Image © Adobe Images

The dollar is overvalued and faces structural headwinds pointing to long-term depreciation.

BCA Research says the long-term case for U.S. dollar weakness remains intact, arguing the currency is still materially overvalued and faces mounting structural headwinds that are unlikely to be offset by productivity outperformance alone.

The starting point is valuation: a deep-dive analysis on long-term currency valuation by BCA's Mathieu Savary finds the dollar remains rich against major peers on purchasing power parity measures, trading at a 16% premium to fair value.

Historically, BCA says overvaluation on that scale has been associated with long-run returns of around minus 3% per year.

BCA's new analysis seeks to counter the apparent random walk FX often presents and to arrive at longer-term directional anchors.

Savary explains that even after adjusting for America's relative productivity advantage - U.S. productivity has outgrown the eurozone and Japan by roughly 31% and 30% since 2000 - the greenback is still around 9.8% overvalued.

In other words, productivity differentials may slow the pace of depreciation, but do not eliminate it.

The U.S. net international investment position, and the logic of the Mundell–Fleming model, meanwhile, provide a smoking gun to downside risk.

The U.S. administration's stated goal of rebalancing the economy away from consumption and toward industrial production is seen as dollar-negative because it pushes the saving–investment balance outward, which weighs on the currency over time.

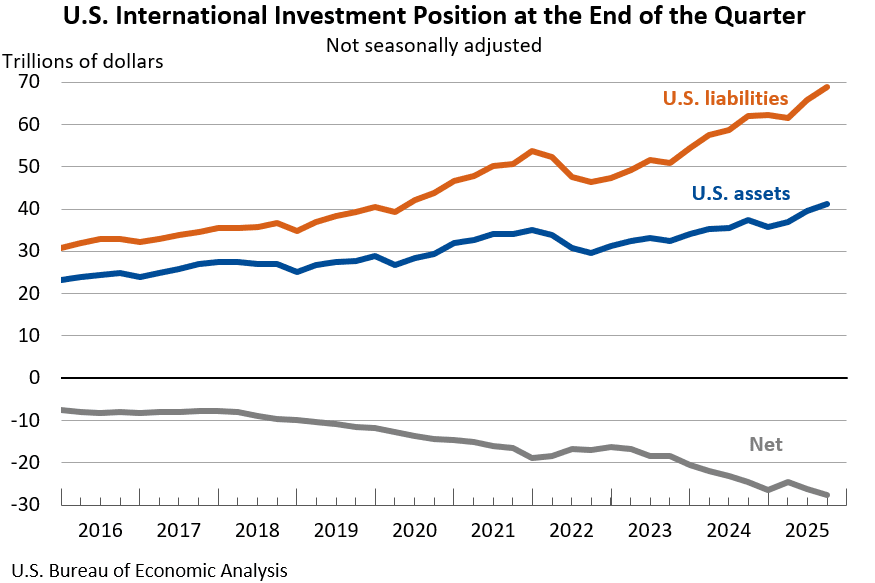

Savary also highlights the deteriorating external balance sheet.

The U.S. net international investment position is now around minus 90% of GDP, and the primary income balance has turned negative, meaning the U.S. is paying out more income to foreign holders of its assets than it receives.

GBP/USD

At the same time, the analysis cites a large fiscal deficit of 6.1% of GDP that must be funded from abroad, alongside a current account deficit of around 3% of GDP, reinforcing the need for ongoing foreign capital inflows.

Add to this the U.S. administration's increasingly acrimonious relationship with the rest of the world.

"Investors feel less secure investing in the US and will either decrease their purchases of US assets or start hedging them more. Either way, these processes will narrow the US capital-account surplus and weigh on the greenback," says Savary.