- USD could rise on the back of US funding its growing budget deficit

- A preference for raising longer-term debt would support USD, says strategist

- Deficit to grow 804bn this year, says Congressional Budget Office statement

© jcomp, Adobe Stock

The US Dollar is likely to gain support if the American government continues its preference for taking out longer-term loans.

Signs that the US Treasury will fund its growing budget deficit with long-term rather than short-term loans is likely to be "Dollar positive" according to a Nizam Idris, head of fixed income and currency at Macquarie group.

The insight comes on the back of data showing that the US Treasury has ramped up its longer-term borrowing - that is in 3, 10 and 30 year bonds - in the first week of April, with 64bn in this category sold, compared to March and the long-term average, but at the same time has reduced its issuance of under 1-12 month bills compared to last month.

Idris says this is a sign the Treasury is probably "tapping the longer end of the yield curve" for the extra money it needs to finance it's ballooning costs, which have risen significantly since the recent tax cuts and increased spending promises, and that the effect is likely to be that it will "steepen the curve and be positive for the Dollar."

Using longer-term loans will mean increased inflows of Dollars since a large proportion of Treasury borrowing comes from outside the US.

The fact that it is longer-dated means essentially the money need not be paid back for several years thus creating a short-term demand spike for the currency.

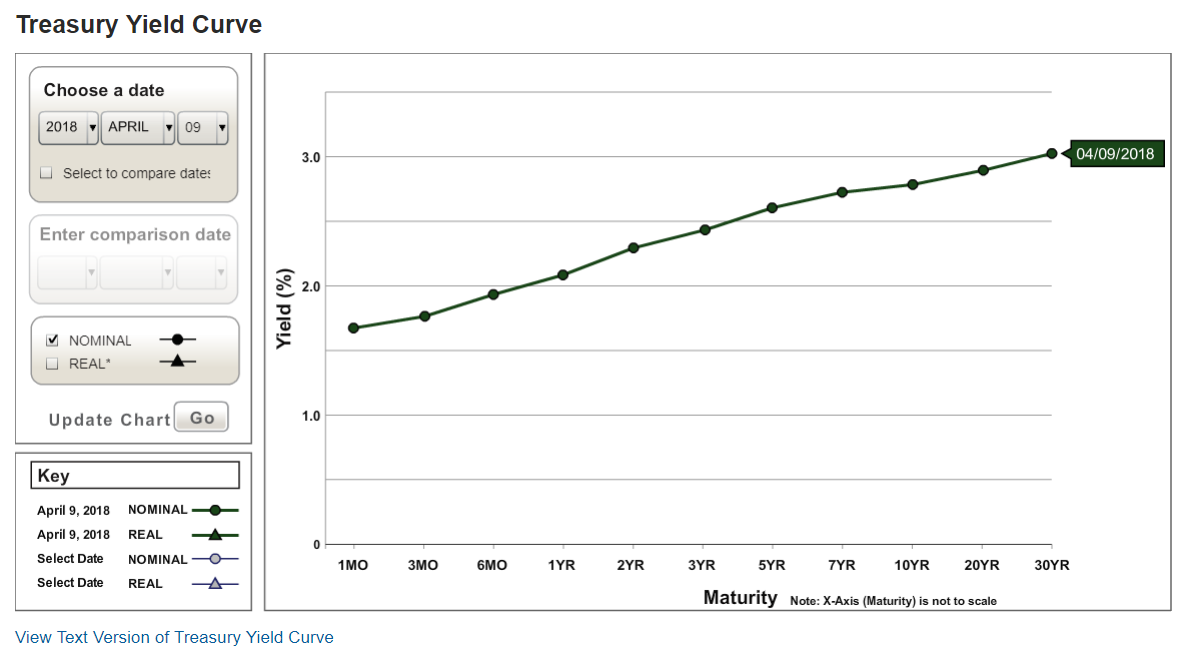

The benchmark US 10-year treasury yield, the amount bondholders are compensated for inflation erosion, was up by 0.8% to 2.808% on Tuesday morning at the time of writing.

The 10-year yield and yields for other maturities is shown in a chart of the yield curve below:

The outlook for the Fed and the way it positions itself ahead of the June policy meeting could also be significant both for bonds and the Dollar.

"If the view is that the FOMC is hiking too slowly then the yield curve could steepen, but if it errs on the side of caution and is seen to be hiking too rapidly in curbing inflation, then the curve could invert," says Nizam.

This suggests the Dollar may respond in an anomalous, 'inverted', way to Fed policy expectations, rising even if the Fed takes a more relaxed approach to increasing interest rates since this would be more likely to generate the steeper curve which is more positive for the currency.

The Macquarie strategist says that Wednesday's CPI figures and their impact on the Federal Reserve are also likely to be instructive. Current expectations are for a 2.1% rise in core inflation which would take it above the Fed's 2.0% target for the first times since the financial crisis and suggest four rather than three interest rate hikes might be expected in 2018.

If this led to a more aggressive response from the Fed and a flatter yield curve, as Nazim suggests, however, the impact on the Dollar might be more difficult to predict.

As far as concerns the US may be about to enter a recession because of inverting curve, the strategists think these are overstated as the increased spending and tax cuts from the government are likely to stimulate the economy in the short-term.

Deficit Projected to Rise Says Congressional Budget Office (CBO)

The Macquarie strategist's comments came on the eve of the release of the CBO's deficit projections - now published - which expect the US budget deficit to rise to 804bn in 2018 from 665bn in 2017.

"Federal debt is projected to be on a steadily rising trajectory throughout the coming decade." said the CBO.

The main reason for the rise was reduced revenue from tax cuts and increased government spending.

"The deficit that CBO now estimates for 2018 is $242 billion larger than the one that it projected for that year in June 2017. Accounting for most of that difference is a $194 billion reduction in projected revenues, mainly because the 2017 tax act is expected to reduce collections of individual and corporate income taxes," says the CBO.

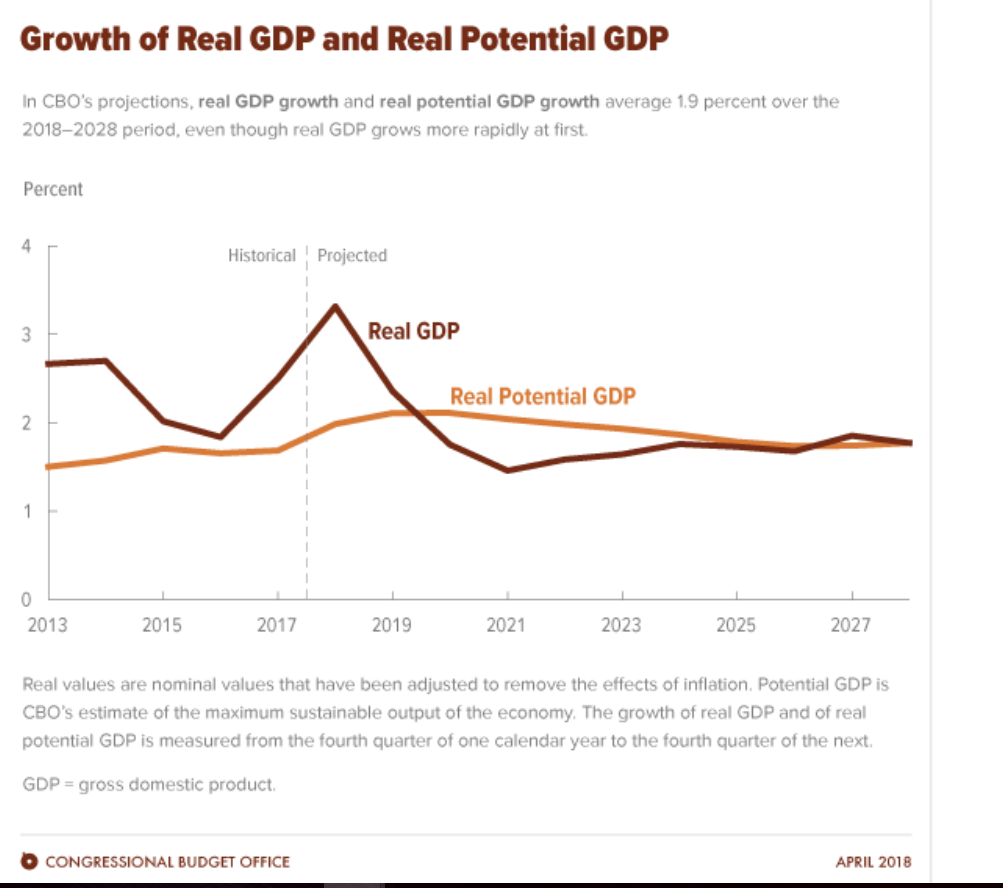

In the short-term economic growth is expected to remain high, rising to a peak growth rate of 3.3% in 2018 but then sliding to 2.9% in 2019 and remaining subdued thereafter.

The chart above shows real and potential GDP. The first is the actual growth of the economy whilst 'potential GDP' is the amount of slack left before the economy is running at full capacity - or its growth potential in other words.

"Between 2018 and 2028, actual and potential real output alike are projected to expand at an average annual rate of 1.9 percent. In CBO’s forecast, the growth of potential GDP is the key determinant of the growth of actual GDP through 2028, because actual output is very near its potential level now and is projected to be near its potential level at the end of the period," says the CBO.

Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here.