Above: File image of James Bullard. © Pound Sterling Live. Still courtesy of CNBC.

The U.S. Dollar sits atop its peers as European and other global economies reopen following the easter break, with analysts citing the comments of a prominent member of the Federal Reserve for the new outperformance.

The Dollar hit new 2022 highs after Federal Reserve Bank of St. Louis President James Bullard said the central bank needs to move quickly to raise interest rates to around 3.5% this year with multiple half-point hikes and that it shouldn’t rule out rate increases of 75 basis points.

Bullard said "I wouldn’t rule it out" when addressing the prospect of raising rates by more than 50 basis points.

A 75 basis point hike would represent a dramatic sign of intent by the Fed to get on top of rising inflation, and is something markets were not anticipating until the comments introduced the idea.

The last time the Fed hiked by 75bps was in November 1994.

Bullard was addressing the Council on Foreign Relations when delivering the comments which only stoked expectations for a series of rapid interest rate rises at the Fed in 2022.

"Bullard spoke yesterday afternoon with a very hawkish tone suggesting that the Fed needs to move quickly in order to raise interest rates to around 3.5% by the end of this year and that the Bank shouldn’t rule out raising rates by 75bps if needed, although this is not his base case. The comments added to the demand for the US dollar with the dollar index making new 23-month highs," says Thanim Islam, Dealer Manager at Equals Money.

Money markets now show investors to be expecting another 215 basis points of rate hikes to be delivered by the Fed by the time the year is out.

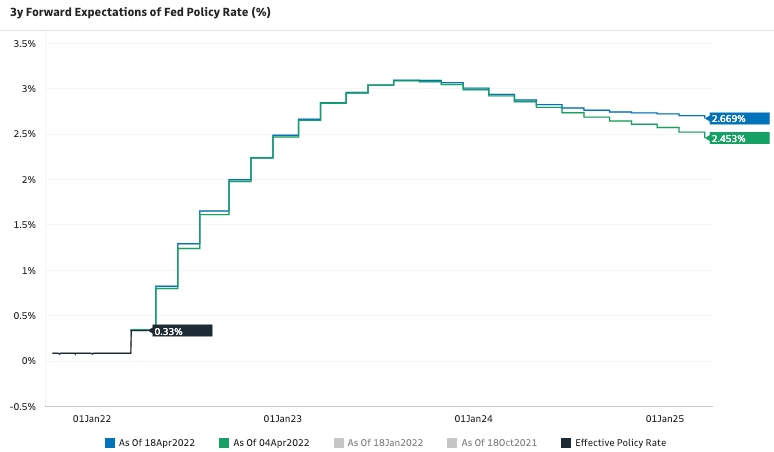

Importantly the TOTAL amount of rate hikes expected from the Fed in the current hiking cycle has risen of late, which is typically supportive of a currency:

Above: Fed hike expectations rise, image courtesy of Goldman Sachs.

The rising of the total amount of hikes to 2.669% in the above, from 2.543% previously, is on balance supportive of the U.S. Dollar.

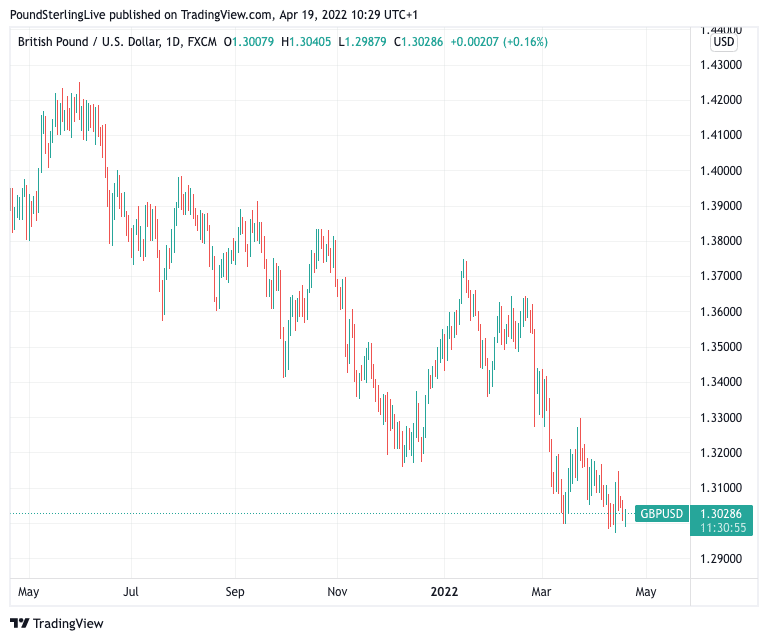

The Pound to Dollar exchange rate dipped below 1.30, the Euro to Dollar rate went below 1.07 to test 1.0761 and the Dollar index - a broader measure of overall Dollar performance - rose to new post-Covid crisis highs at 101.77. (Set your FX rate alert here).

"The USD is making gains above key technical levels – which suggests that a breakout is underway here. The big contributor to this move is the Fed’s divergence with other central banks when it comes to policy," says Bipan Rai, Head of North American FX Strategy at CIBC Capital Markets.

The Yen is the biggest loser with USD/JPY now on track to record its 13th successive daily decline.

The Bank of Japan is not anticipated to hike rates in 2022, confirming it holds the largest divergence with the U.S. Federal Reserve, and it is this divergence that is aiding the Dollar against the low-yielding yen.

"The US yield curve is also inverting and indeed, there are risks to both US and global growth. These suggest the USD should continue to have the upper hand," says Paul Mackel, who heads currency research at HSBC.

Above: The Pound-Dollar exchange rate at daily intervals showing an entrenched downtrend.

Bullard's warning that a 75 basis point hike rate cannot be ruled out is indicative of just how concerned the Fed has become with U.S. inflationary levels.

By raising rates the Fed would help slow the economic expansion and cool inflationary pressures.

But, this economic slowdown means that further out the Fed might have to cut rates again. This results in the yields on longer-dated bonds yielding less than nearer dated bonds.

This results in a flat or inverted yield curve, (this is reflected in the first chart above) as opposed to one that steadily rises to reflect the progressive rise in yields the longer bond durations extend.

"Front-loaded tightening should lead to flat or inverted yield curves, which in our experience are positive for currencies," says Chris Turner, Global Head of Markets and Regional Head of Research for UK & CEE at ING Bank.

"One extreme example, which some customers have been asking us about, is the extreme US yield curve inversion in the early 1980s when new Federal Reserve Chair Paul Volcker took rates to 15% and sent the dollar into recession," he adds.

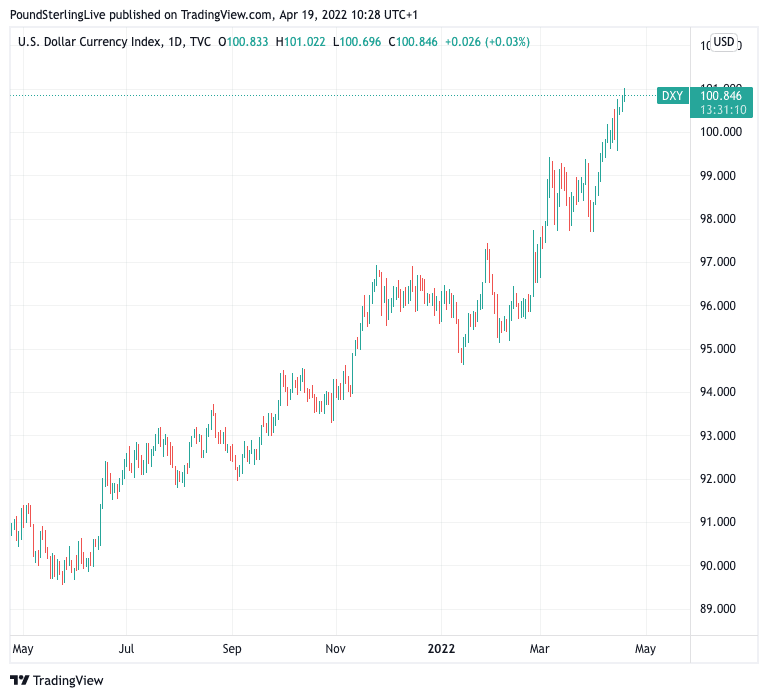

Above: The Dollar index is at its highest levels since March 2020.

Turner says the dollar soared during this period. "Inverted yield curves also discourage FX hedging of bond portfolio flows – i.e. is positive for a currency".

Safe haven demand is also driving the Dollar, with the war in Ukraine ramping up as Russia commences a new offensive in the Donbas region.

The Dollar has tended to benefit as a result of its dual qualities of offering higher yield (courtesy of Fed rate hikes) and ongoing uncertainty in global markets.

A much-watched survey reveals global growth optimism amongst some of the world's biggest investors has fallen to an all-time low.

The Bank of America Global Fund Manager Survey for April reveals sentiment "is bearish as fear of fast & furious Fed sends global growth optimism to all-time low".

Reporting their latest findings Bank of America says they "remain in 'sell-the-rally' camp as the January/February sell-off was the "appetizer not main course of '22".

Investors now expect the Fed to hike interest rates seven times, up from four in March, with the cycle ending in the first half of 2023.

83% of investors surveyed now believe the Federal Reserve is set to make a policy mistake, i.e. they will have to reverse some of the cycle's hikes relatively soon after completion.

The survey reported a 7ppt month-on-month decrease to net 71% of investors expecting a weaker economy in the next 12 months, the lowest growth expectations ever.

"The dollar is likely to remains favoured until we see geopolitical risk and downside growth risk ease in Europe and China," says Anders Eklöf, Chief FX Strategist at Swedbank.