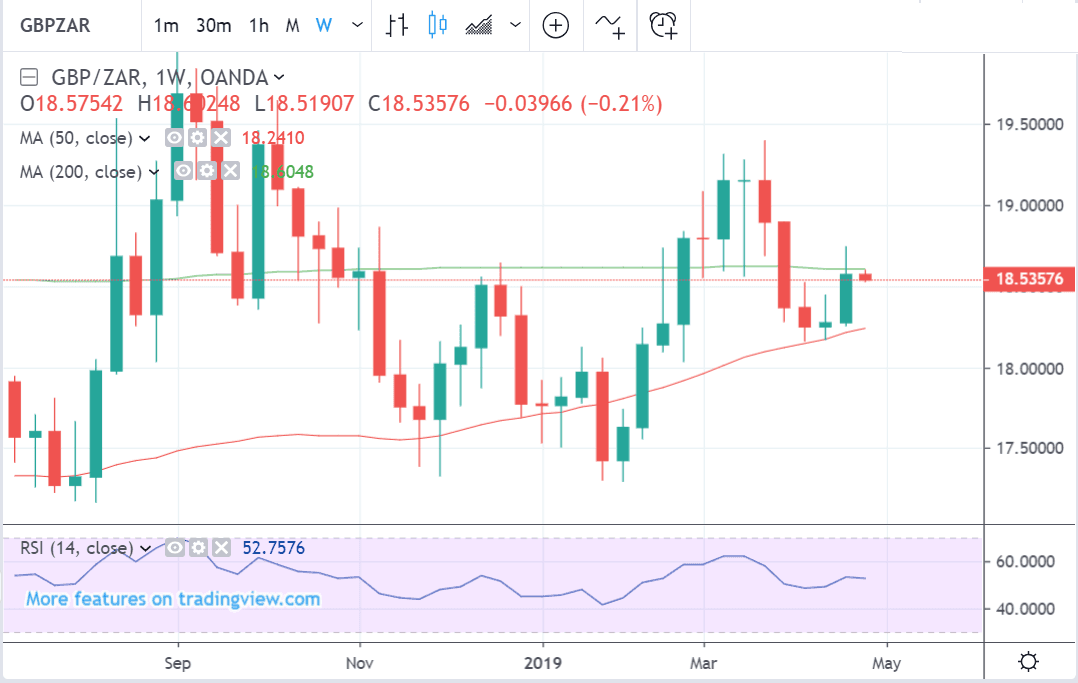

The new uptrend is fragile, though, as the weekly chart below shows, and there is no definite overall medium-term trend bias, as the pair remains trapped between two major moving averages (MA) - the 50 and 200-week MAs.

On its first attempt to break through the pair was rejected by resistance from the 200-week MA and the 50-day which are both situated in the 18.60s.

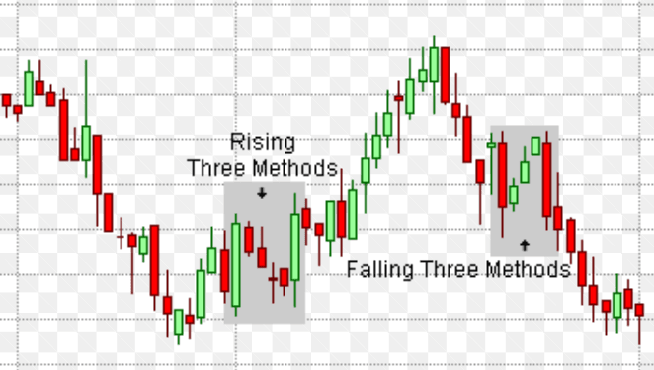

It has spent the last three days pulling back. The pull-back is not particularly steep and could be classed as a rising three-methods bullish Japanese candlestick formation, an example of which, courtesy of www.chartformations.com is shown below is shown below.

According to www.feedroll.com the success rate for this type of candlestick pattern indicating a continuation of the uptrend is 74%.

The tough ceiling of resistance from the two large MAs in the 18.60s means even with the rising 3-methods there is a chance the uptrend could fail, so we would ideally wish to see a clear break above the April 25 highs at 18.74 for confirmation of more upside.

Assuming such a break, however, the uptrend will probably continue up to the next target at 19.00.

Time to move your money? Get 3-5% more currency than your bank would offer by using the services of foreign exchange specialists at RationalFX. A specialist broker can deliver you an exchange rate closer to the real market rate, thereby saving you substantial quantities of currency. Find out more here.

* Advertisement

The South African Rand: What to Watch Over Coming Days

The Rand is mostly driven by global sentiment and the strength of the U.S. Dollar, to which it is negatively correlated.

The U.S. Dollar rose last week amidst a brightening economic outlook and anticipation of stronger Q1 GDP figures; this weighed on Emerging Market currencies such as the Rand.

A further headwind against ZAR strength were rising oil prices which gained ground because of the withdrawal of waivers from Iran sanctions for certain countries.

In the week ahead, there is a risk of USD-related volatility due to the FOMC meeting on Wednesday. Especially if the Fed changes take and decides to shift to a tighter stance. There is a risk of this because data out of the U.S. recently has been better-than-expected and Fed Chair Powell has always said policy would take its cue from data.

Key amongst South Africa’s domestic data releases is the National Treasury’s March main budget data, scheduled for release on Tuesday at 14:00. This could be more important than usual given March is the final month of the fiscal year and should thus give a clearer picture of the main budget deficit for 2018/19. Clearly the bailouts for national utility Eskom could figure in the final calculation.

The release could impact on the Rand via expectations for the country’s credit rating and whether it can stay above junk status. If it cannot it would be disastrous for the Rand as a downgrade would see substantial outflows of foreign credit.

Tuesday at 7.00 sees the release of private sector credit extension (PSCE). We expect PSCE growth to have moderated to around 5.8% y/y in March from 6.0% y/y in February. Consensus is pencilling in 6.1% y/y growth. PSCE is significant because of the big contribution it makes on GDP. Although business credit has slowed over the last decade, this has been partially offset by higher consumer credit creation.

“Our focus remains on the momentum in household credit growth given its acceleration since late 2018 and the support that this provided to consumer spending,” says Thanda Sithole, economist at Standard Bank.

The trade balance is likely to show a modest fall to 2.0bn Rand in March, from a 4.0bn surplus in February, when it is released at 13.00 on Tuesday.

On Thursday at 10.00, manufacturing PMI survey data is out. The survey showed a 45 result in March which is still indicative of a contraction in business conditions.

“This is in line with poor manufacturing activity in 1Q. The sector most likely contributed negatively to 1Q GDP growth,” says Standard Bank’s Sithole.

NAAMSA vehicle sales numbers will also be published on Thursday at 13.00. Vehicle sales growth has been in contraction for five months running. In the Q1 of 2019, vehicle sales growth contracted 5.8% from a year ago following a 1.5% contraction in Q4 of 2018.

The Pound: What to Watch This Week

The main event for the Pound is the Bank of England (BOE) rate meeting which will end with an announcement on Thursday at 12.00 BST.

The BOE is not expected to raise interest rates at the meeting despite robust economic data. Actual growth remains subdued at 1.2% (the weakest since 2009) due to business uncertainty going "through the roof" because of Brexit, so it is unlikely the Bank will want to change rates until after more clarity emerges.

Despite talk of a ‘grab and go’ rate hike in August, Reuters polls forecast rates will not move until early 2020, a calendar quarter later than was forecast a month ago.

The hunt for a new governor to replace Carney in October adds more uncertainty to the mix.

The BOE will publish its quarterly inflation report at the May meeting which includes the latest economic projections, and this is likely to garner more attention than usual - and possibly produce more volatility.

The pound is unlikely to see a big reaction to the BOE decision but any dovish tilt by the Bank - dovish meaning in favour of lower interest rates - could weigh on Sterling, which slipped to 10-week lows versus the US dollar this week.

Lower interest rates or the threat of them can be negative for a currency because they detract from foreign investment inflows, which tend to favour jurisdictions which can offer higher interest returns.

Local Elections

Thursday could see the ruling Conservative Party lose up to 1000 council seats amidst wide-spread voter unhappiness over the government's inability to deliver Brexit.

Council elections are not typically of interest to currency markets, however because the position of Prime Minister Theresa May is so precarious at this point, the outcome of the polls will be closely watched with a heavy defeat raising questions as to how much longer she can hold onto her position.

"Local elections on Thursday will be the latest barometer of the damage to Conservative support being done by the Brexit shambles. Comparisons with the last elections in the same seats (2015) are complicated by boundary changes, but this was a high watermark for the Tory support compared to their current poll ratings and significant losses are likely," says Adam Cole, a foreign exchange analyst with RBC Capital Markets.

"The immediate implications for GBP will depend May’s prospects for surviving as PM, with imminent change (Johnson is runaway favourite to replace her) lifting political uncertainty further," says Cole.

PMI Data

The other major release in the coming week are the release of PMIs for April. These may be closely watched as they recently declined in contraction territory which is defined as a reading below 50. They are seen as a forward indicator for the economy so this raised concerns softer official economic data is coming.

Although official UK data has not yet followed in their footsteps, another gloomy set of PMIs could increase the risk it will.

The Manufacturing PMI is out on Wednesday at 09:30 B.S.T.

In March the PMI rose because of stockpiling by companies preparing for a potentially distruptive Brexit, rather than due to genuine growth. The number expected by markets is 53.2, down from the previous month's 55.1.

Construction PMI fell to 49.7 in March and is forecast to rebound to 50.4 in April when data is released at 9.30 on Thursday.

UK services PMI is the big number to watch as this is a sector that accounts for over 80% of UK economic activity.

The previous month saw the Service PMI plunge below 50 and into contractionary territory in March, falling to 48.9, but data out on Friday at 9.30 is expected to show a rebound to 50.4 in April. If it disappoints the Pound could suffer.

Brexit Impasse Continues

Brexit could also still be a driver of the Pound in the week ahead. Talks between the government and the opposition Labour party have not reportedly made much progress. At the same time pressure is building on the Prime Minister, Theresa May, to resign. If she does go, the Pound will weaken.

On the other hand, the announcement of a joint deal with Labour could lead the way to a stronger Pound. Yet this seems unlikely given the UK’s adversarial political system which does not favour bi-partisanship.

There seems little incentive for Labour to help the Conservatives out of their current self-destructive, death-spin over Europe. If anything there is probably more chance of greater uncertainty in the short-term, not less, as Corbyn is more likely to bide his time and watch the Conservatives be their worst enemy than help Theresa May out of her current deadlock.

* Advertisement