- GBP/USD charts warning of further rebound ahead

- U.S. CPI eyed for clues on inflation & Fed outlooks

- After Fed tapers & says can be “patient” on inflation

- UK GDP data, BoE speeches the highlights for GBP

Image © Adobe Images

The Pound to Dollar rate attempted a sharp recovery from near 2021 lows on Friday and left behind an indication on the charts that a further rebound could be likely this week, but much will depend on the market’s appetite for the greenback and response to U.S. inflation figures.

Sterling had been left reeling after last Thursday’s monetary policy decision from the Bank of England forced investors to begin grappling with mistaken assumptions about the outlook for interest rates in the UK but it rallied sharply in the final hours of trading on Friday.

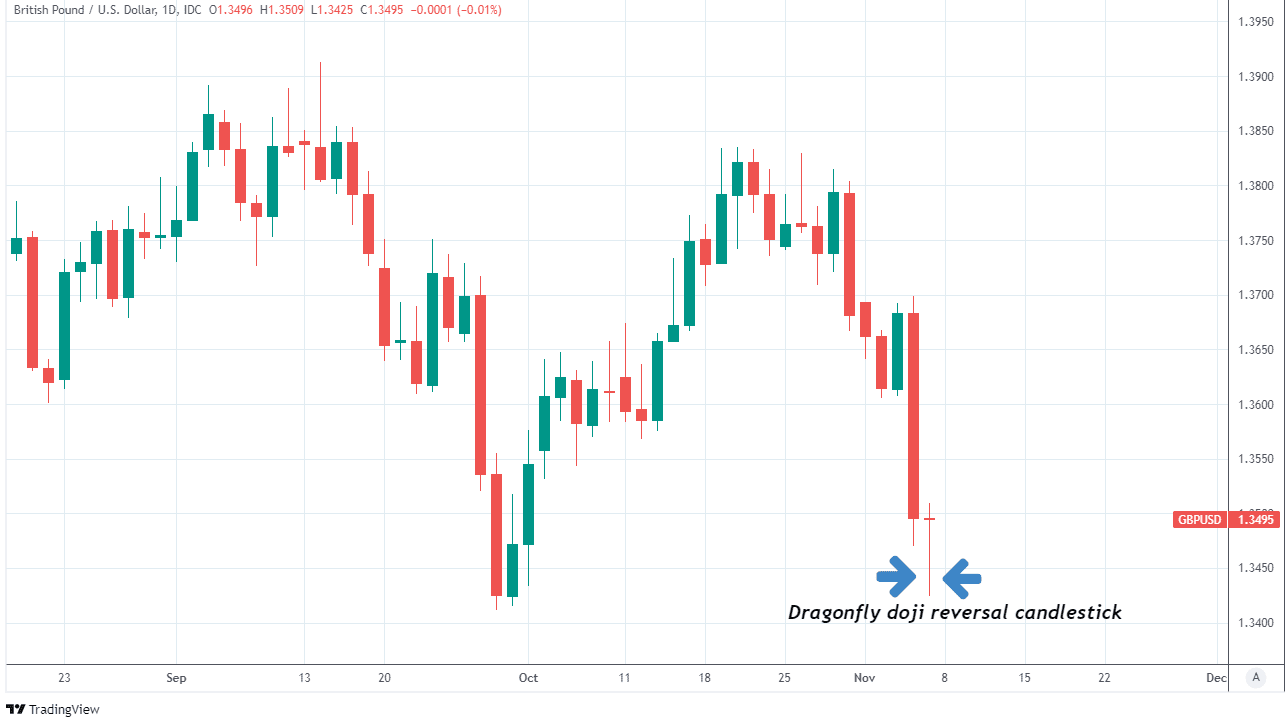

The rebound occurred as U.S. exchange rates softened across the board and saw the Pound-Dollar leave in its wake on the charts what technical analysts call a “dragonfly doji” candlestick, which sometimes comes as a precursor to a trend reversal.

“The sharp rejection of a new low, coupled with the inability of prices to close clearly lower on the day amplifies the bullish undertone of this pattern,” says George Davis, chief technical strategist at RBC Capital Markets, referring to a ‘dragonfly doji’ in an RBC glossary of technical analysis terms.

The above referenced, and below pictured candlestick indicates that the downside could be limited for the Pound-Dollar rate over the coming days and that it may even be especially responsive to any extended retreat by the greenback.

Above: Pound-Dollar rate shown at daily intervals with ‘dragonfly doji’ candlestick.

- GBP/USD reference rates at publication:

Spot: 1.3481 - High street bank rates (indicative band): 1.3109-1.3204

- Payment specialist rates (indicative band): 1.3360-1.3387

- Find out about specialist rates, here

- Or, set up an exchange rate alert, here

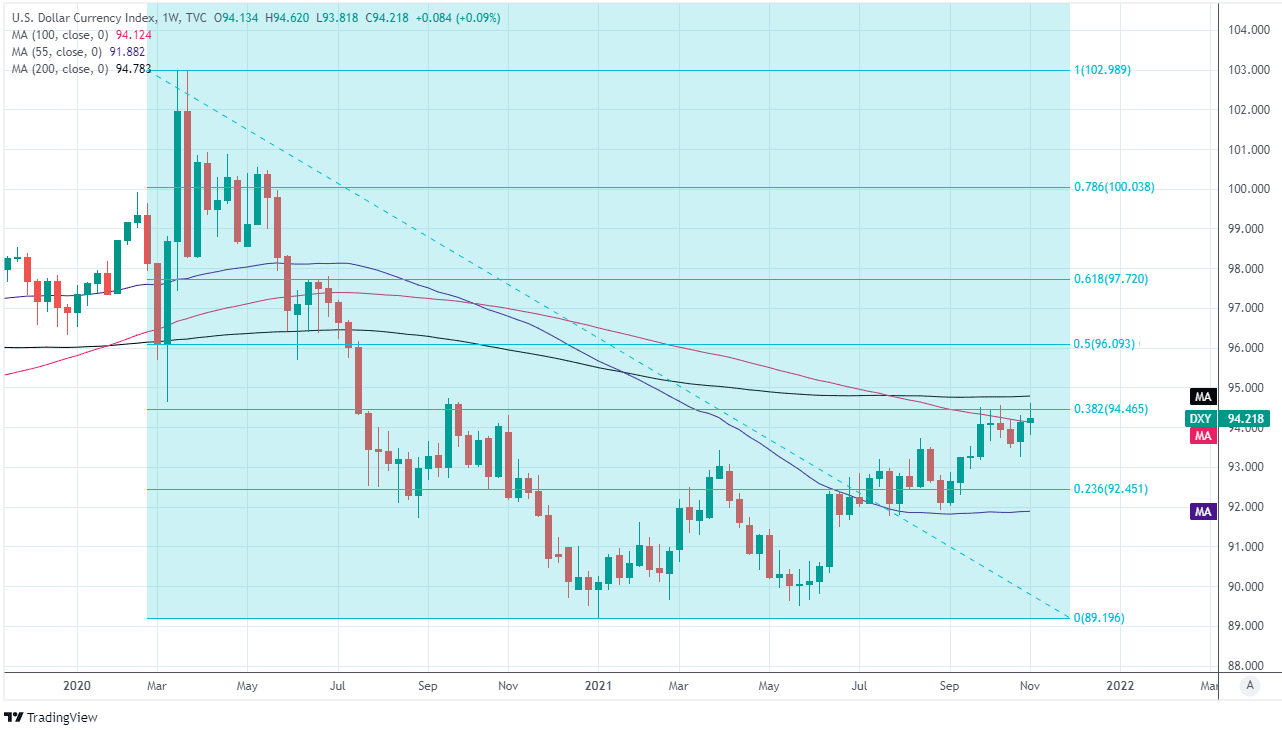

The Dollar Index had been testing a pocket of major resistance levels on the charts before it slipped in the wake of Friday’s stronger-than-expected non-farm payrolls report, which came alongside upward revisions to estimates of job growth in prior months and followed Wednesday’s Federal Reserve decision to taper away its $120BN per month quantitative easing programme over the eight months to mid-year 2022.

“With a Fed that has just fired the starting gun on its normalisation process, momentum on the US-developed RoW monetary policy divergence story seems to be swinging back towards the US side, which is putting a quite solid floor under the dollar,” says Chris Turner, global head of markets and regional head of research for UK & CEE at ING.

The Pound-Dollar rebounded from near 2021 lows but much about the outlook for this week depends for both currencies on the implications that investors might infer from Wednesday’s release of inflation data for October, especially in the context of what it could mean for Federal Reserve monetary policy.

{wbamp-hide start} {wbamp-hide end}{wbamp-show start}{wbamp-show end}

“The rent of shelter component may surge to 6% YoY levels as soon as in late Q1-2022, while the price of used cars has re-accelerated. >5% readings in core inflation are on the cards, while >6% readings in the headline are already consensus ahead of New Years. It will be an increasingly difficult cocktail to balance for central banks as basically all leading indicators on growth point down,” says Martin Enlund, chief FX strategist at Nordea Markets.

Economists widely expect U.S. inflation to remain above 5.4% in October’s data and for the core measure of inflation to remain at 4%, while many have warned that price growth could rise further over the coming months, which may tempt the market to believe that a sooner end to the Fed’s QE programme or some other policy action could become likely during the coming months.

But some of last Wednesday’s remarks from Chairman Jerome Powell suggested the Fed is already assuming that abnormally high levels of inflation will persist for longer and that it could afford to be patient in waiting for them to dissipate, given that recent increases in inflation have been driven almost entirely by temporary factors.

Above: U.S. Dollar Index at weekly intervals with major moving-averages and Fibonacci retracements indicating possible areas of technical resistance.

“Of course, the timing of that is highly uncertain, but certainly we should see inflation moving down by the second or third quarter. The time for lifting rates and beginning to remove accommodation will depend on the path of the economy. We think we can be patient. If a response is called for, we will not hesitate,” Chairman Powell said in Wednesday’s press conference.

The potential rub for the greenback and source of support for the Pound-Dollar rate here is that financial markets were already pricing-in close to two interest rate rises from the Fed by the end of 2022 and the Fed’s “patience” or tolerance of temporary overshoots of inflation suggests there’s little if any scope for the anticipated lift-off to be brought forward any further.

There’s little on the domestic side to guide the Pound-Dollar rate this week between the appearances from BoE Governor Andrew Bailey and other central bank heads until the UK’s September and third-quarter GDP data is released on Thursday at 07:00.

“We think GDP was unchanged on a month-to-month basis, undershooting the 0.4% consensus. Bar revisions, our forecast implies quarter-on-quarter GDP growth slowed to 1.3% in Q3, from 5.5% in Q2, below the MPC's latest forecast of 1.5%,” says Samuel Tombs, chief UK economist at Pantheon Macroeconomics.

Governor Andrew Bailey is set to speak at one of the BoE’s virtual Citizens' Panel Open Forum events around 17:00 on Monday before participating at 16:00 on Tuesday in a panel discussion titled "Central Banks and Inequality" at an online conference jointly hosted by the Federal Reserve, Bank of Canada, BoE and European Central Bank, although it’s not clear that these events would play host to discussions on Bank Rate.