The Pound-to-Dollar rate will make further gains in 2018, supported by a backdrop of easing Brexit risks and stunted US inflation, or so go the forecasts of a broad range of analysts.

Almost all of those analysts predict the Dollar will either weaken again or flatline which, when combined with a stronger Pound, will help lift the GBP/USD exchange rate.

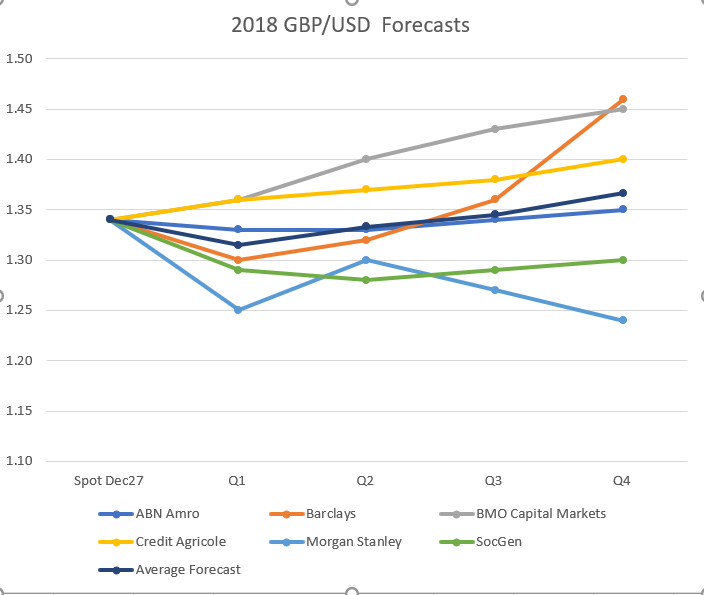

The average of all forecasts obtained by Pound Sterling Live stands at 1.37 for the end of 2018 - higher than the current market rate of 1.34.

Above: Pound Sterling Live compilation of forecasts.

Analysts and strategists at Barclays, BMO Capital Markets, ING and Societe Generale all have an outright negative view of the US Dollar’s prospects in 2018. ABN Amro, UBS, and Credit Agricole are all neutral.

Frequently found among the reasons for the lacklustre outlook is the 'Rest of World' growth performance, which will reduce the relative attractiveness of the US Dollar and associated assets in 2018.

Better growth in the rest of world will draw funds out of Dollars and into myriad other currencies as the world catches up with the US post-crisis recovery and investors scramble to get a piece of the action.

Another major theme to play a part in Dollar weakness is subdued inflation in the US. It may seem counterintuitive but in today's world traders are waiting for inflation, which erodes the value of a currency, because higher inflation will also lead to higher interest rates.

Higher interest rates attract capital from speculators and foreign investors, both of which lift the currency concerned, thus in a roundabout way higher inflation strengthens currencies.

In the US, inflation has remained subdued below the Federal Reserve’s target, despite a broad strengthening of the economy, and analysts are betting this trend will extend into 2018.

The view is neatly summed up by Georgette Boele, a strategist at Credit Agricole, who wrote in a recent note that subdued inflation is "preventing a sustained medium-term uptrend in the Dollar.”

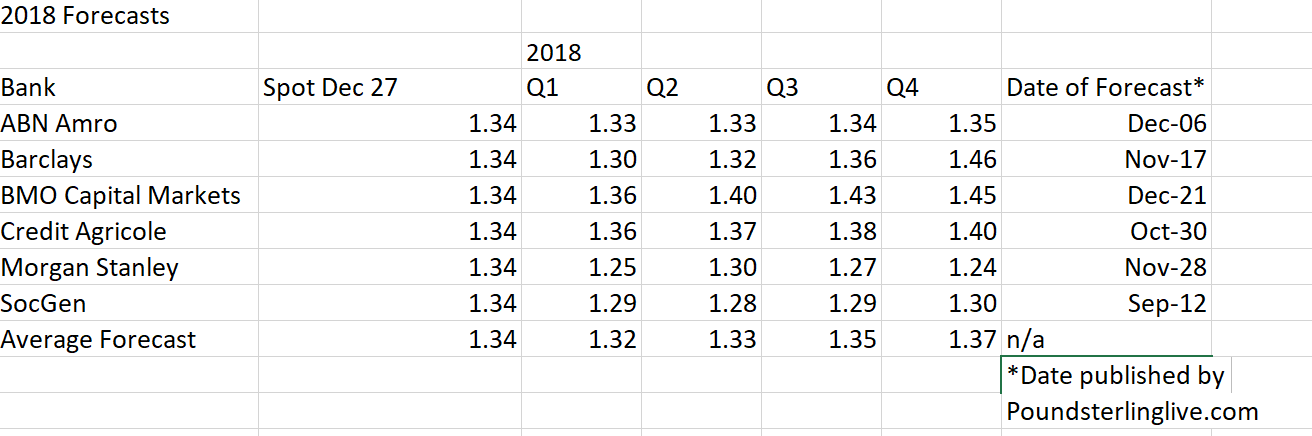

Above: Pound Sterling Live compilation of forecasts

Sterling To Exit the Ashes

The Pound overall is seen as having the potential to rise in 2018. Most analysts have flagged how undervalued it is compared to their valuation models, metrics, and historical averages.

Kit Juckes, Societe Generale’s chief foreign exchange strategist, says Sterling will spend 2018 "bumping along the bottom," unable to rise because of poor economic data but already so undervalued it "cannot get any cheaper than it already is."

Credit Agricole says downside is "limited" due to the already heavy weight of a Brexit premium, which has had as damaging an effect on the exchange rate as it could even in the worst case scenario of a move to a World Trade Organization trading relationship with the EU.

Consensus - and this is among those who are normally more pessimistic on the Pound - seems to be that the only way is up for Sterling in 2018.

The more optimistic bunch have also gone as far as to suggest Brexit risks will probably ease in 2018, saying politicians will want to avoid a “cliff-edge” Brexit that they say might have potentially catastrophic economic consequences.

As a result, concessions in order to achieve an exit deal are more likely than not, even if at the eleventh hour.

UBS stands out as the only major bank with a negative view of Sterling in 2018, with its analysis forecasting that a "decelerating economy compounds uncertainty around Brexit" in the year ahead.

The Importance of 'Return'

The return an investor gets above the rate of inflation is a major consideration in currency valuations, according to one school of thought and it features heavily in the forecasts by Morgan Stanley and ABN Amro.

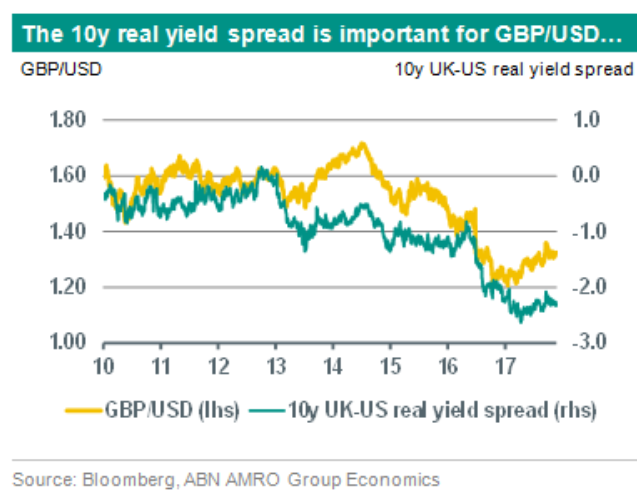

The return above inflation is called the "real yield" in bond market parlance and there is often a very tight correlation between the 'real yield' return and currency returns.

The graph below provided by ABN Amro shows how tight the relationship is:

US real yields are forecast to remain either neutral (ABN Amro) or "limited" in the case of Morgan Stanley, because these banks forecast that US inflation will actually rise next year and that this will erode the additional return over inflation offered by US bonds.

In contrast, UK real yields are expected to rise as UK inflation falls as the referendum fall in the Pound falls out of the prior year comparison period and due to the delayed impact of a stronger Pound against the Dollar in 2017. Sterling has risen by 8.5% versus the greenback this year, although it is still 9.4% below its pre-referendum level.

Next year’s flow of funds is likely to favour the Pound, therefore, leading to a rise in GBP/USD.

Get up to 5% more foreign exchange by using a specialist provider by getting closer to the real market rate and avoid the gaping spreads charged by your bank for international payments. Learn more here.