Order flow data is an accurate indicator of fx returns for most G10 currencies and suggests upside for the Dollar in September.

Recent economic data may have been uninspiring, and hopes for Thursday’s inflation data subdued, but some strategists say don’t discount a Dollar recovery just yet.

Market expectations of another hike from the Fed in 2017 have almost dissipated and a strong rise in August inflation might not be enough to change this but some are still betting on another rate hike, while others see the Dollar going higher in the near term regardless of what the Fed does.

Bullish statements on the greenback come toward the tail end of a six month period where the Dollar index has fallen by more than 10% and the US currency has suffered high single digit losses, double-digits in some cases, against many of its G10 counterparts.

US Dollar Index shown at weekly intervals. Source: Netdania.

The Greenback Is Down But Not Out

Recent weakness of inflation and uncertainty over the 2018 composition of the Federal Open Market Committee are among the foremost reasons why the Dollar index has sold off so sharply.

But faster growth in the second quarter and a further improvement in the labour market has left market pricing of the US Dollar appearing too pessimistic, according to one strategist, and could result in the greenback seeing a bounce over the short term.

“We expect the Fed to leave the key rate unchanged at its September 19-20 policy meeting” says Carl Hammer, chief fx strategist at SEB. “but believe that the central bank will hike this rate in December 2017. In 2018 we expect three more hikes.”

Hammer has forecast the Fed will formally announce the beginning of its balance sheet reduction at the September meeting, which will see the US central bank unveil details of its plan to shift its quantitative easing assets back onto the market.

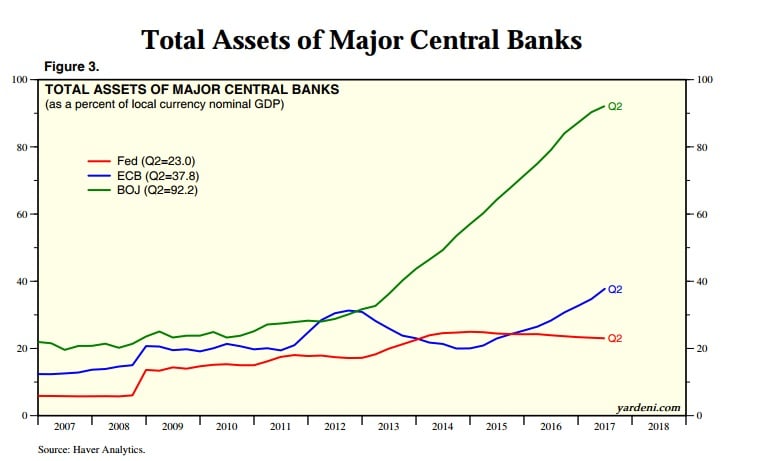

The Federal Reserve balance sheet swelled from around $800 billion in 2008 to $4.6 trillion in 2015, when it concluded the tapering of quantitative easing. Fed QE assets are equivalent to more than 20% of US GDP.

Graph showing balance sheet assets of three major central banks. Source: Yardeni Research Inc.

Order Flow Points to Upside For The Dollar

Net interbank order flows are a significant driver of currency prices, according to strategists at Bank of America Merrill Lynch, which are responsible for as much as half the monthly returns in foreign exchange markets since 2006.

“Looking at the partial data for September (1-8 September), there is broad evidence of USD demand that has yet to translate to meaningful currency gains,” says Vadim Iaralov, a strategist at BAML.

Measuring changes in net supply and demand works as an indicator of returns for 19 out of the 23 G10 and emerging market currencies analysed by BAML. A one standard deviation change in net demand for a particular currency over another can correspond to a 1-2% gain in the fx rate.

“Our analysis suggests spot playing catch up for GBP/USD, EUR/USD, for USD/CAD and for USD/RUB by the end of September when we compare the expected return vs actual return (1-8 September),” Iaralov wrote in a Wednesday note.

The Pound-to-Dollar rate could fall as much as 2.2% before the end of September, according to BAML’s analysis, while the Euro-to-Dollar rate is vulnerable to a 1.5% pullback. There is as much as 2.4% upside in the USD/CAD exchange rate, according to the BAML model.

But Beware, The Fed Et Al

Headline consumer prices and core consumer prices, which exclude volatile food and energy costs from the comparison, are seen rising for the month of August when the official data are released at 13:30 pm London time Thursday.

Consensus suggests the inflation barometers rose by 0.3% and 0.2% respectively but any disappointment could see expectations of a Fed standstill solidify and would likely mean renewed selling of the greenback.

This is while, looking further out, a great unwinding or paring back of the US Dollar reserves built up by foreign central banks threatens to provide a source of downward pressure on the greenback over the broader term.

The appreciation of the dollar since mid-2014 and an uncertain outlook for the euro area boosted the dollar’s proportion of global central bank reserves substantially," says Hammer. "Going forward, rebalancing of reserve holdings could become a USD-negative factor, since reserve managers are probably unwilling to raise the USD proportion further from current levels."