HSBC have cut their forecasts for the US Dollar based on their latest analysis of Donald Trump's economic policies and his administration's effectiveness in achieving them.

Above: David Bloom, HSBC's Head of Global FX Strategy.

Just days before a much-anticipated announcement on intended tax reforms by the United States Government, a leading foreign exchange analyst has come out and said the Dollar's cyclical rally is due to end.

Markets are anticipating a pro-USD outcome from US President Donald Trump when he announces tax reforms on Wednesday, April 25. Dollar bulls need a significant announcement if the USD is to kick-start its ascent.

The US Dollar has risen strongly since Donald Trump’s presidential inauguration, rallying to its peak against a basket of currencies by an estimated 6%.

A host of Dollar-positive election promises helped fuel the rise, including tax cuts, infrastructure spending, border tariffs and the repatriation of billions in offshore corporate earnings.

Trump’s inability to get his policies through Congress, however, has depressed that initial euphoria.

His failure to get Congress to repeal the Affordable Care act was a major blow as the savings it would have delivered were going to be used to pay for tax cuts.

It also triggered a wave of scepticism at his ability to get his policies implemented.

This may have marked the start of a new phase of weakness for the Dollar according to HSBC’s Global Head of FX Strategy, David Bloom who appears unconvinced that Trump will be able to announce fresh policies with the clout to stimulate the Dollar's rally.

Financial Problems

Trump’s consideration of thrift is no coincidence – the US finances are in a perilous state.

The country is running a high budget deficit and even higher trade deficit - in every way it spends more than it makes.

This was highlighted recently by the reminder that the federal borrowing limit had almost been reached, and whilst emergency measures will keep wheels turning until the end of the year, the Government will then either need to raise the ceiling even higher or make dramatic savings.

Does the prospect of massive infrastructure spending and ‘phenomenal’ tax reforms seem credible or likely in such a milieu?

For many traders, the answer is now a no.

Tax Cuts are Hardly Ever Self-Financing

Nevertheless, Donald Trump’s economic advisers, maintain a line of thinking that Trump’s tax reforms will generate more revenue than they cost and so become self-financing.

They draw inspiration from supply-side economist Gerald Laffer, who said Trump’s policies would lead to economic ‘Nirvana’.

The idea is that the tax cuts stimulate so much growth that the economy pays for them itself.

"We, and Congress, will most likely see this as wishful thinking. If it were that easy, everyone would do it. Though some positive effect on short-term growth is possible from tax cuts, this is likely to be inadequate to boost revenues to outweigh the costs," says analyst Viraj Patel at ING Bank in London.

Bloom agrees saying it seems unlikely that tax cuts will be self-financing.

The Tax Policy Center estimates that the proposed tax cuts from the new US administration would lower taxation revenues by USD6.2trn over 10 years (approximately 32% of current US GDP).

Taking into account added interest costs and macroeconomic effects, this estimate widens to USD7.0trn.

Experience from Regan’s presidency in which the same belief in tax cuts could be self-financing proves they were not in that case, and the government had to borrow massively to finance those tax cuts in the end creating a massive burden of debt for future generations to bear.

Deficit and the Dollar

Concerns about the deficit, tax cuts and borrowing are part of the structural complex which will bring the Dollar down argues Bloom.

The analyst argues deepening concerns about the budget deficit and government debt will come to weigh on the currency:

“While the market is still waiting in anticipation of fiscal changes, we believe aggressive tax cuts if implemented could lead to an eventual USD switch from cyclically positive to structurally negative.

“Here, government debt, budget deficits and trade imbalances become the focus. So, at first, the fiscal boost is seen as USD positive on a cyclical basis; however, this fiscal boost could soon switch to structural worries about bigger deficits and become USD negative.”

The Desire for a Weaker Dollar Does Not Gel with Policy Agenda

Trump seemed ignorant of the impact of his policies on the Dollar when he was campaigning.

But he was not the only one - mainstream analysts were characteristically myopic in their forecast that the Dollar would fall on a Trump election win too – in the end the Dollar rose, as markets considered his bevy of Dollar-positive policies.

Once seated in office, however, Trump began to realise that some of his policies were rendered mutually exclusive due to their almost unanimous positive impact on the Dollar.

His protectionist trade policies and “Buy America, Hire America,” rhetoric were incompatible with a strong Dollar.

Unfortunately, his tax reform and infrastructure spend policies threatened to push up the Dollar.

Bloom thinks that overall the administration does not now want a strong Dollar and will actively try to weaken it using verbal intervention.

“The US President is clearly uncomfortable with the level of the USD. In an interview with the Wall Street Journal he said the USD is ‘too strong’ and in the past he has suggested the strong USD ‘is killing us’. For a US president to opine on the USD is a break from the practice of the last 30 years. Currency strategists were often loathe to have currency forecasts that pointed in the opposite direction to central bank policy – “don’t fight the central bank”. It may be no wiser to fight a President,” says Bloom.

The administration’s focus is less on ‘blanket’ trade and tariff policies and more on focused bilateral, individually-tailored, deals is symptomatic of the new sensitivity to the currency as a more precision approach is likely to prevent an appreciation of the Dollar.

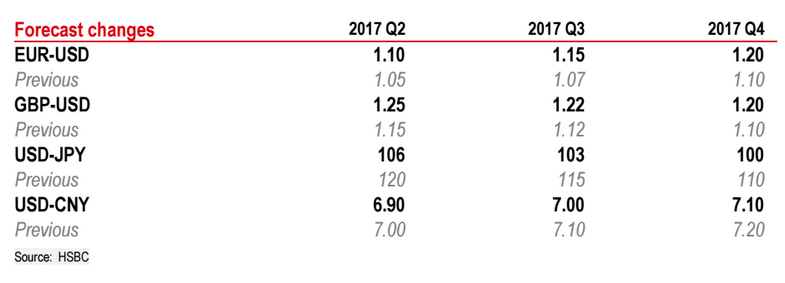

Forecasts

HSBC’s forecasts for the key Dollar pairs have now been cut notably to reflect the bank's latest analysis.

They see the Euro to Dollar exchange rate rising the most, reaching 1.20 in Q4 2017, helped by Euro strength as the European Central Bank (ECB) begins to taper its stimulus programme.

However, the news is not so good for those hoping for the Pound to turn stronger against the Dollar.

HSBC say they see the Pound to Dollar rate at 1.20 because Bloom expects the Pound to weaken more than the Dollar.

However as the table below reveals, HSBC have hiked their forecasts for the GBP/USD massively.

USD/JPY is expected to fall to 100 and the profle here is again one of a notably weaker Dollar.