Image © Adobe Images

Matt Weller, Global Head of Research of City Index, details what to watch on the path to pound parity.

When was the last time the British pound sterling traded at parity (1.00) with the US dollar?

No need to dig out your history books; it's not a trick question. The pound has NEVER traded at parity with the US dollar.

After spending the entirety of the 1800s at around 5:1, sterling has been trending generally lower against the greenback for the past century.

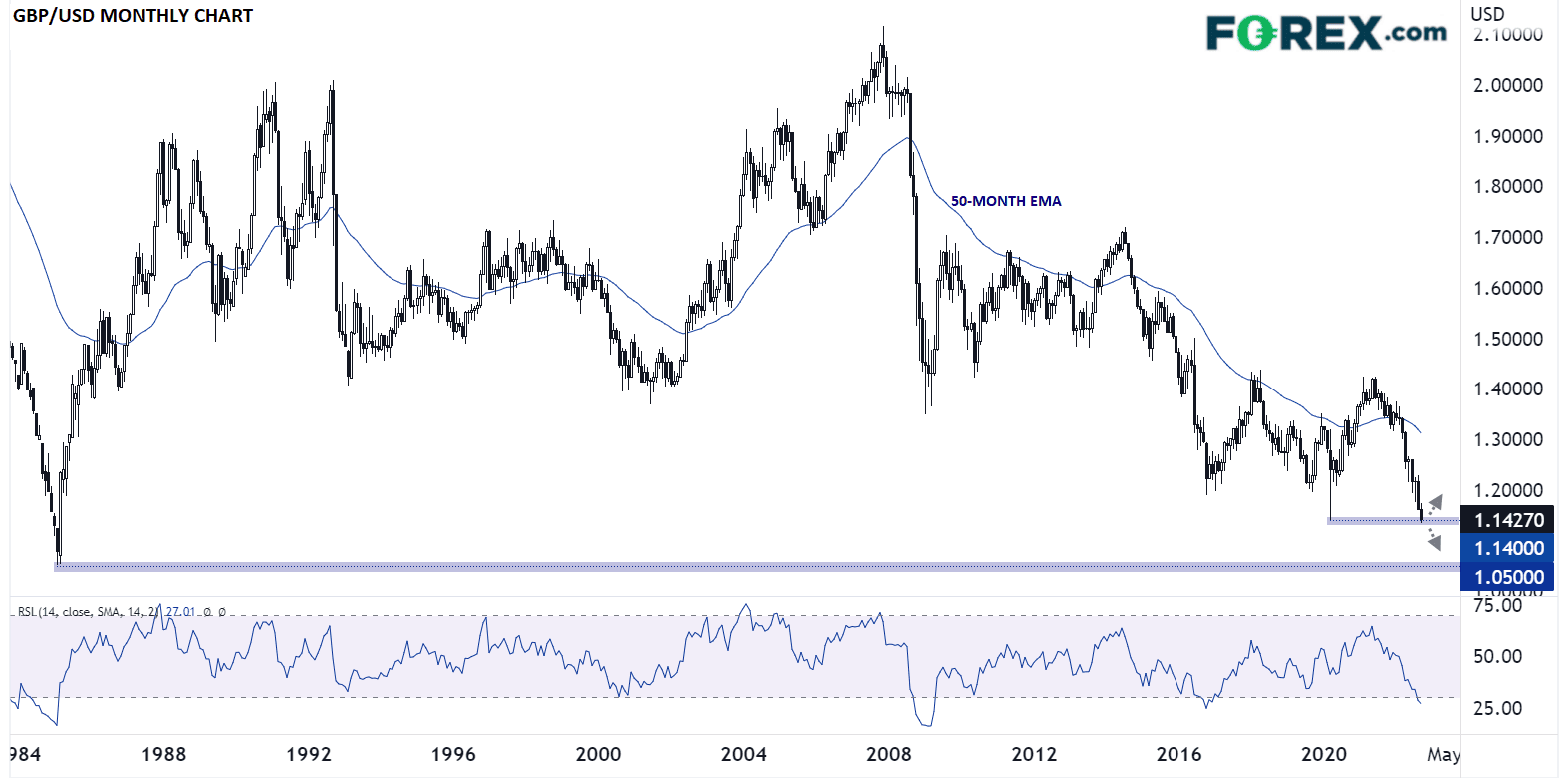

The closest the two currencies got to one another was in 1985, when the GBP/USD exchange rate briefly fell below 1.10.

GBP/USD: Historical parallels with 1985

Proving that history doesn’t repeat but it does rhyme, the new UK Prime Minister Liz Truss’s role model, Margaret Thatcher, was in charge back then, and the US had passed large tax cuts under a Republican President (Reagan) a few years earlier that were starting to bear fruit on the underlying economy.

Eerily, both the US and UK were grappling with elevated inflation in 1985, though the US was able to get a grasp on price pressures before its colonial overseer, much as traders and policymakers are expecting this time around.

In addition, oil prices were normalising after a sharp spike into the triple digits that led to rationing and calls for price caps.

What factors could drive the pound to parity?

Relative to the US economy, the UK economy is at higher risk of seeing a brutal stagflationary period in the coming quarters.

The BOE recently predicted that the UK economy would see a prolonged recession and that inflation would peak above 13%; notably, that inflation forecast was before the UK government announced a plan to cap household energy prices that may put peak inflation closer to 11% in the island nation, but that is nonetheless higher than the US is expected to reach.

While it may defray price pressures, the UK government’s energy cap scheme risks blowing out the UK’s current account deficit further.

As a reminder, the current account measures the total value of goods and services a country imports relative to the total value of goods and services it exports.

After holding steady in the 1% to 5% of GDP range for decades, the UK current account recently widened to 8% in Q1 2022.

If gas prices keep rising due to Russia cutting off deliveries to the European continent, the cost of the energy subsidy scheme could soar, exposing the government’s balance sheet to large losses and driving down the value of the pound sterling sharply.

What to watch on the path to pound parity

Once seen as fanciful, there is some evidence that FX options traders are at least considering the possibility of GBP/USD parity.

According to NatWest, current options pricing implies a roughly 25% chance that GBP/USD could hit 1.00 in the next 12 months; similar calculations by Bloomberg put the implied probability closer to 20%.

As outlined above, a continued rise in energy prices could speed the prospect along, as would stubbornly high inflation or a deep recession on the European continent.

Technically speaking, GBP/USD is currently testing its COVID-lows near 1.1400, the last level of previous support until the 1985 closer to 1.0500.

While still not necessarily the most likely path, a break below the 1985 lows would truly bring parity into play for the first time in the 200+ year history of the GBP/USD exchange rate.

Expectations for a 100bp Hike at Fed Overblown

The Federal Reserve's September policy decisions is due Wednesday 21. Weller says he doesn't believe the Fed will be panicked into a 100bp rate hike:

It seems like a lifetime ago, but at this time last month, traders were thinking the Fed was more likely to raise interest rates by just 50bps (0.50%) in its September monetary policy meeting.

However, after a hawkish address from Fed Chairman Powell at Jackson Hole, another solid NFP report, and a much hotter-than-expected CPI report, the market has completely thrown out any possibility of a mere 50bps rate hike and even started to price in an outside chance of a full 100bps (1.00%) rise.

In our view, the possibility of a 100bps rate hike is overblown.

Lost amongst traders’ handwringing over the Fed’s clear focus on defeating inflation and the hotter-than-anticipated CPI reading is the fact that inflation is still declining relatively sharply.

After all, the year-over-year CPI inflation rate has fallen from 9.1% to 8.5% to 8.3% over the last two months.

While the Fed would certainly have preferred to see a rate closer to 8.0% last month, other measures of inflation are clearly falling rapidly, suggesting that the hotter-than-expected CPI reading may be a one-off outlier.

For example, the recently-released New York Fed survey showed that 1-year inflation expectations fell to 5.7% (from 6.2%) previously, and the survey’s average 3-year expectation for inflation fell from 3.2% to 2.8%, within shouting distance of the Fed’s long-term target near 2%.

Above: "Going long the US dollar remains the most obvious trade in the FX market" - Weller.

In other words, there is no evidence that we are entering a self-fulfilling cycle of rising prices; if anything, the evidence suggests that consumers and businesses expect price pressures to keep dropping in the coming quarters.

Instead of pointing to a 100bps rate hike this month, the stubborn inflation readings of late suggest that the central bank may be forced to raise interest rates for longer, perhaps into the first half of 2023, rather than pausing the current tightening cycle at the end of this year.

A month ago, traders were pricing the peak interest rate for this cycle around 4.00% in January; now the market expects rates to peak closer to 4.50-4.75% in Q2 2023.

Notably, this meeting will provide an updated Summary of Economic Projections (SEP), including the infamous “dot plot” of Fed members’ interest rate expectations.

Traders will be keen to see when and where Federal Reserve policymakers see this tightening cycle coming to an end.

Finally, the central bank is still ramping up its Quantitative Tightening (QT) program to wind down its balance sheet, so any comments around how Jerome Powell and Company see that developing could move markets as well.

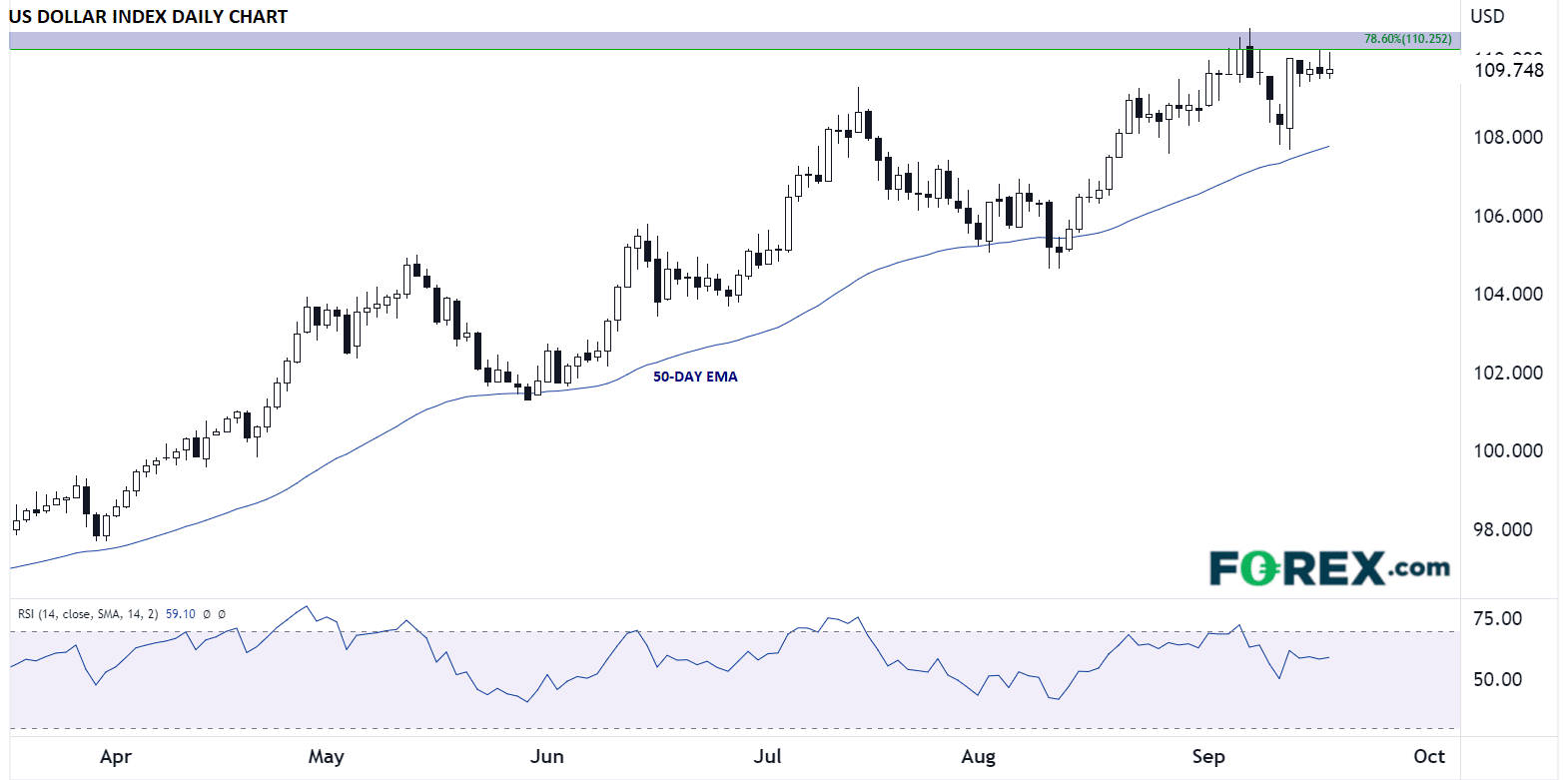

Going long the US dollar remains the most obvious trade in the FX market (though that doesn’t necessarily means it will work out!). Not surprisingly, the US dollar index continues to find support at its rising 50-day EMA, keeping the bias in favor of the bulls.

As of writing, the index is testing the 78.6% Fibonacci retracement of its big 2001-2008 fall near 110.25, but if the Fed comes off as more hawkish than anticipated, a break and close above that area could target 112.00 or higher heading into October.