"This means that one-way traffic in FX, with the dollar staying on a downtrend for longer, still appears unlikely" - ING Group.

Image © Adobe Stock

Federal Reserve (Fed) policymakers were far from unanimous in their views on how much further interest rates may need to rise in November and recent data has done little to suggest that would have changed since this month's meeting, though analysts at ING say it's too early to count the U.S. Dollar out.

Chairman Jerome Powell was speaking for himself and "various" others on the Federal Open Market Committee (FOMC) when saying in November's press conference that earlier U.S. economic data had argued in favour of a higher peak in interest rates than was suggested in September's forecasts.

This is not quite the "many," the "most" or the "majority" of participants that would be required for a consensus in favour of aiming higher than the 4.75% level that was suggested in September as next year's likely endpoint for the Federal Funds rate in the current monetary policy cycle.

That was the most important revelation contained in Wednesday evening's release of minutes from the November meeting at which FOMC members agreed to lift U.S. interest rates by three-quarters of a percentage point for a fourth consecutive time running.

"The market latched onto the unusual description of how many participants were onboard with Powell’s press conference message," says Elsa Lignos, global head of FX strategy at RBC Capital Markets.

Above: Interest rate implied by June 2023 Federal Funds rate future slips back below 5% following Wednesday's minutes. To better time your international payments, consider setting a free FX rate alert here.

The Dollar was sold widely ahead of Wednesday's release but losses built further after only to then snowball in Europe on Thursday as financial markets rethought wagers on how much further the Fed might lift its interest rate.

"The OIS market was priced for the terminal rate reaching a little over 5.00%, close to 50bps above the September median dot terminal rate and hence the minutes failed to provide any impetus for a move higher," says Derek Halpenny, head of research, global markets and international securities at MUFG.

"That left market participants with the data that was released yesterday with the biggest focus on the much sharper than expected declines in the PMI," he adds.

Financial markets were still pricing-in a peak Fed Funds interest rate near to 5% on Thursday, however, which is above the 4.75% flagged as likely in November's Federal Open Market Committee forecasts.

Prices data released since November's meeting has suggested that U.S. inflation rates softened in October while other figures have hinted of cracks beginning to emerge in the local labour market so has done litlle, if anything at all to argue in favour of a steeper climb in interest rates.

"The November FOMC minutes noted that “a substantial majority” of FOMC participants agreed that a slower pace of hiking would “likely soon be appropriate,” writes David Mericle, chief U.S. economist at Goldman Sachs, in a review of Wednesday's minutes.

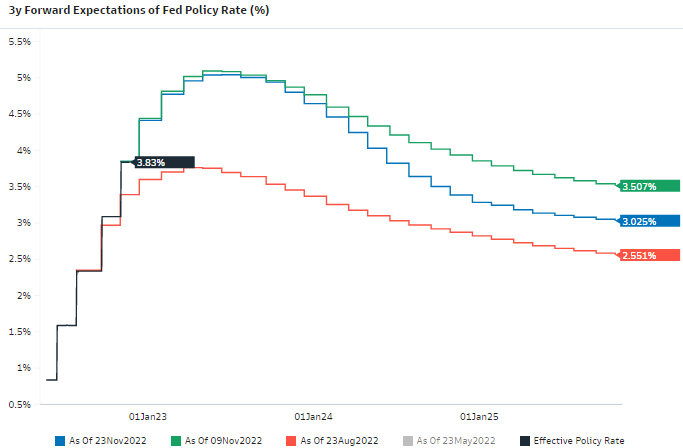

Above: Market-implied expectations for Fed Funds rate at selected dates. Source: Goldman Sachs Marquee. If you are looking to protect or improve your international payment budget you can secure today's rate for use in the future or set an order for your ideal rate whenever it becomes available. More information can be found here.

"Echoing the language in the post-meeting statement, FOMC participants argued that the level of the policy rate, the uncertain lags with which monetary policy affects activity, and the incoming data would all be important factors for the future path of monetary policy," he adds.

Wednesday's minutes suggested that FOMC members acknowledged early on in November's discussion that the U.S. economy now appears to be growing at below what might be considered its typical pace with some interest rate-sensistive parts of the economy having slowed noticably.

Risks to the outlook were also seen on the downside but "all participants" agreed that interest rates would have to rise further after data had "provided very few signs that inflation pressures were abating," and given that wages were growing at levels "inconsistent with achievement of" the 2% inflation target.

This leaves much to be determined by economic figures emerging between here and the December meeting as well as by the inflation data set for release shortly after then and in the following months, which will be important for determining how much further interest rates are likely to be raised.

"This means that one-way traffic in FX, with the dollar staying on a downtrend for longer, still appears unlikely," says Francesco Pesole, a strategist at ING.

"While we don’t exclude the dollar contraction to take DXY below 105.00, we struggle to see sub-105 levels holding for very long," he adds.

Above: U.S. Dollar or DXY Index shown at daily intervals with 200-day moving-average and Fibonacci retracements of rally that followed September 2021's Fed decision indicating possible areas of technical support. Click image for closer inspection.

Above: U.S. Dollar or DXY Index shown at daily intervals with 200-day moving-average and Fibonacci retracements of rally that followed September 2021's Fed decision indicating possible areas of technical support. Click image for closer inspection.