- GBP/USD closes in on lowest levels since early 1985

- Risk of deeper loss amid growing energy supply threat

- New PM, policy agenda also key for BoE policy & GBP

- BoE speeches, Fed chatter & U.S. PMIs also in focus

Image © Adobe Images

The Pound to Dollar exchange rate sustained heavy losses last week but now risks falling further after a Russian state energy supplier announced an indefinite suspension of gas deliveries to Germany, which could weigh heavily on the Euro and other European currencies in the days ahead.

Sterling made a beeline for its longest run of intraday losses on Monday when falling against the Dollar for a seventh consecutive session following a late Friday announcement from Russia’s Gazprom warning that the Nord Stream gas pipeline would remain closed indefinitely.

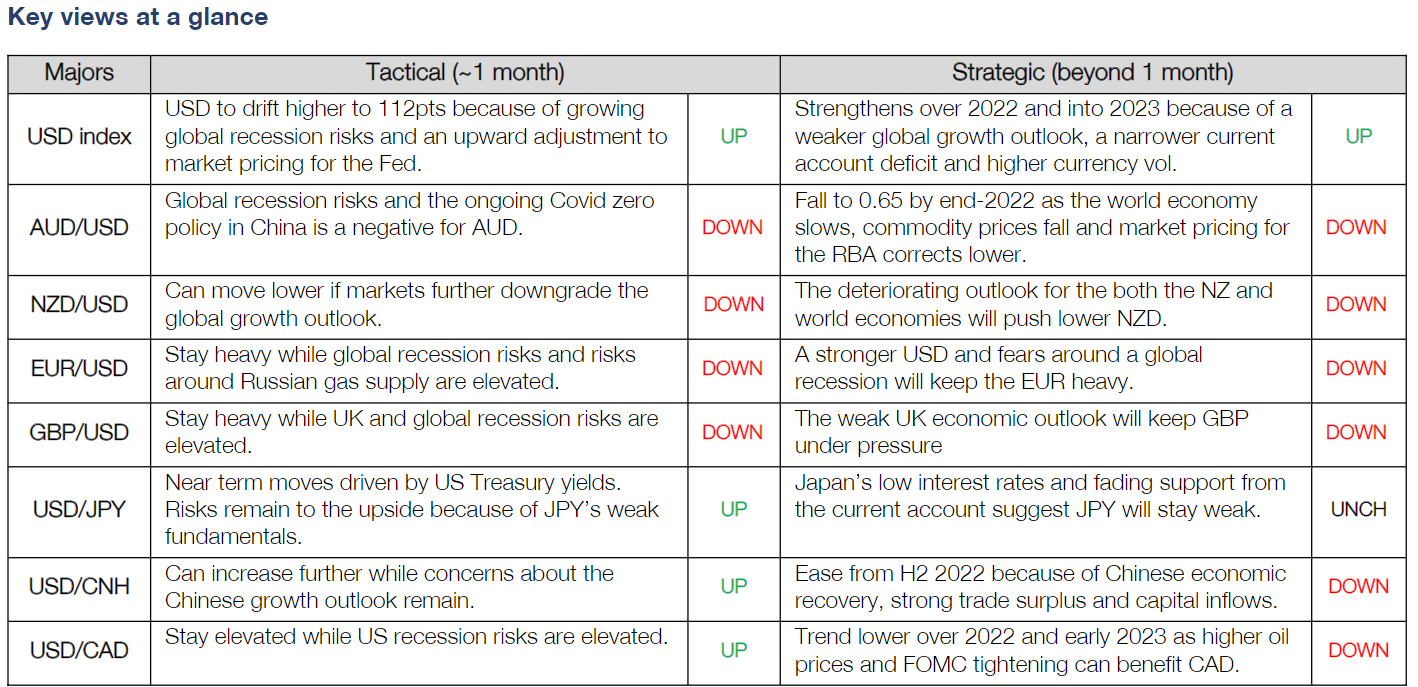

“The Group of Seven governments agreed to (attempt to) implement a price cap on Russian oil exports,” says Joseph Capurso, head of international economics at Commonwealth Bank of Australia.

“GBP/USD can remain heavy this week because of fears around strongly rising inflation and imminent recession. GBP/USD could fall below the covid low of 1.1412 this week. There is no important domestic economic data scheduled,” Capurso and colleagues said in a Monday research briefing.

The Pound-Dollar rate was closing in on 1.1412, its joint lowest level since March 2020 and April 1985, on Monday while it wasn't clear if weekend remarks from Foreign Secretary Liz Truss will be enough to keep it from falling further in light of the crystallising energy supply risks.

Above: Pound to Dollar rate shown at daily intervals.

Above: Pound to Dollar rate shown at daily intervals.

The Foreign Secretary is expected to be announced as the Conservative Party nominee for the role of Prime Minister on Monday so it’s possible Sterling will be cheered by her assurance of the monetary policy independence of the Bank of England (BoE) in an interview with the BBC at the weekend.

Some analysts and economists had cited a planned review of the BoE’s remit and doubts about her commitment to monetary policy independence as likely contributors to the Pound’s losses against the Dollar and other currencies over recent weeks.

But also important are the details of campaign commitments to “immediate action” on the ‘cost of living crisis,’ which could have implications for a BoE interest rate policy that will also be in focus when Monetary Policy Committee member Catherine Mann speaks at 16:30 on Monday.

She participates in the 53rd Annual Conference of the Money Macro and Finance Society at the University of Kent ahead of Wednesday’s parliamentary appearances by Governor Andrew Bailey and others who’re scheduled to testify about the August Monetary Policy Report.

“While this week’s fall is likely to have been exacerbated by month-end rebalancing and corporate flows, it’s clear that UK assets aren’t seen as attractive at current exchange rates,” says Paul Robson, Europe head of G10 FX strategy at Natwest Markets.

Above: Pound to Dollar rate shown at weekly intervals with Fibonacci retracements of 2020 recovery indicating possible areas of short-term technical support for Sterling. Click image for more detailed inspection.

Above: Pound to Dollar rate shown at weekly intervals with Fibonacci retracements of 2020 recovery indicating possible areas of short-term technical support for Sterling. Click image for more detailed inspection.

“It means risks for Sterling are heavily skewed in favour of further declines, potentially steep declines. While the cyclical low of 1.1412 may see a pause, there is really very little reason why the decline will stop at this level unless the growth outlook improves,” Robson said on Friday.

While European energy troubles and British government policy will likely be the dominant drivers of the Pound to Dollar rate in the days ahead, there is also a sluice of important U.S. economic data due out and a raft of Federal Reserve (Fed) policymakers who’re set to speak publicly.

Most notably of all, Fed Chairman Jerome Powell will participate in a moderated discussion at the Cato Institute’s Annual Monetary Conference on Thursday, although before then three others will also attend public engagements including Vice Chair Lael Brainard.

“Fed officials remain uncommitted on the size of the rate hike at the 20-21 September FOMC meeting. They want to digest all available data before finalising the decision, with the August CPI data being a key input,” says Tommy Kenny, a senior economist at ANZ.

“Real US Treasury yields jumped sharply higher last week as nominal yields rose and inflation expectations, as implied by TIPS, fell notably. Real yields are back at levels prior to the July FOMC meeting. Fed officials would welcome this tightening in financial conditions,” Kenny said on Monday.

Source: Commonwealth Bank of Australia. Click image for closer inspection.

Source: Commonwealth Bank of Australia. Click image for closer inspection.

With Fed officials aside, the most important event in the U.S. calendar will likely be Tuesday’s release of the Institute for Supply Management (ISM) Services PMI for August, which is expected to edge lower from 56.7 to 55.0.

Just the same as with last week’s Manufacturing sector PMI, the market may look to see if it confirms the message of the earlier S&P Global PMI surveys, which suggested that both industries slipped deeper into recession last month but were contracted by the ISM surveys.

“USD [Dollar Index] is expected to continue trending higher above 110pts this week. The deteriorating outlook for the world economy – especially in Europe and China –supports the USD because it is a safe haven currency. The US economy by contrast is in good shape. Rising US yields relative to elsewhere support the USD,” CBA’s Capurso said on Monday.

“The FOMC’s Beige Book is the US highlight (Thursday). Market participants will be interested in early signs that supply chain congestion is easing and the impact of higher interest rates on growth in demand. A spike in volatility measures and/or slump in equity markets could push the USD [Dollar Index] above 112pts this week,” he added.

Above: U.S. Dollar Index shown at monthly intervals with Fibonacci retracements of January 2002 downtrend indicating possible areas of technical resistance and shown alongside 02-year and 10-year U.S. government bond yields.

Above: U.S. Dollar Index shown at monthly intervals with Fibonacci retracements of January 2002 downtrend indicating possible areas of technical resistance and shown alongside 02-year and 10-year U.S. government bond yields.