Image © Adobe Images

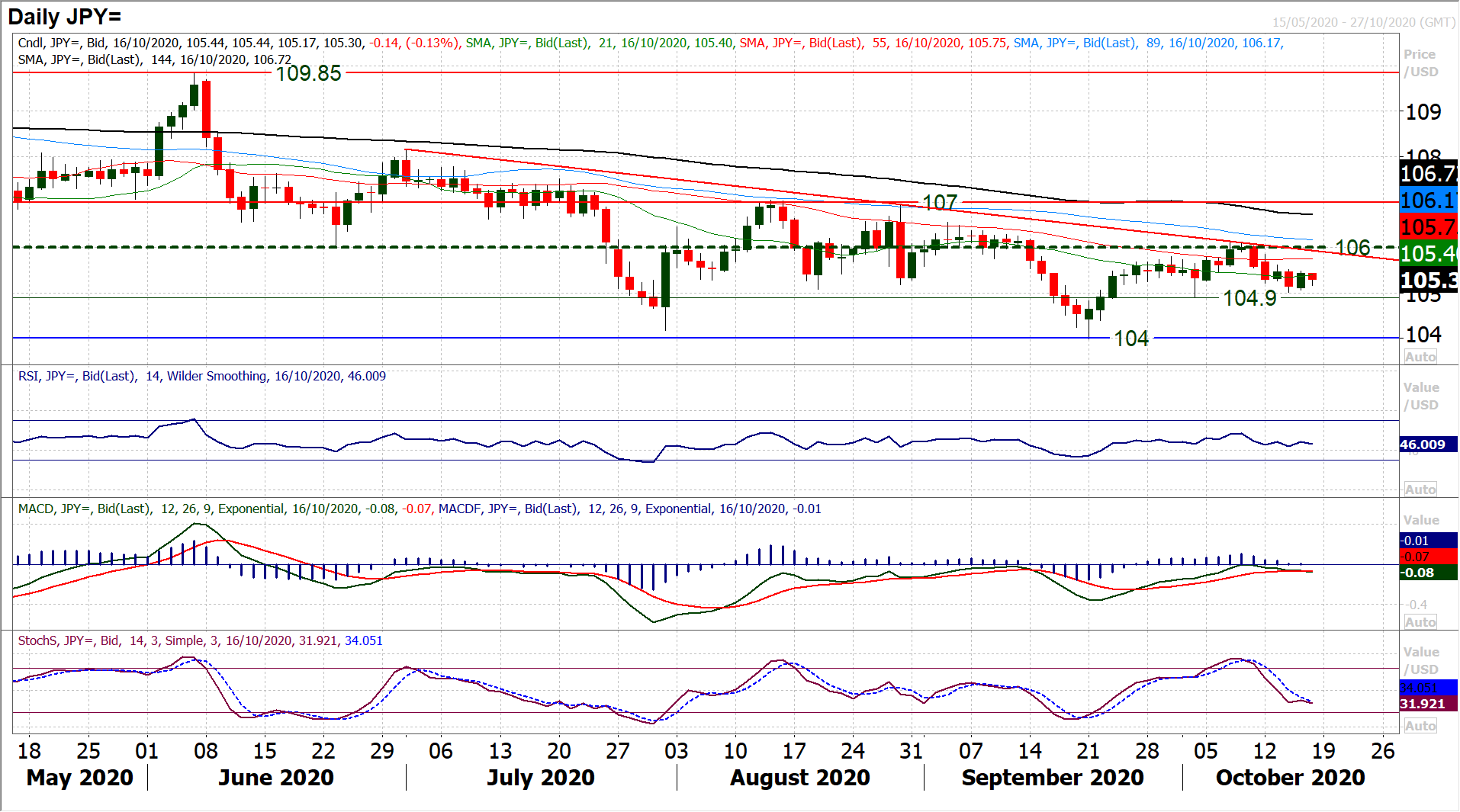

The Dollar-Yen exchange rate failed to breach above 106 and has since retreated lower to current levels around 105.25. Analyst Richard Perry of Hantec Markets says technical signals point to downside pressure targeting the 104.90 October low.

In these times of uncertainty and a lack of conviction on risk appetite, it should come as little surprise that Dollar/Yen has had a mixed few sessions.

However, with the failure around 106.00 and the re-engaging of what is approaching a four month downtrend, we continue to see a negative bias to the medium term outlook.

It suggests that near term rallies will continue to fade. The rally in June fades around 108.00, in August around 107.00 and now in October around 106.00.

It points towards ongoing downside pressure on the 104.90 October low and then below towards 104.00.

The medium erm downtrend is at 105.95 today. We see on the hourly chart there is a slight breach of a near term downtrend, but the resistance around 105.60 is still intact.

We view these little intraday bounces as a chance to sell.

The risk negative bias that has ushered flow back towards safe haven assets in recent sessions is still present as we come towards the end of another frustrating week for major markets.

There is a distinct lack of trend or conviction right now through forex and commodities.

It is difficult for traders to take a view amid the frustrating lack of progress in US fiscal support negotiations and deadlock over a UK/EU trade deal.

In Washington, the sense is that fiscal support is becoming (if it is not already) a political football kicked around as who can use it for their advantage moving into the Presidential election.

Agreement is ever more unlikely and this is weighing on broad market sentiment. (For a more detailed look at the Dollar and the election, Pound Sterling Live's latest report on the matter is now ready for download).

The EU/UK negotiations are also extremely knife edge, with game theory playing out in a classic sense. They are close enough to continue talking, but the lack of real traction makes it likely that this will drag on for some weeks yet.

So with the impact on major markets, we see a drift towards safety, with the dollar and yen benefitting at the expense of higher risk commodity currencies such as Aussie and Kiwi.

In the US a rebound in Treasury yields helped equities rally into the close, but this traction looks to be waning again today. As yields tick back lower again, it is setting up for another frustrating day for the bulls.

It is a US focused day on the economic calendar to end the week. However, first up is the final Eurozone inflation reading for September at 1000BST. Headline Eurozone HICP is expected to be confirmed at -0.3% (-0.3% flash September, down from -0.2% final August).

The core Eurozone HICP is expected to also be confirmed at +0.2% (+0.2% flash September, +0.4% final August).

Into the US session, the main focus is US Retail Sales at 1330BST which is expected to show core ex-autos sales gaining by +0.5% in the month of September (after growth of +0.7% in August). US Industrial Production is at 1415BST and is expected to improve by +0.5% on the month in September (after +0.4% in August).

Capacity Utilization is expected to also improve to 71.9% (from 71.4% in August). The preliminary look at October’s Michigan Sentiment is at 1500BST and is expected to tick slightly higher to 80.5 (from 80.4 in September).