Image © Adobe Stock

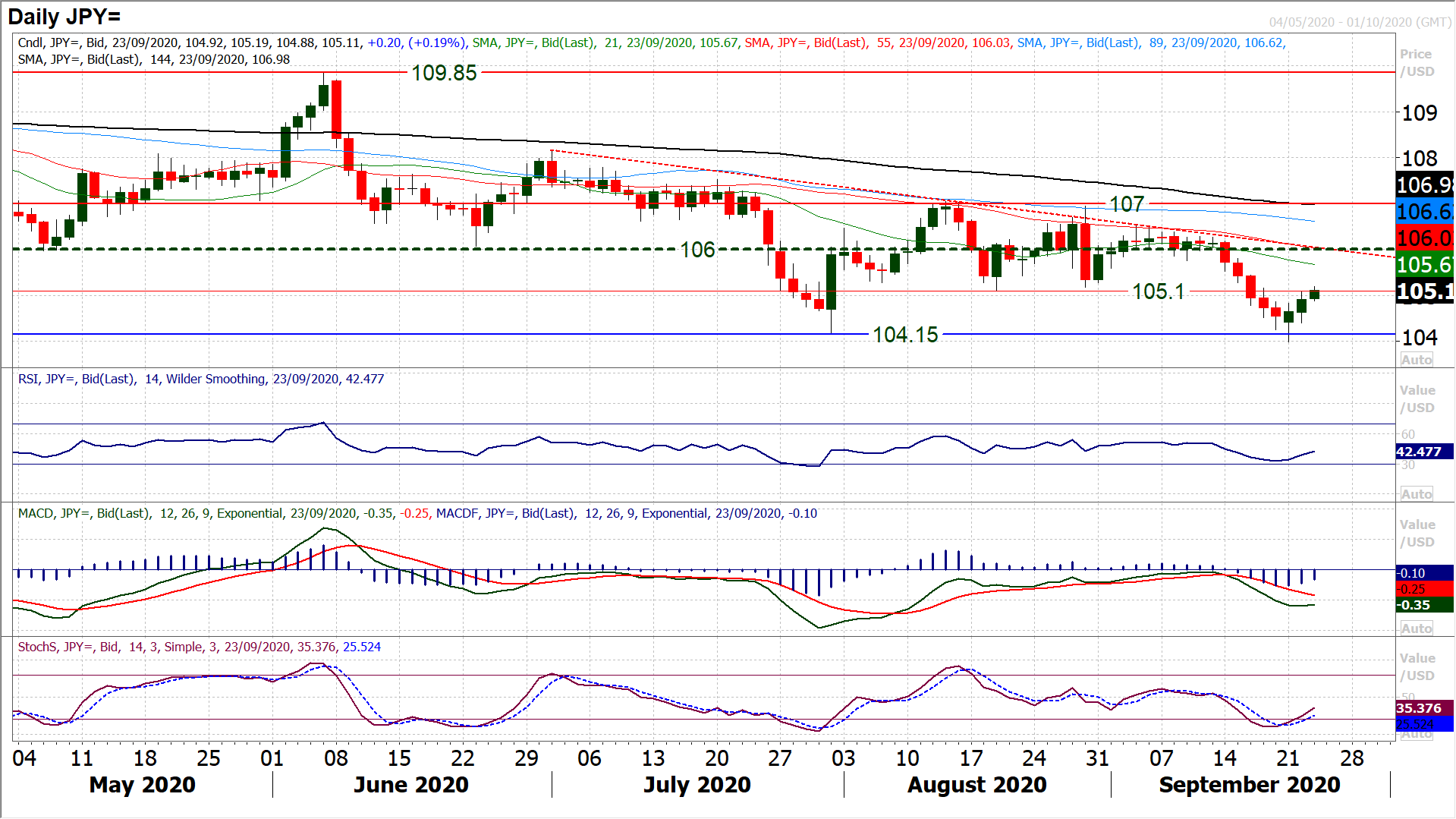

The Dollar-Yen exchange rate is seen at 104.96 in mid-week trade having rallied for two days in succession, a development that leads analyst Richard Perry of Hantec Markets to turn more constructive on the USD/JPY outlook.

Another remarkable session of swinging sentiment on the dollar saw the eventual formation of a second decisive positive candle for Dollar/Yen.

For a second consecutive session, an initial move lower was used as another chance to buy and this marks a significant shift in sentiment as the recovery begins to really develop now.

The hourly chart shows the decisive move above 104.85 resistance to complete a small base pattern and imply +85 pips of additional recovery.

This may not sound like much but there has been a significant shift in the outlook over the past couple of sessions where a recovery is now building strongly.

Momentum indicators are reacting strongly too, with a bull cross now on Stochastics, whilst RSI has also turned higher.

Early gains today add to this move. There is upside potential in this near term bounce, but the daily chart shows the need to pull through the initial overhead supply 105.10/105.30 from all the old August lows.

This is being tested this morning. Above 15.30 brings the market up towards the old 106 pivot area again. The hourly chart shows 104.85 is growing as neckline support above 104.40 as a higher low.

A recovery on the US dollar is gathering momentum.

With traders increasingly concerned about second wave COVID infection rates rising across Europe and trends also turning higher for the US, there is a shift into the dollar.

Throughout the summer months the perception was that the US was in for economic underperformance.

However, this perception is now being re-set as France, Spain and increasingly the UK are struggling with rising infection rates which are forcing the reinstatement of social containment measures.

Congress may have been able to pass a stopgap funding bill to keep government open, but a fiscal support package remains some way off.

Fed chair Powell may have towed the dovish line, but there has also been surprisingly hawkish comments from the FOMC’s Charles Evans over limiting QE and raising rates sooner than expected.

The dollar has seen the benefit of all this, driving higher through 94.00 resistance on Dollar Index.

This equates to two month lows on EUR/USD whilst gold has also broken decisively below $1900.

The Reserve Bank of New Zealand maintained a fairly steady ship on monetary policy (rates at +0.25%, asset purchases steady at NZD 100bn) and kept the door open to negative rates.

This has not helped the Kiwi too much though this morning.

The Agenda

The economic calendar is awash with flash PMIs for September today. Eurozone data is at 0900BST and is expected to show Eurozone flash Manufacturing PMI improving to 51.9 (from 51.7 final August) and Eurozone flash Services PMI to remain at 50.5 (50.5 final August).

This would see the Eurozone flash Composite PMI slipping slightly to 51.7 (from a final 51.9 in August). The UK flash Manufacturing PMI is at 0930BST and is expected to drop back to 54.1 (from 55.2 final August) whilst UK flash Services PMI is expected to fall to 56.0 (from 58.8 final August).

This would leave the UK flash Composite PMI at 56.3 (down from 59.1 in August).

The US flash Manufacturing PMI is at 1445BST and is expected to remain at 53.1 (53.1 final August) with the US flash Services PMI to slip slightly to 54.7 (from a final 55.0 in August).

Aside from that, the EIA Crude Oil Inventories are at 1530BST and are expected to show an inventory drawdown of -2.3m barrels (after a drawdown of -4.4m barrels last week).

Once more there will be focus on Fed chair Jerome Powell who testifies before the House Select Committee at 1530BST about impact of COVID-19.

Again, any clarity on Fed monetary policy could drive volatility. There are two other Fed speakers today too, with Loretta Mester (tends to lean hawkish) at 1400BST and Randall Quarles (centrist) at 1900BST.